Guest Blog Series

Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

There is a lot of doom and gloom out there. Analysts lament the demise of FICC revenues (Deutsche Bank a bright spot today though). IDBs seem to be particularly struck by a dearth of volumes, despite significant investments into shiny new SEF platforms.

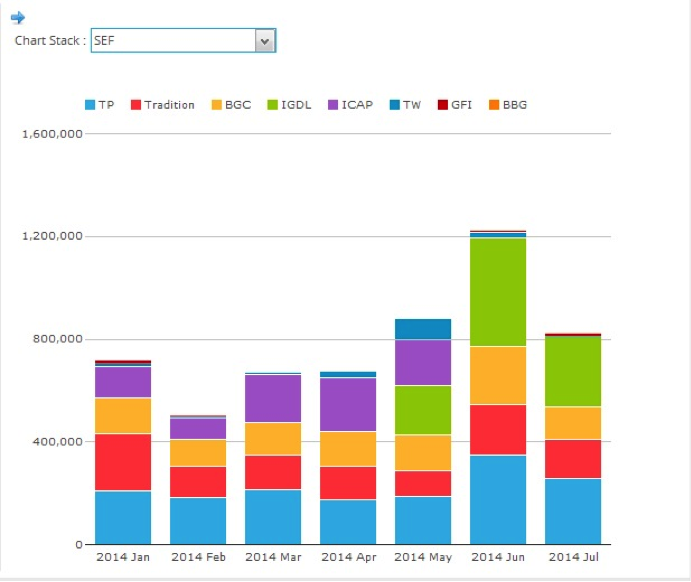

However, if you dig beneath the headline numbers, there are some significant bright spots out there. Look at short-end volumes for example. Bloomberg has been a particular success in the ever-evolving SEF story, but it has zero penetration in the OIS markets, leaving it all to the IDBs:

From SEFView, we can see:

(The BBG market share is so small in OIS that it does not even register on the above).

It’s welcome to see such a rising trend in volumes overall, despite the doom-mongers.

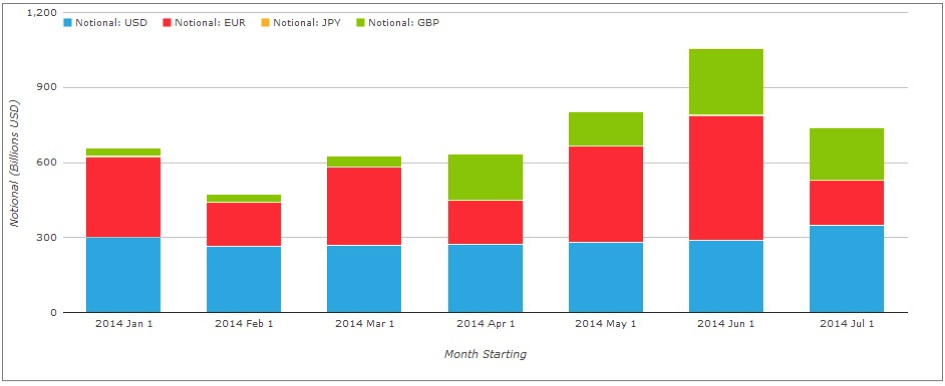

Let’s look at the currency breakdown for ON SEF trades only using SDRView:

Unsurprisingly, we can see a significant pick-up in Eonia volumes as the ECB first ramped-up their rhetoric. May saw +56% and June +81% increases on YTD average volumes. In addition, comparing the SEFView figures with those reported to DTCC, we see significant block activity with the typical block trade 9.4% larger than the threshold.

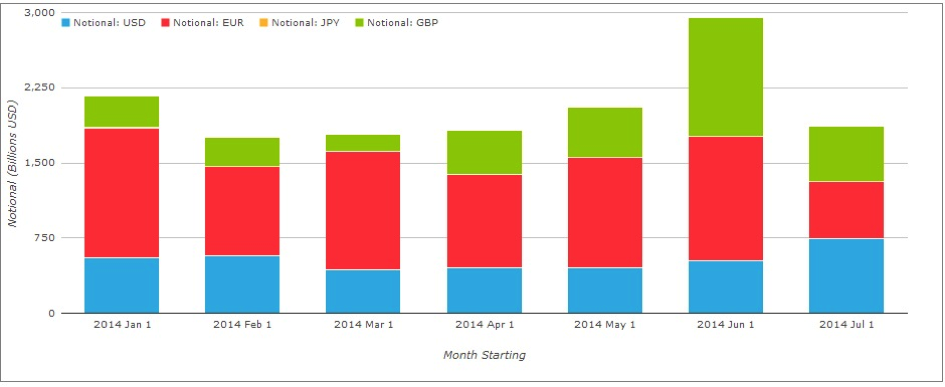

Whilst we can also see a significant up-tick in GBP Sonia activity, it isn’t until we look at On and Off SEF activity combined that we see more of the story:

GBP OIS (Sonia) volumes have been gradually climbing all year, until in May they eclipsed Fed Funds trading and June saw almost equal volumes of Eonia and Sonia trading.

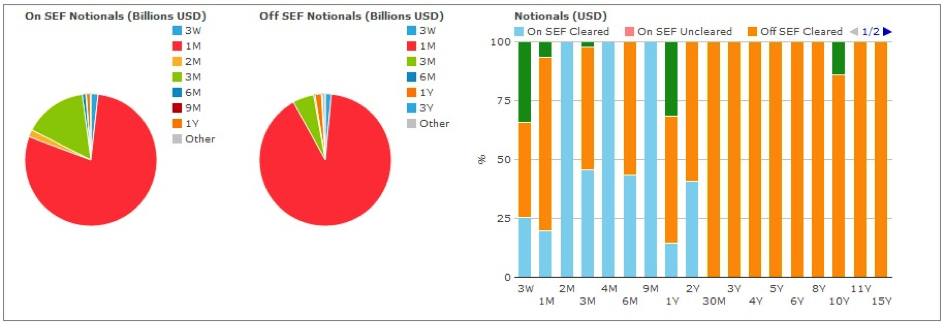

In terms of the tenors that trade, Eonia and Sonia couldn’t be more different. By notional, 88% of all Sonia trades are 1 month in maturity:

As we saw in the land of make-believe, there is a significant portion of Eonia trades – around 8% by notional – that trade longer than 1y in maturity. This is simply not seen in Sonia space, with only 0.75% of the notional longer than 1y. Whilst we saw that the structure of the Eonia market is moving away from a short-end focus into a liquidity-transformation play, we cannot say the same for Sonia.

The distinct lack of activity on the D2C SEFs for OIS further suggests they are still the realm of dealer banks. Looking at the data for June, we see that nearly 30% of the volume traded across two sessions – the 13 and 16 June – as the market reacted to Carney’s Mansion House speech. On these days, we see that nearly 15% of all trades were block, and 96% of notional was traded as a 1 month tenor.

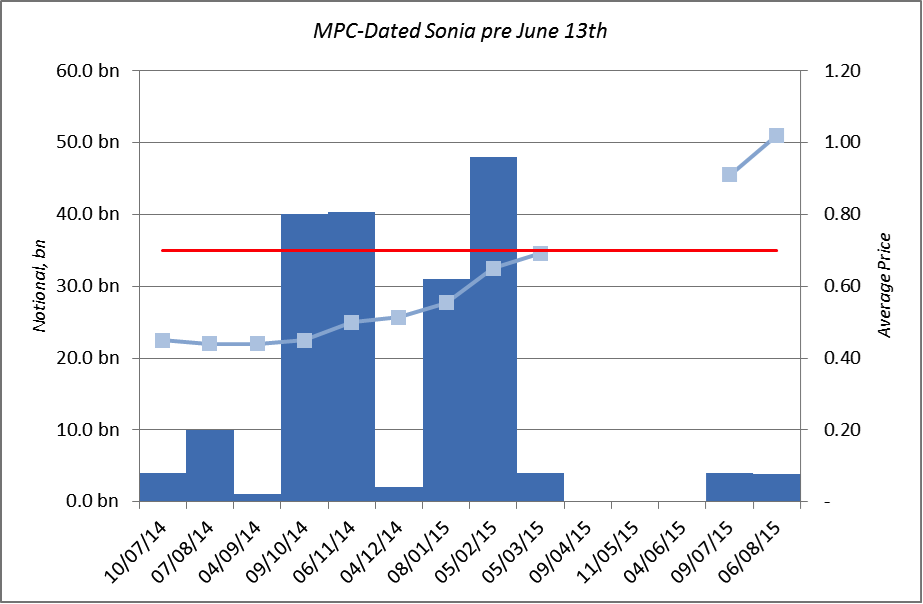

We can break the data down to analyse the market’s reaction before and after Carney’s pivotal speech. If we look at the volumes and price of MPC-dated trades before the 13 June, we see the following:

Showing;

- Feb 15 as the most traded meeting date with nearly $50bn equivalent trading

- The first interest rate hike not fully priced-in until March 15

- A total of $188bn traded

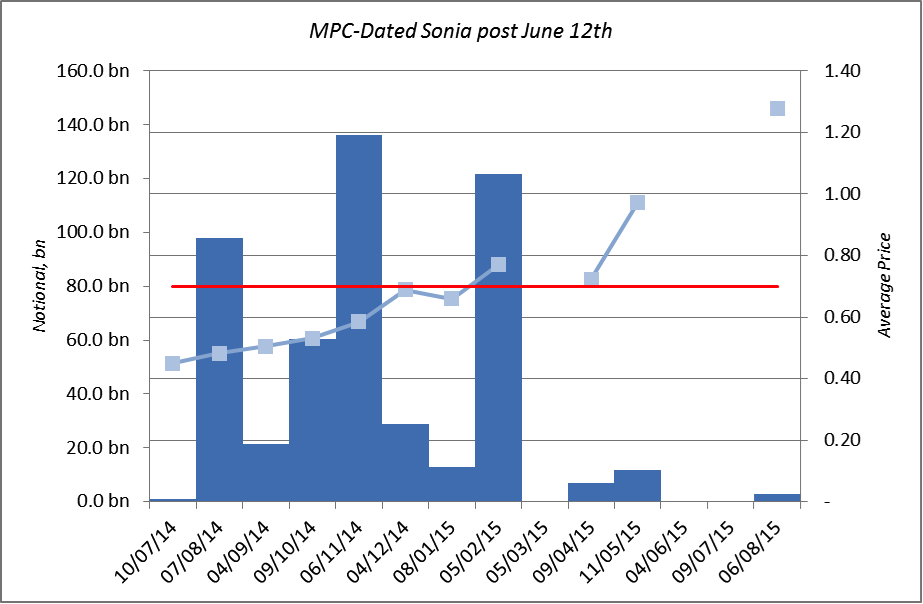

Now, the same analysis conducted post-Mansion House:

Showing a significant explosion of trading activity:

- $502bn-equivalent in total notional trading

- Nov 14 and Feb 15 are the two focal meeting dates – possibly a spread trade?

- A 25bp hike is priced-in for the Dec 14 meeting, in direct response to Carney stating rate rises “could happen sooner than markets currently expect”

- 11 block trades were seen before 13 June. 45 block trades went through in the rest of the month. The meeting in Feb 2015 saw the most block activity, with 21 trades throughout the month.

Once again, with a bit of digging, the granularity of data provided through trade reporting is remarkable. The fact that market activity is focussed on both November and February is not that surprising – both are Inflation Report months, and hence the most likely candidates for MPC rate action. However, the difference in structure of the Eonia versus Sonia markets is striking.

With the Sonia data offering such a clear picture of the short-end, such precise financial derivative information must aid the financial transmission mechanism in the UK. Indeed, there was a stagnation in house prices in July, and nowhere is it more evident than in the Sonia data above that the first interest rate hike is less than six months away.