All seems calm in the markets overnight. We’ll continue to update this blog throughout the day with observations on volumes and prices as activity picks up. Just hit F5 to refresh.

End of Day GBP Wrap-Up

Better late than never….we’ll close this blog with a review of what traded in GBP on the 29th June.

- 135 trades were reported to the SDRs in GBP swaps versus all Libor tenors

- £4.9bn in notional

- Over £3.3m in DV01

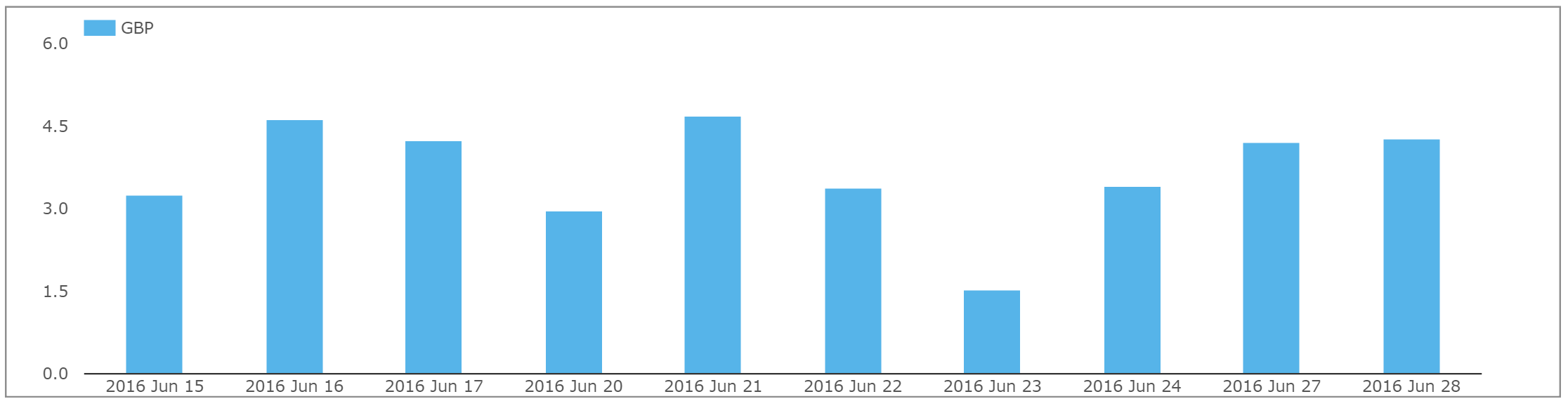

Comparing to previous days, we can see that the 29th was a less volatile day that also saw lower volumes. In terms of risk traded, it was still comparable to the Friday after the referendum, but lower than previous days this week.

15:01 LON – GBP Update

Interesting moves. We’ve had 3 OIS trades (finally!) and in decent size. Phew. We’ve also now seen over £2.9bn in notional trade along the GBP IRS curve.

Rates are (generally) higher, but in a flattening move. It looks a bit worrying to this observer. Is the market pricing out any rate action from the BoE but downgrading long-term growth prospects for the UK? I’d still be worried about funding the deficit. Keep an eye on swap spreads – I guess they’ll be negative soon enough?

11:42 LON – GBP OIS Anyone?

According to my screens, we are yet to see a single OIS trade in GBP today. Really? We’ve seen around £50bn trading every day for the past week. We’ve had a 1.5bp range in Sep Short Sterling this morning. And no trading in OIS? Welcome to the strange world of Sterling and fleeting liquidity…

11:35 LON – GBP Volumes pick up

GBP IRS volumes are beginning to pick-up nicely again today. We’ve now seen 45 trades hit the SDRs in a total of £1.2bn. This equates to nearly £1m in DV01. 10 years is once again back down at 1.00% and the curve is flattening.

09:32 LON – GBP Update

A very subdued start to the session today. Not much to report. 10 year swaps have traded higher at 1.021%, which is more in-line with most of yesterday’s trading – recall that 10 years closed towards the lows of the day yesterday at 1.00%.

- 10 swaps so far traded

- Only £276m in total notional

- Equating to less than £135k in DV01.

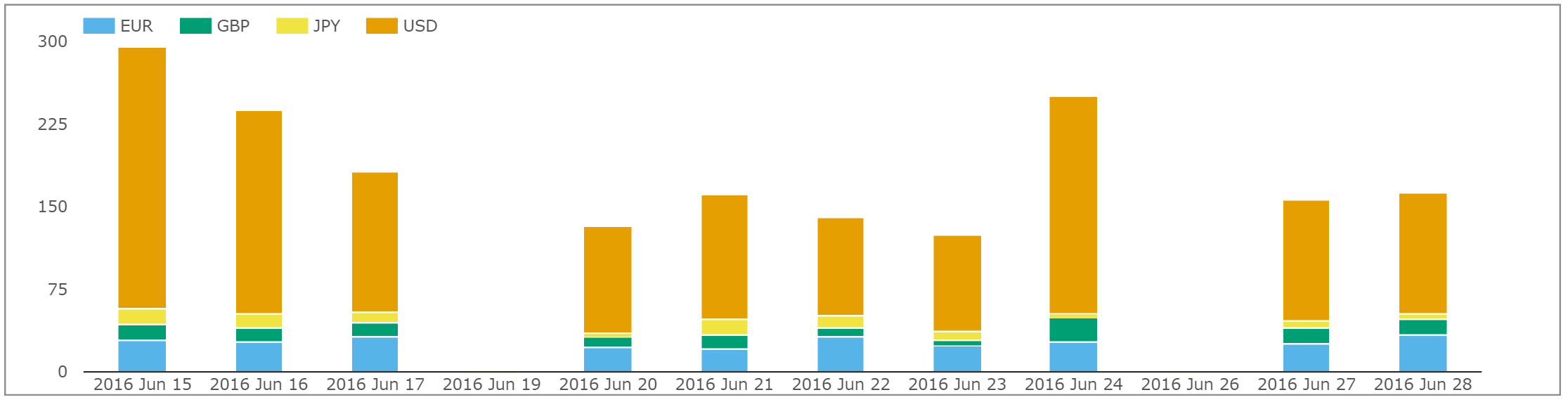

A very quiet start. Volumes below:

08:18 LON – USD Update

Still not much going on in the Swaps market. Only one GBP trade (see 08:05) and USD swaps are still subdued. A total of $2.6bn in notional has now traded in USD swaps, with Rates stable.

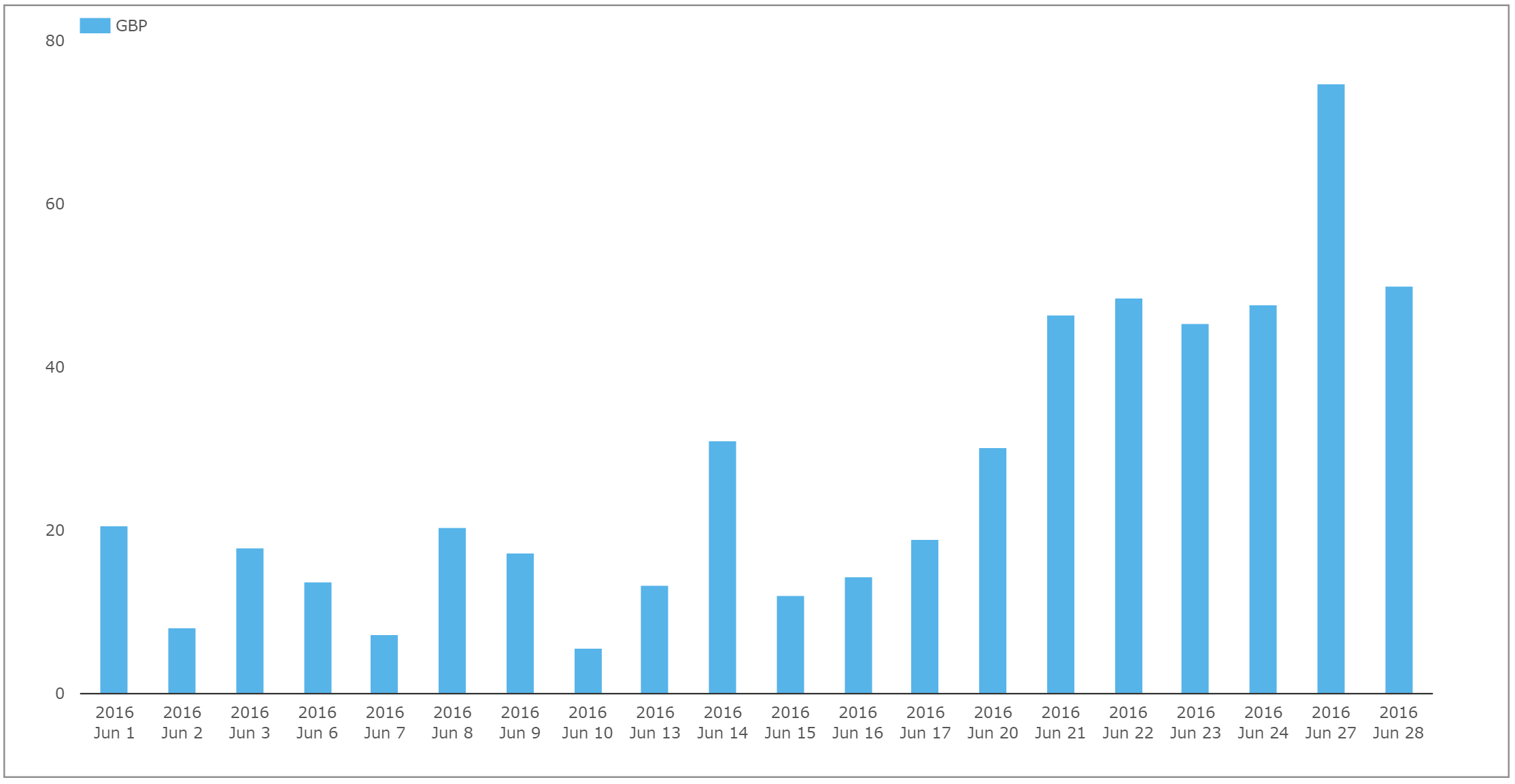

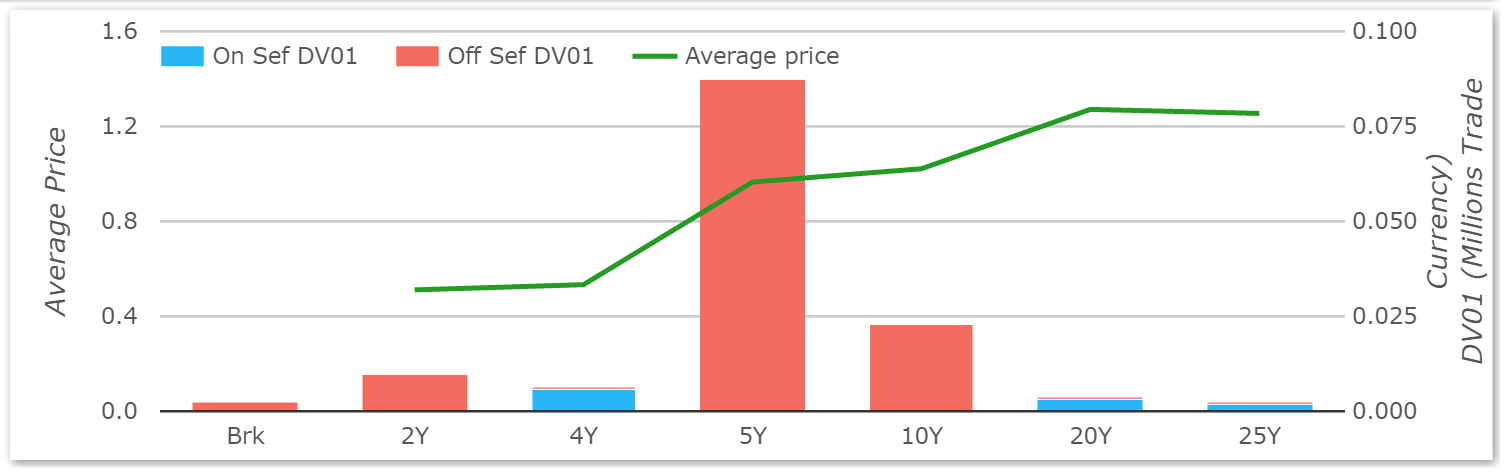

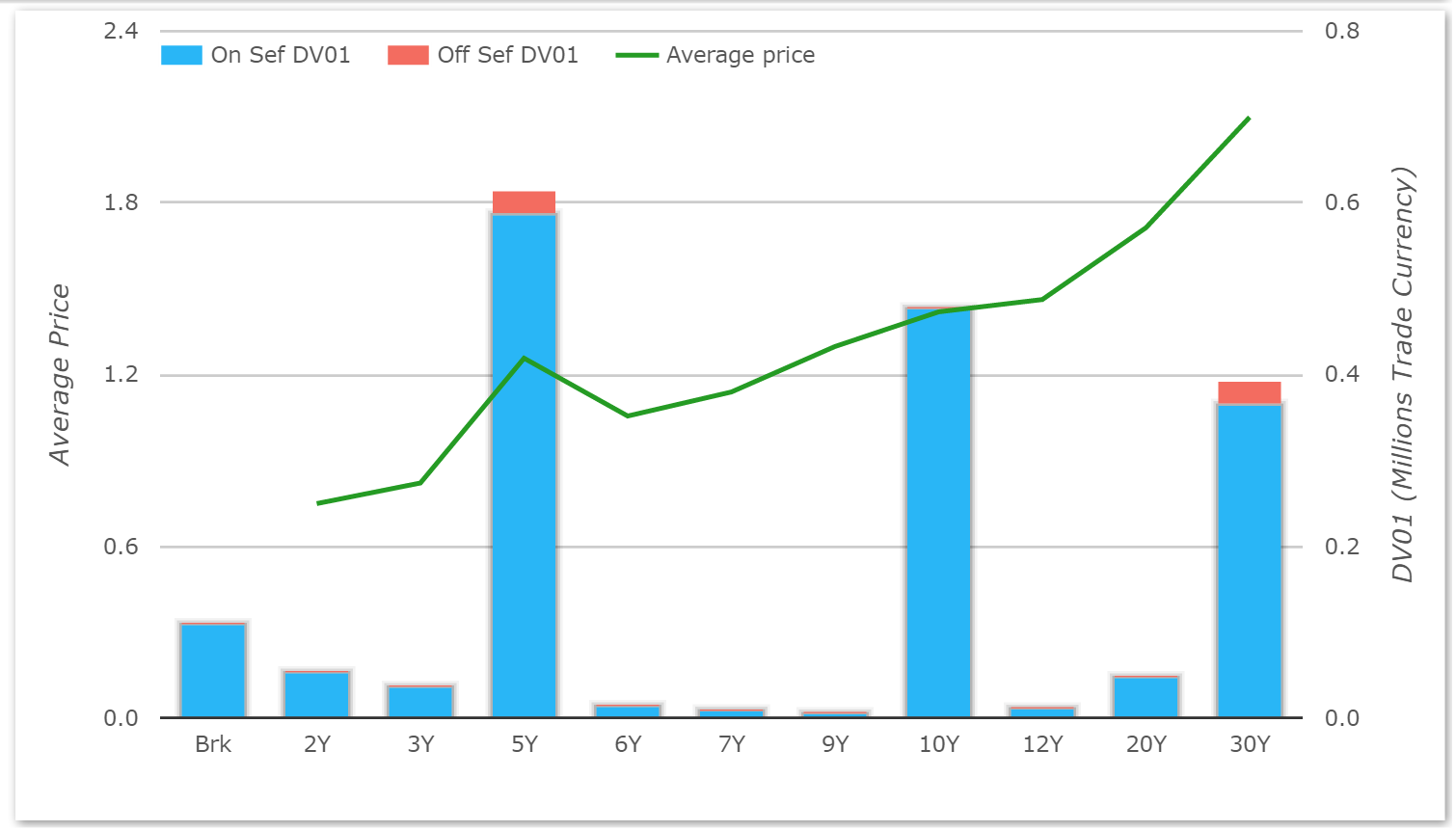

08:05 LON – Volumes Review for 28th June

Yesterday’s price action may not have been as volatile as previous days, but we nevertheless continued to see elevated volumes. It is not especially apparent when looking at GBP, USD, EUR and JPY swaps together. This is because USD swaps didn’t have a very big day:

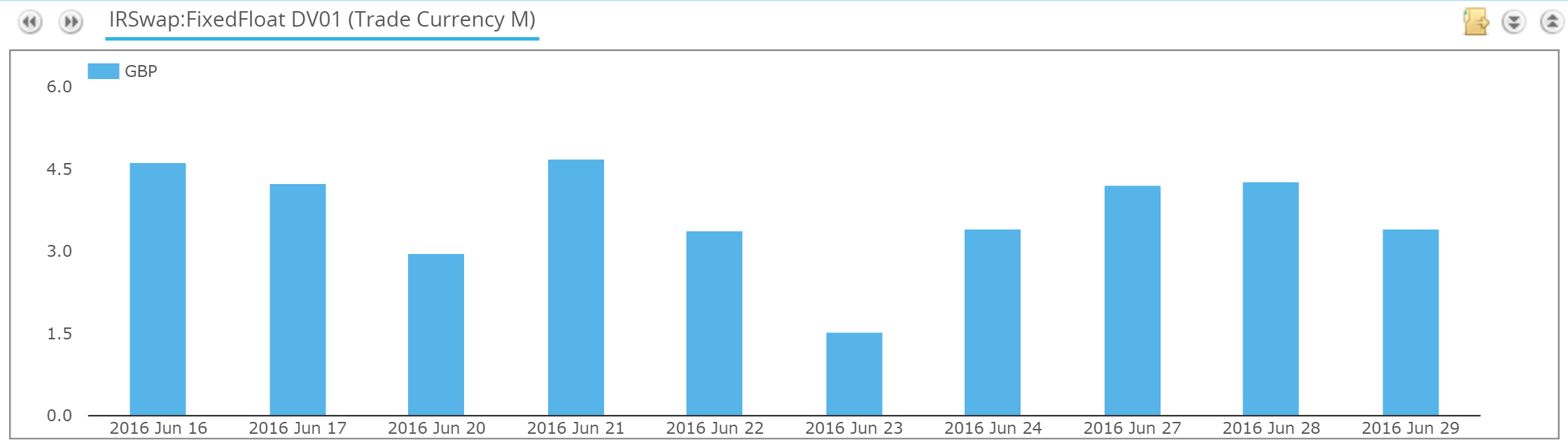

But it is well worth drilling down into those GBP IRS numbers (light blue bar). When we look at them in DV01 terms we see that yesterday had a very large amount of risk traded:

As the caption says, yesterday actually saw MORE risk go through in GBP swap markets than on any other day since the referendum. So whilst rates were remarkably stable throughout the day, markets were still clearly very busy. With 10 years closing at the 1.00% level and off its highs of the days, I’m guessing it doesn’t take a genius to work out that some of those late in the day flows were receivers.

The first GBP swap coming through to SDRs this morning is 4 years vs 3m LIBOR at 0.4607% in small (£5m). With the 3m LIBOR market less liquid than versus 6m, it’s not that easy to interpret what that means for the rest of the curve today – the previous trade in this structure was at 0.442% at midday yesterday. The best we can say from this trade is that Rates appear to be stable this morning with no huge moves from last night’s closes.

05:39 LON – USD Overnight Wrap

Swap markets appear to have been calm overnight. USD Swap rates are less than 1 basis point higher than last night, with only small volumes trading so far.

- Just 36 trades have been reported to the SDRs overnight

- A total notional of less than $1.5bn has traded

- Prices are stable

We’ve summarised prices and volumes below.

The breakeven forward between the 3¼% Jan 2044 gilt and the 4% Jan 2060 gilt (a forward 16 years wide) is about 0.77%. This is very low, which has one of several possible causes.

➊ For the 16 years starting in ≈27⅝ years, the economy will be sufficiently weak that short-term interest rate will average under 0.8% (after averaging about 2.43% for the 17½ years from July 2026 to Jan 2044).

➋ Investors are mistaken.

➌ Investors believe that this forward rate can be a hedge for present economic weakness, and hence assumes that bad news could lower the forward rate much further.

➍ Regulation or indexing prevents gilt investors from shortening from the 4%60 into the 3Q44.

You choose! (But I don’t believe ➊, dislike ➋, and there must be a limit to ➌. Regulatory incentives for cash-matching will impoverish future pensioners.)