Guest Blog Series

Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

Happily we are coming into the quiet summer time. As well documented, many market participants head to the beach for August and we expect to see a significant drop-off in liquidity and trading volumes as a result. Of course, that doesn’t mean we necessarily see a drop in volatility, as any junior trader left holding the fort back in August 2007 will attest – BNP money market funds threatening to break the buck and worries over Northern Rock in the UK were just two factors contributing to the 25bp spike in USD Libor that month.

But what also happens in August is that virtually every trader decides to re-write their spreadsheets.

Whilst we are all still hunting for the spreadsheet-to-rule them-all, often it is more important to have one that just works!

Old habits die hard, and August has been the perfect opportunity for me to look at the new Clarus SDRView API, and incorporate it into my spreadsheets. Being able to slice and dice the data “on-the-fly” is quite addictive – and has allowed me to re-write all of my old spreadsheets with real transactional data rather than fictitious screens.

Given this new found level of detail, I focussed on the most transparent swaps market we now have – USD Swaps. I hold my hands up and admit that I was fully expecting to see evidence of July’s 7year UST auction in the data. After-all, the 7 year tenor does not trade as a principal, therefore you would think we’d see some evidence of the $29bn auction, or at least of the $10.8bn taken down by Primary Dealers. Except for a higher than usual $3.4 billion 7Y on Tradition on 31-July (see SEFView), I’m still looking…..

So that got me thinking – if we can’t see enough evidence of a bond auction, but we can easily see evidence of issuance activity being swapped – is there any kind of evidence of a “non-professional” user base in these markets. Obviously, large trades are easy to find – but that should be because they are the exception, not the rule.

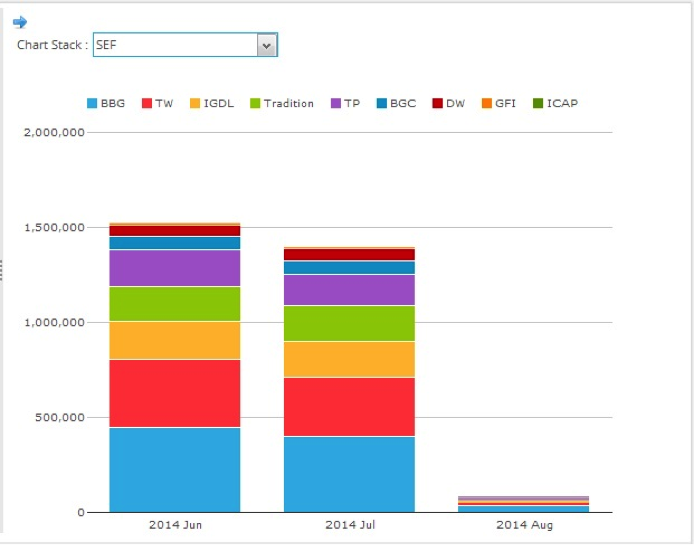

So we turn to one of the success stories of the Dodd-Frank ACT, Bloomberg SEF. We have a whole month of data for July for these so-called “customer” transactions.

From SEFView, we can see that BSEF made up around 27% by 5y-equivalents for USD swaps in July:

So what is the composition of these trades like?

If we were talking about the equity markets, we would be splitting the transactions into sub-100 “odd lots” as a start.

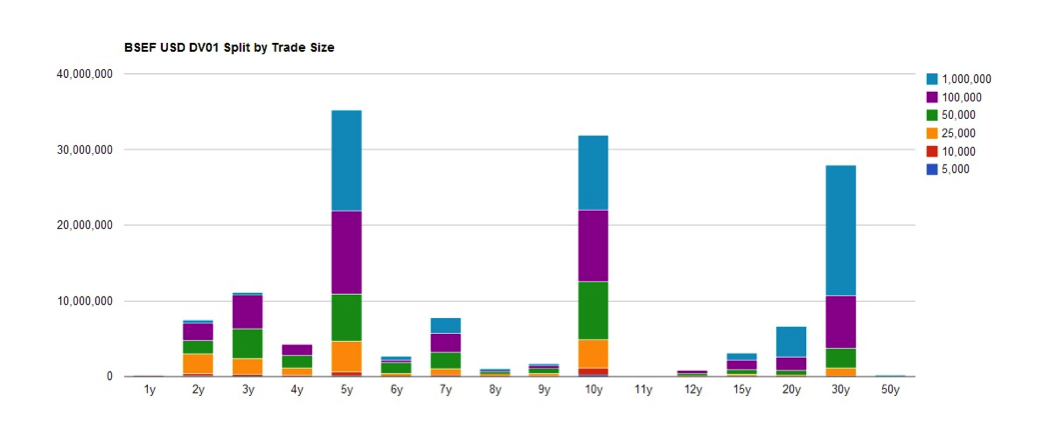

For the Swaps world, using the SDRView API, I’ve been able to split the trade universe into DV01 slices – trades less than 5k, trades less than 10k etc. The lack of homogeneity in our markets is once again striking:

We can again see how concentrated volumes are in the 5y, 10y and 30y areas – 67% of all DV01 is traded in these tenors.

However, the power of the API lets us analyse the exact composition by size:

- Small trades (less than 25k) are largely irrelevant in these markets, even in non-benchmark tenors.

- Large trades (100k plus) are typically capped in notional reporting terms as they break the block thresholds. Nevertheless, they make up a huge proportion of benchmark trades

- (It’s worth pointing out that BSEF seem to have some mapping errors on the block thresholds, as they have reported a $500m 20y trade on 30 July, hence the upper limit on my DV01 filter is $1m.)

- In the “long-end” (10y plus maturities), size matters. 63% of trades by DV01 are larger than 100k.

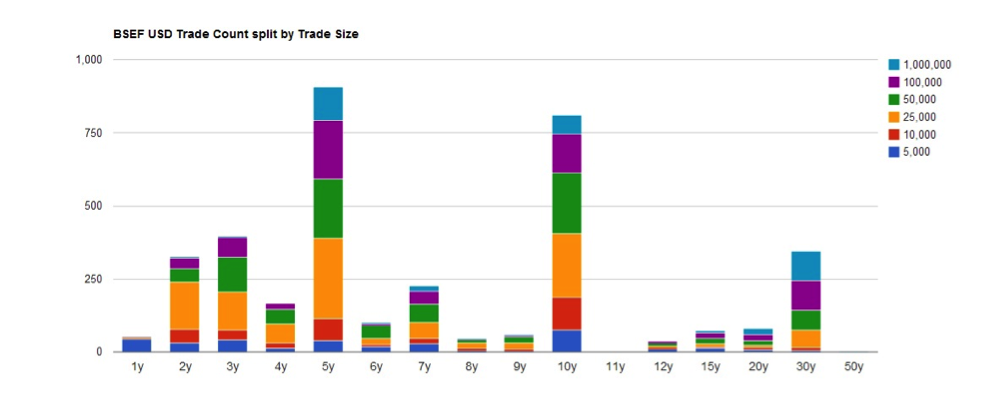

Performing the same analysis by trade count (much as the CFTC did originally) actually paints a different picture:

- We can see activity in the short-end (<5y), which struggles to even register on a DV01 basis.

- $25k DV01 is the most frequent trade size – i.e. it is fair to say this represents “market size” for trades shorter than 12y.

- $100k DV01 and larger is most frequently traded in the long-end.

- BSEF reported a total of 3,620 trades in vanilla USD Swaps for the month of July. Is that a large enough number of trades for wannabe market-makers?

I intentionally focussed the analysis on a D2C SEF to hunt for evidence of a “non-professional” market. BSEF should be the natural market-place that all of those vulnerable swaps market participants flock to – the transparent, electronic nirvana of Gensler’s dreams.

In reality, the numbers point to a market that is still the over-riding preserve of professionals, trading infrequently and in large size.

Given the state of the industry at the moment – low volatility leading to reduced trading against an ever-expanding cost base – perhaps it’s not surprising that market incumbents haven’t committed to instantly changing their behaviours.

However, as different sources of liquidity enter the market, the key question is which of the above graphs will they alter?

At the moment in USD swaps, 19% of the tickets contribute 2.4% of the total risk traded. In EUR swaps, 19% of the tickets contribute just 0.82% of the risk.

Maybe the change is actually underway?