FOW (Futures & Options World) recently published my article on US Swaps transparency. If you are a subscriber to FOW, you can view the complete article here.

Otherwise, the article is re-produced below.

_________________________________________________________________________________

The Dodd-Frank Act requires both the real-time reporting of all OTC Derivatives trades done by US persons to Swap Data Repositories (SDRs) and the real-time public dissemination of these trades. For the first time, anyone is able to see on any given day, what OTC Derivatives products trade, what price they trade at and in what size.

I cannot overstate the fundamental nature of this change. We have transitioned from a market where trades were private and a few privileged firms had insight, to a market where there is post-trade transparency for all.

Let look at how market participants use this new post-trade transparency.

Price Discovery

While there was and is a mass of indicative prices on flow products, we now have actual prices published within a few minutes of a trade being executed, for all product types from the thousands of Swaps that trade on a given day, to the hundreds of Swaptions and to the tens of Caps and Floors.

This data on actual prices is widely monitored by Brokers, Dealers, Hedge Funds and Asset Managers to assist in price discovery; either directly from the public dissemination pages of the SDRs (DTCC, BSDR, ICE, CME) or from consolidated views provided by vendors such as Bloomberg, Clarus and Thomson Reuters.

Volumes

However the real new insight is the size of the trade. This yields useful information on how price varies with size and is important to analyze for those firms that need to conduct large trades in the market.

Again such data is widely monitored using the above sources.

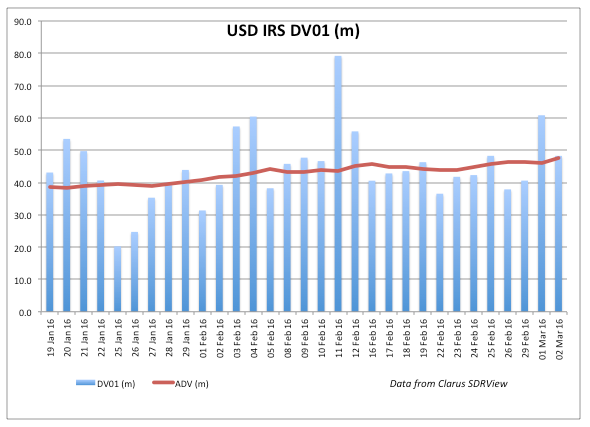

Liquidity

The size of each trade means we can now quantify liquidity by determining today’s volume and the average daily volume (ADV); measures common in Futures and Options markets, and do so in either in gross notional or DV01 terms (see picture).

Such depth of information is valuable in understanding liquidity in the Swap market and comparing this to the Futures market or the Treasury market, which is important given the inter-dependency of these markets.

Market Share

With the availability of public data, Brokers and Dealers no longer need to rely on imperfect information (often little more than gossip) to know their market share in a given product and currency. They can determine this daily, weekly or monthly by comparing their trade counts and notionals with the market and establish objective metrics to monitor performance.

Possible Future Uses

Lets now turn to possible future uses of the public dissemination data.

Compliance

A compliance function within a Broker or Dealer needs to conduct surveillance on its trades. This surveillance involves comparing your own trades to the market and looking for suspicious trades e.g. off-market prices.

Now that we have a source of all market trades, many of the same types of checks that are used for Securities and Listed Derivatives can be performed for OTC Derivatives.

Risk

A risk management function needs to perform independent valuation and risk assessment of positions entered into by its traders and to do so needs to purchase closing market data from suppliers of such data, namely brokers and vendors. By necessity much of this data has been both fragmented and indicative; so not based on actual trades.

Now that we have a source of actual prices and sizes for the whole market, this can be used to augment existing price sources and improve risk management.

Indices

A lot of ink and money has been spilt on LIBOR and ISDAFIX, with one criticism being that these are not determined by actual transactions. IOSCO Principles of Financial Benchmarks recommend that an index be anchored by observable transactions between buyers and sellers in the market.

By widely increasing the availability of such transaction data, it is possible that we may start to see new Indices develop and be used by market participants.

Final Thoughts

Our industry has invested many millions in implementing the regulation to report OTC Derivative trades in real-time to SDRs. To do so simply to see the data vanish into a regulatory black box does not seem to be money well spent.

However with real-time public dissemination in the US for all OTC Derivatives, we now have a similar level of transparency to that available in Futures and Options markets.

Such transparency improves price discovery and the efficiency of markets. Surely that is crucial in regaining investor trust and re-building volumes for the benefit of the whole industry.