Happy New Year everyone. My New Year has started by tackling 172 pages of FCA consultation – lucky me!

In Summary

- UK regulators are consulting on “Improving Transparency for bond and derivatives markets“.

- For Swap markets, this will now move post-trade transparency in-line with Clearing Mandates – if a swap is mandated to clear under UK rules, it will be report in public data.

- With a bit of luck, the outcome of the consultation will move volume disclosures for large trades (aka block trades) in-line with US rules, which have proven to be positive for swap markets.

- ISINs will continue, but will be supplemented with Start Date, End Date, floating leg spreads and the LEI of the CCP at which the swap is cleared (whoop!).

- Adoption of a “UPI”, which will also become part of US reporting rules, will also be introduced.

- The consultation runs to 60 questions (you don’t have to answer them all!) and we have until 6th March 2024 to submit responses. Please remember to include DATA in your responses!

Context

The UK rules for pre- and post-trade transparency were largely inherited from MIFID II post-Brexit. In case any of our readers are not familiar with MIFID II transparency – it doesn’t work. We have blogged repeatedly on it, and yet 15 years after the G20 “commitment” to reform OTC derivative markets, we still have no transparency in Europe. The US continues to set the gold standard for capital markets.

Fortunately, regulators in both the EU and UK are working on changing the current state of affairs. This blog tackles the FCA’s Consultation Paper CP23/32 “Improving Transparency for bond and derivatives markets”.

This is good because;

- Changes to the regime are certainly necessary and;

- No one wants to read another Clarus blog that moans about MIFID II!

Product Identifiers

Please listen to Amir at 3:23 minutes on our latest podcast to see what Clarus think of ISINs:

Fortunately, this Consultation Paper will now introduce some solutions by introducing :

“further data fields to deal with…limitations of identifier(s) for transparency purposes. Speaking with market participants, we believe these data fields should include:

FCA CP23-32, Page 66 https://www.fca.org.uk/publication/consultation/cp23-32.pdf

- the concept of tenor and effective date (equivalently, effective start date and

expiry date)- spread on the floating leg of IRSs

- upfront payments forming part of CDS transactions

- identification of the clearing house in which the instrument is cleared

We encourage all of our readers to respond in the affirmative to Question 45: Do you agree with our proposal to introduce the additional data fields enhancing the UPI to identify an instrument? Yes, Yes and Yes.

Deferrals (and liquidity)

At the moment, the combination of liquidity assessments, deferrals and flags all contribute to the MIFID II data problems. To improve the quality of the data, it is important that the data is published in a timely manner – the current deferral of four weeks for most swaps data is just too long (89% of notional in vanilla EUR IRS was found to be reported with a four-week delay!).

The FCA paper wants market participants to consider two new deferral regimes:

- LIS (i.e. large block trades) will be delayed by 15 minutes, with the full-size disclosed at the end of the day. If a trade is really big, then a second LIS threshold will be triggered, which will further delay the publication of the size & price to T+3. This is “model 1”.

- Alternatively, LIS trades are delayed by 15 minutes, with their volume published only up to the LIS threshold. This is “model 2”.

Model 2 is the same as the US model (with UK-calibrated LIS thresholds). Seeing as Model 2 has been live, is working, and has improved swap markets in the US, I am betting that market participants will end up most enthusiastic about Model 2.

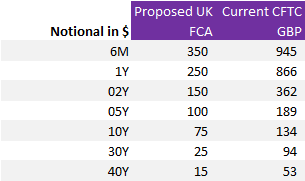

It is also worth noting the relative size of the proposed LIS thresholds in GBP markets compared to the existing Block Thresholds in the US (which will change in about a year. Maybe.)

Scope

From the perspective of OTC derivatives and the Clarus blog, I think the only other relevant part of the consultation is that the scope for transparency will change. All of the changes look at post-trade transparency – aligning with the US, where there is no concept of pre-trade transparency for OTC swaps. And the FCA very sensibly propose removing any requirement to make a Liquid/Illiquid assessment (which remember led ESMA to declare that the whole of the FX asset class was illiquid!).

Instead, the Consultation Paper states that:

The transparency regime should focus on derivatives that are cleared. Pricing information for cleared transactions is comparable across execution venues including those executed bilaterally OTC. We propose to exclude .. derivatives that are not subject to the UK clearing obligation.

CP 23-32, https://www.fca.org.uk/publication/consultation/cp23-32.pdf

As if they expected a Clarus blog on that very subject, the consultation almost immediately states:

We recognise that by using the classes of derivatives subject to the clearing obligation as the starting point for the transparency regime we may exclude other derivatives that may be relevant in size or important from a market integrity perspective.

CP 23-32, https://www.fca.org.uk/publication/consultation/cp23-32.pdf

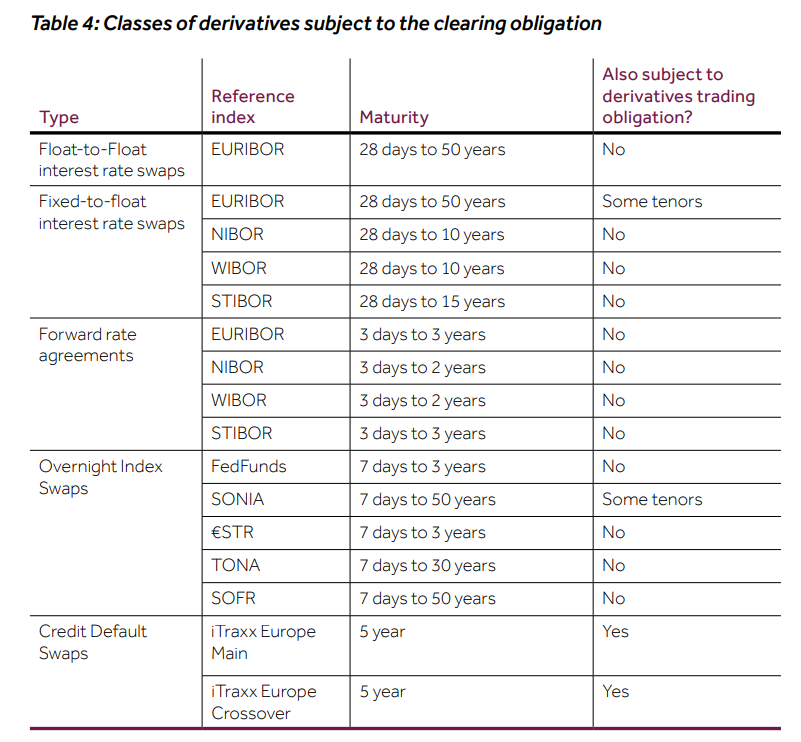

For those needing a reminder, it means that these swaps will be covered:

My concern about this scope is very simple:

- In an RFR world, we do not use IRS trades to monitor stresses in credit markets. The swaps are all cleared and do not reference credit-sensitive rates.

- In times of stress, we are very thankful for transparency data to prove that markets are still functioning.

- But in times of stress, we need price data regarding what is happening to credit spreads. Derivative markets, via cross currency basis spreads and implied basis from FX Forwards, are pretty much the only “credit stress” barometer that we have.

- Yes, CDS spreads help, but these are long-dated instruments. In times of stress, it is the immediate 3 months that you care about.

- There is no sign that Cross Currency Swaps or Swaptions have suffered from post-trade transparency.

Needless to say, we will also struggle to work out what proportion of markets are cleared if we have no post-trade transparency for uncleared markets. I hope regulators are ready to publish monthly summaries from their own reg data!

Ultimate Goal

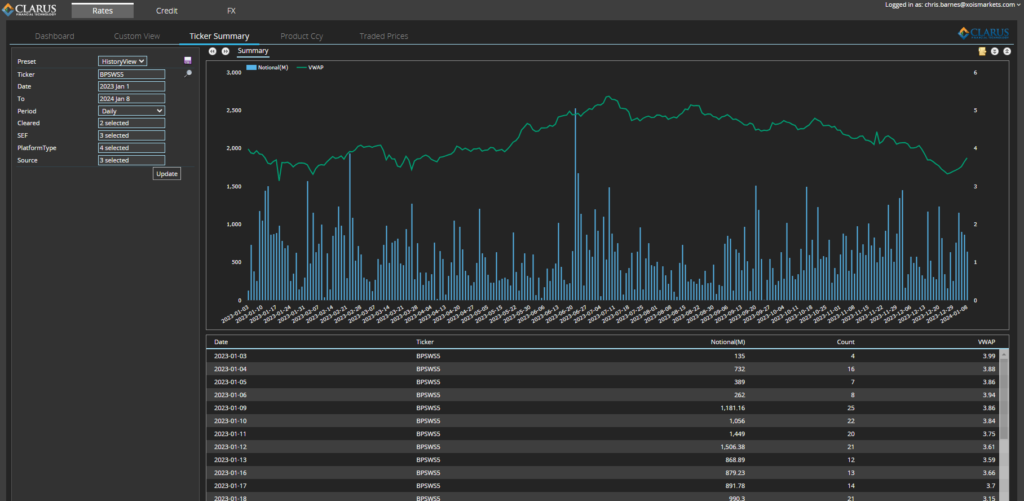

Regulators, market participants and Clarus are pretty much aligned on the end goal here – to be able to produce something very similar to our “Ticker Summary” for widely traded OTC derivatives, such as GBP 5Y swaps, represented by the BBG Ticker BPSWS5 below:

This consultation paper is a good start and we really hope it serves to clean up the data.

We then look forward to being able to get our hands dirty on actually using the data (which will take further changes further down the line).