Amended 7th October 2020 to correct the changes to block and cap thresholds to 67% and 75% respectively.

- The block threshold for Swaps, and all other OTC derivatives, is changing.

- The thresholds for trades qualifying for block status and the reporting cap for notional amounts are also diverging.

- This will substantially increase transparency in the SDR data.

- Block Trades (and capped notionals) will continue to be reported in 15 minutes, with no change to the delay granted to these large trades.

- We have to wait 30 months for these changes to come into effect.

The CFTC

Two week’s ago, at their 17th September meeting, the CFTC rejected a change to the current block trading deferral period for swap trades. Large swap trades will continue to be publicly reported 15 minutes after execution. The proposed rule to extend this period to 48 hours was rejected.

Anyone who read our consultation response (or our blog) will know that we at Clarus were very worried about the potential loss of transparency a 48-hour delay would have caused. So this new ruling from the CFTC is very much welcomed in these parts. The Chairman’s accompanying remarks say it all:

As I noted when these rules were proposed in February, “data is the lifeblood of our markets.” Little did I know just how timely that statement would prove to be.

Justice Brandeis famously wrote in advocating for transparency in organizations, “sunlight is the best disinfectant.” … The final swap data reporting rules enhance transparency to the public of pricing and trade data…. These changes will enhance market transparency by applying a stricter standard for blocks and caps, thereby enhancing public access to swap trading data.

Statement of Chairman Heath P. Tarbert in Support of Final Rules on Swap Data Reporting

I like the idea that Clarus now sell sunlight for derivatives markets. Maybe we have a new tagline coming?

What Are The Current Rules?

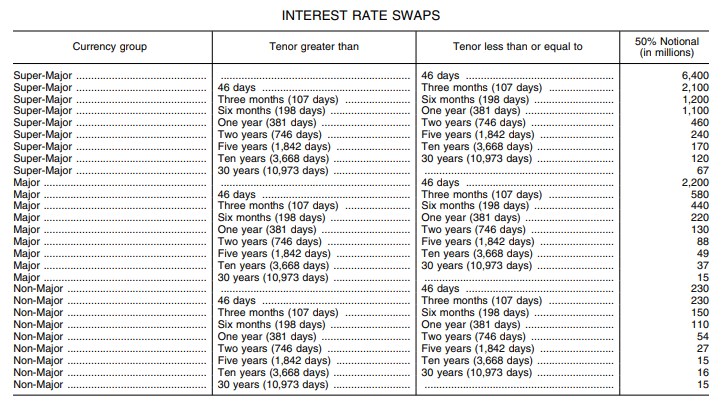

For the sake of completeness, the current block thresholds can be found on Page 78 here. These define both the block threshold and the capped notional amounts. Above these sizes, swaps publicly reported to SDRs have their notional amounts capped.

FIA also provide a good overview of the block regime (and “large notional off-facility swaps”) here.

Trades above these thresholds are reported with a 15 minute delay.

What Are The New Rules?

Of key importance to my mind are:

- Part 43 data, which is the public trade reports that we use to power SDRView, will now see higher block thresholds. Currently, about 50% of notional is above the block thresholds. This will change. In the future, trades that are above a 67% threshold will qualify as block trades. In addition, the reporting cap threshold is moving to 75% of total notional. Therefore, 75% of total notional transacted will be transparent, with 25% remaining “dark”. The reporting delay will remain at 15 minutes for block trades.

- Part 45 data, which is the private data the CFTC receives and is not disclosed to the public, will now also include data on uncleared margin. As we have discussed, we hope that one day this can be promoted into public data as well.

- Part 49 data will also change, but this all seems to be at the SDR end, so I haven’t kept on top of these changes.

The changes to the block thresholds are somewhat confusing (I got them wrong on the first edition of this blog). To be clear, the new rules mean that block sizes and capped notional amounts are diverging. Currently, the cap and block sizes are the same. They are calibrated such that 50% of total notional (across all swaps – see below) is immediately published.

This will change. The Block Size will be calibrated such that trades larger than 67% of notional will be counted as blocks. However, the cap threshold will move even higher, to be calibrated at 75%. This means that the full size of some block trades will now be disclosed (those trade that are above the block threshold but below the cap threshold).

When Are the New Rules Coming into Effect?

In a well-judged bout of rule-making, it turns out that the changes to Part 45 data will also impact the new Part 43 block thresholds. Parts of the Part 45 private data are going to become more standardised, which in turn will make it easier for CFTC staff to analyse the data.

This will impact the Part 43 changes, because the block thresholds are calibrated using Part 45 data.

What all this means is that there must be a phase-in period for Part 45 changes, followed by one year of quality data to recalibrate the block thresholds.

Therefore, while the changes to the rest of part 43 rules will have a compliance period of 18 months, the new, post-initial block and cap sizes, calculated according to the 75-percent notional amount calculations, will have a compliance date of one year after the 18-month compliance period (for a total of 30 months).

Federal Register: 17 CFR Part 43 Real-Time Public Reporting Requirements

So readers I wouldn’t hold your breath. We are 30 months (2.5 years!) away from actually changing the block thresholds.

How Much More Transparency Does This Mean?

We cannot calibrate the new thresholds ourselves, because the methodology prescribed (page 75) requires full transparency over all trade sizes in the SDR:

- Calculate the total notional amount of SDR trades within a swap category for the past year and multiply this total by 75%.

- Order all SDR transactions in order from smallest to largest.

- Take the cumulative sum of all notional amounts until the 75% limit is reached.

- The size of the trade breaching the 75% threshold is the new capped notional threshold.

For calculating block sizes, the same methodology is used, but using 67% as the calibration criteria.

With our current data, we do not know what the distribution of trades is like above the block thresholds.

However, we should (roughly) be able to calibrate our old totals with the new totals. Roughly speaking, we would expect to see SDR notional amounts increase by 25% when the new capped thresholds are calibrated in 30 months time.

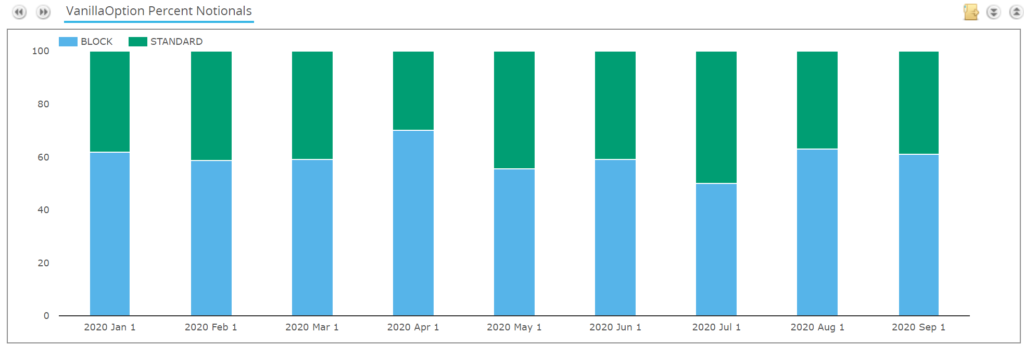

The rule changes are across the board, for all classes of OTC derivatives that are publicly reported. The recalibration should be significantly greater for some asset classes, such as FX Options. Depending on the reliability of the newly standardised Part 45 data, we should avoid the crazy situation we see right now where 60%+ of FX Options (in USD vs Asian currencies) are reported as block trades:

In Rates, recall from our previous block trading blog that it is only Tradeweb and Bloomberg who are able to classify trades as “Block Trades”. However, the new calibration regime will also impact the capped notional amounts reported by SEFs running CLOBs (i.e. the D2D market) and therefore will cause reported volumes across the whole of the SDR to increase.

It’s just a shame we have to wait 30 months for the changes to come into effect!

In Summary

- We are very happy to see that the majority of the industry rallied behind transparency in derivatives markets and chose to reject the proposed 48-hour delay to block trade reporting.

- A simple deferral regime is a good deferral regime. The 15 minute delay in block trade reporting has served the industry well so far.

- We encourage Europe and the MIFID II review to take note of this important transparency rulemaking in the US.

- The transparency in the SDR data will substantially increase once the thresholds are raised from 50 to 75% of total notional.

- There is now just the small matter of a 30-month wait for these changes to take effect!