As references to Libor declines ahead of 2021 and the use of Risk Free Rates (RFRs) increases, derivatives will have to adapt. So in this blog I will look at the cross-currency swaps and the choices needed to move to RFRs.

Cross currency swaps can behave quite differently to single currency swaps and I will present a number of options for users in the future. The conventions of two currencies can sometimes cause differences in payment timing, rate fixing dates and notional exchange.

This blog looks at the various options and how they may become part of the RFR-based cross currency swaps.

The current cross currency markets

Cross currency markets have evolved to follow the interest rate conventions of the individual currencies with the added component of notional exchanges on the first and maturity dates of the swap.

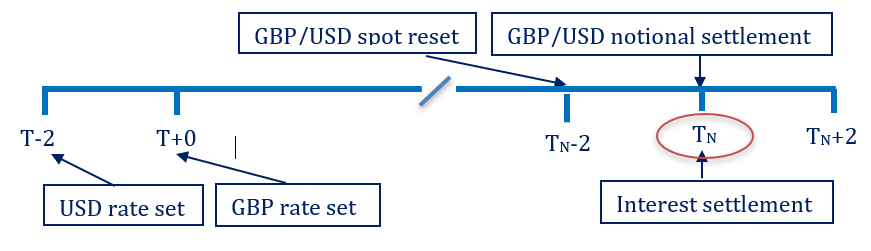

For example, a GBP/USD cross-currency swap referencing Libor (showing a single leg, part way through the swap so the initial and final notional exchanges are not shown) would look like this:

As per the Libor conventions, the USD Libor sets 2 business days before the relevant period (T – 2) while the GBP Libor sets on the first day of the relevant period (T + 0). Market participants who have managed this mis-match for many years are quite familiar with this feature. This also occurs in many other currencies where the two interest rate legs set Libor (or IBOR) on different days.

Interest settlements are on the final day of the relevant period (TN).

Another feature of the cross-currency swap is the notional reset at the start of each period. The above diagram shows the notional reset dates for the following period to show how they align with the interest payments from this period.

Many cross currency swaps are dealt this way to reduce the impact of the cheapest-to-deliver collateral on the swap pricing. And how does this work?

The spot rate is set at TN – 2 and the notional is adjusted at TN with a payment in one currency to set the swap PV to zero. This means the cheapest to deliver calculation is only over that quarter and the impact of the forward valuations is minimal.

The red circle shows the day on which both the interest and notional settlements occur.

Although most dealer-dealer swaps are done with notional resets, it is more common for end-users who are using the cross-currency swap in a hedge accounting transaction to not reset the notional.

Cross currency swaps with RFRs

With the very likely cessation of Libor sometime after 2021, the cross-currency market like their single currency one, will move to RFRs to replace Libor and other IBORs.

The use of RFRs presents us with some interesting challenges and decisions. The final rate is not known until the end of the relevant period if the ‘compounded, settled in arrears’ methodology is used.

Each of the two currencies can often have a different payment lag defined for the single currency swap. For example, USD uses a 2 day lag while GBP employs a 0 day lag. (See OIS Swap Nuances).

This means that if you align the rate set dates for the GBP/USD cross-currency swap legs then the payment dates inherited from the single currency OIS swap definitions will not occur on the same date!

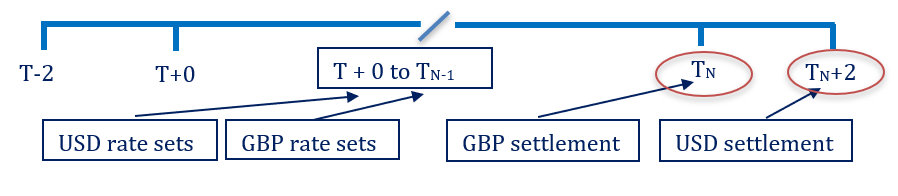

For a single leg (as shown above in the Libor-based version) the interest payments for the RFR look like this:

The red circles show the 2 different settlement dates for GBP and USD interest payments.

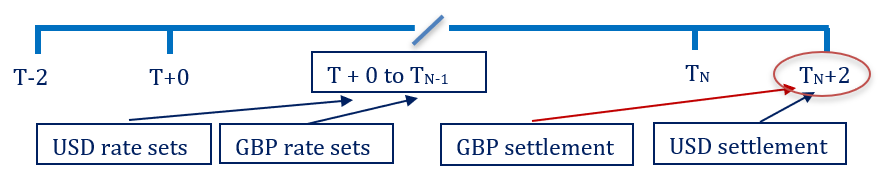

But market practice could set the payment dates to the date determined by the currency with the longest lag like this:

The GBP settlement (red arrow) has now been moved to TN + 2 to align with the USD payment and both settlements now occur on the same day (red circle).

The notional reset dates

Now we have successfully made sure that the interest payment dates are on the same day (2 days after the end of the relevant period; TN + 2) we now have to look at the notional reset payments.

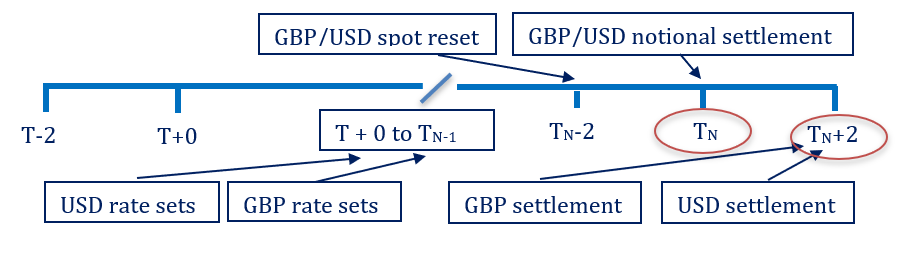

The notional reset payment dates are on the first day of the relevant period for the Libor-based swap. This means they are now on a different day to the RFR-based interest payments.

The new spot rate is set 2 business days before each relevant period starts to align with FX market conventions. The actual reset occurs on the first day of the relevant period which is before the interest payments (usually 2 days later).

In this case, the payments cannot be netted (interest and notional) which can add additional payment dates and potentially credit issues.

The cross currency RFR swap now looks like this (after moving the notional reset to the next leg):

The two settlement date (red circles) are now on different days.

Potential ways to align payments

The interest and notional payments can be aligned but this does imply some changes to reset days.

1. Change the interest reset days

With the typical 2 day payment lag for compounded, in arrears interest payments the relevant period for the RFR resets could be moved 2 business days earlier so the actual interest payments occur on the last day of the relevant period.

This may be a solution but any single currency interest rate hedges would also need to be moved 2 days earlier to line up properly.

This can cause operational and trading issues.

2. Change the notional reset days.

The alternative is to reset the spot rate for the notional exchange on the first day of the relevant period rather than 2 days prior. In this case, the payments would align but, like the interest rate changes, this can create complex operational issues for some users.

Either option would solve the problem but both deviate from the current conventions in OIS trading or Libor-based cross currency swaps. This would make one-to-one matches for cross currency swaps across Libor and RFR impossible.

Summary

The inevitable transition from Libor to RFR based cross currency swaps will present a number of challenges including the alignment of payments.

These will have to be resolved soon to avoid confusion and potential re-booking of swaps once conventions are adopted by the market.