In January 2020, the ARRC published the final recommendations for cross-currency swap conventions. It should be noted that the recommendations are primarily directed towards dealer-dealer trades and the publication points out that dealer-end user trades may require different structures.

I have commented previously on potential options in AUD markets and more generally for other currencies. Since last year many changes in RFR markets have meant that an update to the previous blogs is timely as markets start to concentrate more urgently on the end of LIBOR.

Which currencies are most impacted?

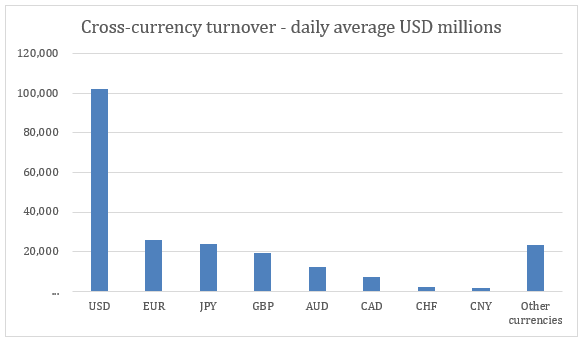

The chart below is from the BIS Triennial Survey 2019 and shows the average daily turnover per currency in millions of USD.

As expected, USD dominates the turnover as a majority of cross-currency swaps have USD on one leg due to markets being most liquid against USD.

The large turnover in LIBOR-related legs (USD and GBP) will definitely be impacted soon as market participants look to reduce the risks associated with a LIBOR cessation event.

This suggests the conventions need to be finalized so that markets can start to trade efficiently referencing RFRs instead of LIBOR.

EUR, JPY, AUD and CAD also feature in turnover. Despite the likelihood that the benchmarks associated with the cross-currency swaps will persist for some time in these currencies, nevertheless new fallbacks will have to be added to remain consistent with ISDA changes.

What is very evident is that USD will need some changes very soon. And this change to the dominant currency will drive further decisions on other currencies represented as the other leg of the swaps.

Fallback vs OIS Swaps

One aspect of the changes referenced in the ARRC recommendations is the alignment of the fallbacks with the existing OIS OTC market practices.

The OIS markets generally trade on a ‘payment delay’ basis where settlements occur 1 or 2 days (depending on the currency) after the final date of the relevant period. This delay allows for the alignment of the rate fixing dates to the actual days in the period (with the final rate known 1 day after the end date) while still giving sufficient time for settlements to be effected.

Fallbacks work quite differently; they employ a ‘2-day backward shift’ methodology. Although this aligns well with the LIBOR rate fixes in some currencies (e.g. USD) it can be problematic for other currencies (e.g. GBP) where there is no lag between the rate fix date and the start of the period. The standard 2-day backward shift is likely to be used for all currencies (as per ISDA’s previous consultations) so that settlement can be made in a timely manner.

In the fallbacks, this difference in the rate fixing dates for some currencies will require deft adjustments to the calculation of floating rates and how they will replace LIBORs and other IBORs.

Also, the fallbacks will not directly align with OTC OIS markets and adjustments will be required when using OIS swaps to hedge cross-currency swaps using the fallbacks.

Could there be a difference betwen new cross currency swaps and legacy swaps?

Potentially yes, there could be a difference depending on the new market conventions.

Put simply, is there more support for aligning the RFR-based cross-currency market conventions to the existing, underlying OIS markets? Or is there more aptitude to align with the LIBOR fallbacks?

The former means a payment delay convention would apply across both markets with associated changes to the FX reset date convention.

In the latter case, market dealers could be more inclined to align cross-currency swaps with the fallback changes where the 2-day backward shift is preferred?

Either way, the general difference between OIS swaps and fallbacks will have to be considered in the near future.

| Swap | Rate fix convention | Settlement |

| OIS single currency | Zero backward shift | 1-2 day delay |

| Cross Currency | 2-day backward shift | Zero delay |

Options for existing trades

Apart from new trades, all market participants with existing cross-currency swaps should be considering the options for amending the fallbacks. These include:

1. Double trigger

While USD dominates cross-currency swaps turnover, there is a second, non-USD leg to consider. If the other currency is not a LIBOR currency, then it will most likely not trigger the fallback at the same time as USD.

In this case, counterparties may decide to include a double trigger which forces both legs to revert to the fallbacks if one side is impacted.

2. Fallback to Term RFRs

Term RFRs have been described previously in blogs here and here. The Sterling Working Group has started work on establishing a viable Term rate which is well underway now. The ARRC has brought forward the time for a USD Term rate to 2020.

While these rates are still in development, the exitance of the Term rates offers an alternative for dealers and end users who have expressed concerns about operational challenges of using the standard fallbacks.

3. Move directly to RFR based cross currency swaps

Once the markets for new cross-currency swaps is established, some counterparties may decide to simply amend existing swaps to reference the RFRs without waiting for a fallback trigger.

Although this is an attractive alternative, care needs to be exercised especially where hedge accounting is attached to the swaps.

The options above are not an exhaustive list but should prompt counterparties to consider the alternatives to just accepting a standard model for changing the fallbacks to LIBOR and other benchmarks.

Options for new trades

Dealers will have to agree conventions very soon so the viable interbank cross-currency markets based on RFRs can develop.

Consistency in the conventions and transparency in quotes available to markets and end-users is essential for pricing and revaluation.

The ARRC recommendations are quite numerous and I really encourage you read them in detail. There are a number of options for the RFR cross currency markets which will be important to fully consider when establishing conventions.

One of the more important decisions will be on the ‘standard’ quoted price. Will it be RFR-RFR where these markets are viable (e.g. USD/JPY)?

Or will it be RFR-IBOR even where there are two benchmarks (e.g. USD/AUD where both AONIA and BBSW will co-exist)?

One of the key factors in making the decision (possibly per currency pair) is the relative volatility of the basis swap. In general, RFR-RFR basis volatility is lower than RFR-IBOR volatility: this could be the deciding factor. This is a foundation decision which will greatly impact the future trading of cross-currency swaps

SOFR development in USD

So how is SOFR growing? We have commented on this in the Clarus blogs so many times over the past year it is impractical to mention them here.

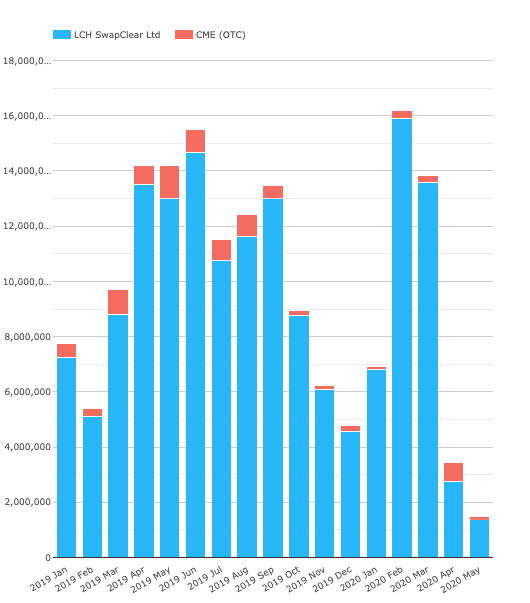

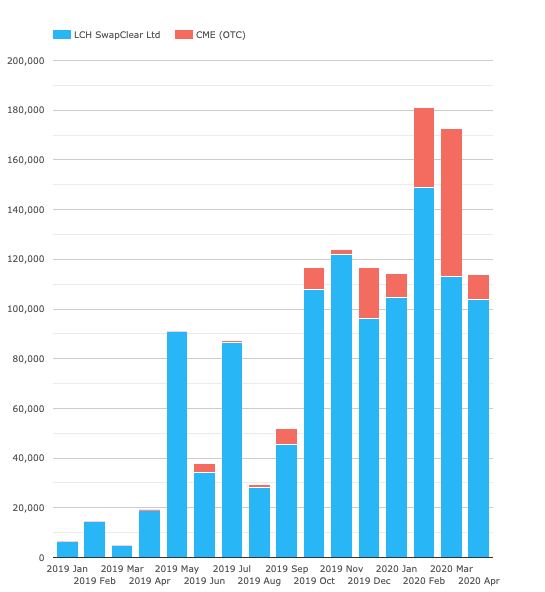

But, looking at CCPView again I have reproduced the following charts:

(From Jan 1, 2019 to May 8, 2020)

Just focus on the vertical axis in both charts: the total OIS is 100 times the SOFR OIS indicating EFFR dominates OIS trading.

SOFR trading will have to increase significantly before cross-currency markets can confidently move to referencing it as the new benchmark.

Summary

The ARRC recommendations for cross-currency dealer-dealer swap conventions have been released and are ready for markets to adopt and make decisions on the preferred approach.

While there are several options for how the quoted markets develop there are some important considerations for how legacy swaps adopt the new fallbacks and how these, in turn, will be able to integrate with the new market conventions.

But the slow development of SOFR as a dominant reference rate will continue to slow the transformation of the cross-currency markets.

Part of the issue is the “Final Recommendations” still leave a number of questions/options on the table. So once again it will be down to the market to decide on conventions, likely through “majority wins” in terms of executed volumes through the brokers. We have seen this process in the FRN space where it seemed like consensus had been reached in the SONIA space, until backward observation shift raised its head. I think it will be some time before we see a clear consensus on conventions for interdealer RFR-RFR xccy basis swaps unfortunately.