ISDA have launched a consultation for a fallback mechanism in the event that a LIBOR rate ceases to be published. This would mean that any contract referencing the LIBOR rate and governed by the ISDA 2006 Definitions would use these proposed “fallback” rates.

How Will it Work?

The consultation document states that fallbacks will be defined in a “Supplement” to the original ISDA 2006 Definitions (although remember that I’m not a lawyer!). From the docs:

The consultation document states that fallbacks will be defined in a “Supplement” to the original ISDA 2006 Definitions (although remember that I’m not a lawyer!). From the docs:

ISDA expects to publish a protocol to facilitate multilateral amendments to include the amended floating rate options, and therefore the fallbacks, in legacy derivative contracts.

Before we even start thinking about protocols to change contracts, we need to first understand the fallback mechanisms and how they are calculated.

ISDA have therefore launched a consultation to allow market feedback on 4 possible approaches to fallback rates. The current consultation states:

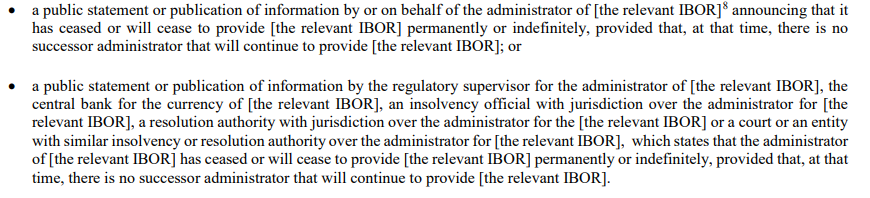

- Fallbacks apply if the “IBOR” is “permanently discontinued”.

- The fallback rates are all based on RFRs – see our blogs on Libor reform to catch up on the assorted Risk Free Rates across multiple jurisdictions.

- The current consultation applies to GBP, CHF, JPY and AUD. But can we really imagine that USD and EUR (Euribor) will reach different conclusions?

Permanently Discontinued

It’s probably worth acquainting ourselves with the text that defines what triggers the use of a fallback rate. From my reading, the fallbacks are triggered if anyone with the authority to do so (including regulators, central banks or the benchmark administrators themselves) publicly announce that it will cease to publish (even indefinitely):

The fallback rate will only come into effect once the rates stop being published – which may be after the announcement date. Much like happened with the TOIS fixing in Switzerland, I guess we could see a situation where the “market” somehow agrees on a convenient date to stop publishing.

The fallback rate will only come into effect once the rates stop being published – which may be after the announcement date. Much like happened with the TOIS fixing in Switzerland, I guess we could see a situation where the “market” somehow agrees on a convenient date to stop publishing.

OIS plus a Spread

Onto the actual fallbacks. They will be made of two components:

- Libor is a term rate (e.g. for 3 months). RFRs are overnight rates (i.e. for one day). We must decide how we should relate an overnight rate to a term rate.

- Libor includes a “credit spread” because it is where other banks will offer to lend to other banks. What this “spread” exactly incorporates (credit, term premium, liquidity) is not the subject of the consultation, but rather how we should calibrate the spread.

Let’s get the easy bit out-of-the-way first – the RFR term rate.

Adjusted RFRs

To relate the RFR overnight rate to a term Libor rate we must “adjust” the RFR rate so that it makes sense. ISDA proposes four options. We think that the market will probably choose option 2 or 3 below:

- Spot Overnight Rate. The RFR rate on the fixing date of the Libor becomes the fixing for all Libors. Libor has naturally been a forward looking rate, so I’m not sure this will garner much support.

- Convexity-adjusted Overnight Rate. Compound the RFR rate by itself to create a “simple” term interest rate.

- Compounded Setting in Arrears Rate. The RFR is observed over the relevant tenor and compounded daily. This clearly makes sense.

- Compounded Setting in Advance Rate. The observation period for the RFR ends before the fixing date and is applied to a subsequent period. Again, Libor has naturally been a forward looking rate, so I’m not sure this will garner much support.

Whether the market choses option 2 or 3 will depend upon how we calibrate the term spread. Let’s have a look at the options.

Spread Adjustment Methodologies

The goal here is to calibrate a rough proxy for the spreads that are inherent in Libor rates relative to RFRs (after all, OIS vs Libor basis is far from zero – see our blogs). So to be clear, the final fallback rate would be the Adjusted RFR plus the Spread.

1. Forward Approach

The Libor and RFR curves are bootstrapped together, and the spread between the two curves at every single date in the future is calculated. This would entail ISDA agreeing:

- A single curve build methodology with the market (probably not too hard).

- A consensus for the source of market data. I imagine this will be somewhat harder.

- Some type of agreement from the publisher of market data that they will continue to publish rates so that this remains a valid fallback option. This sounds the trickiest part.

I think that this is a great idea, and in practice is what should happen when portfolios are actually ripped up and transferred to RFRs. The Adjusted RFR would have to be consistent and hence be the Compounded Setting in Arrears Rate.

Hopefully the market can try to get around the inherent problems of sorting out market data to make this possible.

2. Historical Mean

A look back period of 5 or even 10 years is used to calibrate the average realised spread between the RFR (or adjusted RFR) and IBOR prior to the demise of the fixing. To prevent there being a huge disparity between where the current market is and where this historic spread is calibrated, there would be a transitional period of one year. At the start of this transitional year, the fall-back rates would be set at the spot IBOR/RFR spreads, and then gradually converging (linearly each day) towards the long run 5 or 10 year average that would apply from the end of the one year transition period.

If this approach curries favour amongst the market, then we should see Libor-OIS spreads converge to their e.g. 5 year averages from now until 2021. It will make trading short-end basis extremely complex into 2021 and beyond as the pricing of any monetary policy changes must be balanced against the chance that an IBOR rate ceases to publish. It’s difficult to say where the most concentrated positions in pure Libor-OIS basis are – short end or long-end? This approach would see the least amount of value transfer from long-end positions but could mean that short-end trading becomes extremely complex.

3. Spot-Spread Approach

As you were for the Historical Mean, but instead of using an average or employing a transitional period, the spread between the Libor fixing today and the adjusted RFR for the relevant period would apply from this point forwards.

This is a huge event risk as it may be observed only on a single day (or maybe over a 5 or 10 day averaging period). Depending on the term structure of the Libor-OIS basis curve, this could see huge value transfer for long-end positions, as well as creating exactly the same complexity for short-end trading. I don’t see any positives of this approach over approach number 2.

Timeline

ISDA will augment the consultation with some data at the end of July. Responses to the consultation should be submitted by Friday October 12th.

What happens if counterparties don’t submit to the protocol, I’m not clear on at all. But the idea behind this consultation has to be that we come up with the most workable and realistic solution to the legacy LIBOR problem. From our initial read, we think that looks like an RFR set in-arrears plus a Forward Spread. Let’s see if the market agrees.

UPDATE August 20th 2018: ISDA just added 81 charts (count ’em!) to the consultation. They can be found here.