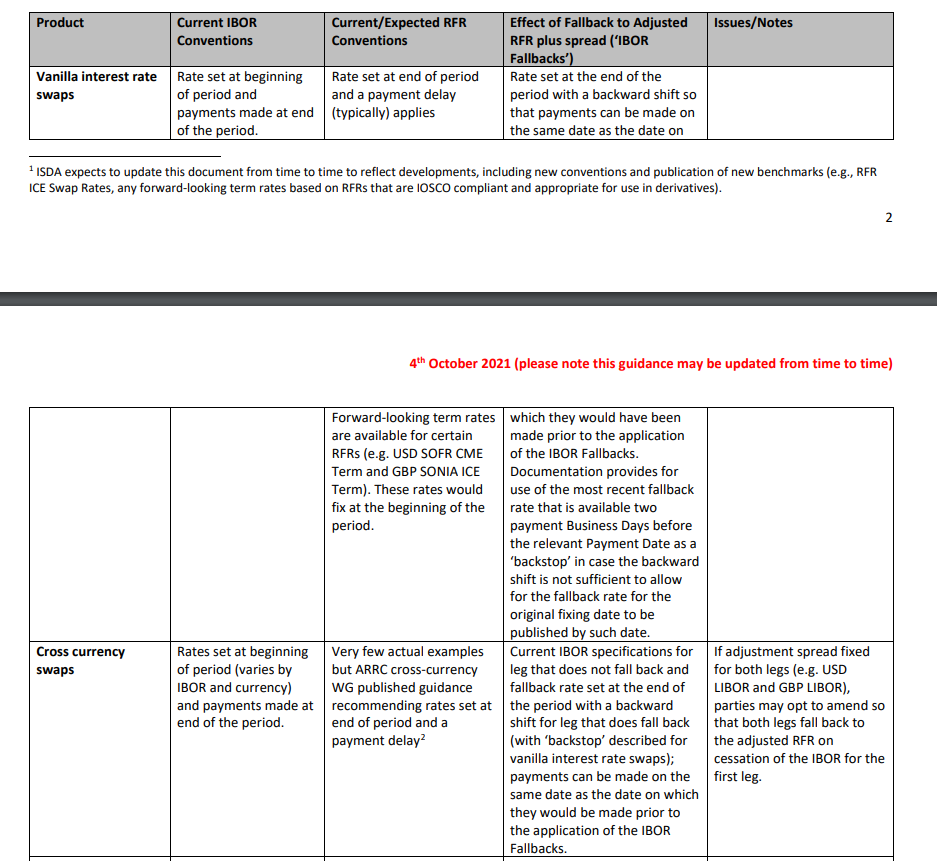

- Cross Currency Swaps exchange a funding position in one currency for a funding position in another currency.

- Markets have transitioned to trading RFR vs RFR since September 21st 2021 in three major currency pairs.

- The interbank market continues to trade a resettable floating-floating swap, incorporating a USD cash payment to reset the mark-to-market close to zero at each coupon date.

- We define the precise dealer-to-dealer market conventions for RFR vs RFR XCCY swaps.

- SDR data from US markets shows that 95% of cross currency swaps now trade as RFR vs RFR.

Maintaining Market Standards

I opened an email from ISDA with dismay earlier this week. Entitled “RFR Conventions – Product Table” I got excited that someone had formalised the process we use to create some of our most widely read blogs such as:

- OIS SWAP NUANCES

- MECHANICS OF CROSS CURRENCY SWAPS

- MECHANICS OF ASSET SWAPS AND GOVERNMENT BOND SWAP SPREADS

Obviously we try to keep on top of these things, but with the whole market moving to RFRs, there are a lot of Clarus Blogs out there that we really need to revisit and recast in an RFR world. I thought that ISDA had stepped in (hoorah!) but unfortunately the entry in the table for Cross Currency Swaps was quite disappointing:

“Very few examples” of Current/Expected RFR conventions for XCCY swaps??!! Let’s put that right today on the Clarus blog!

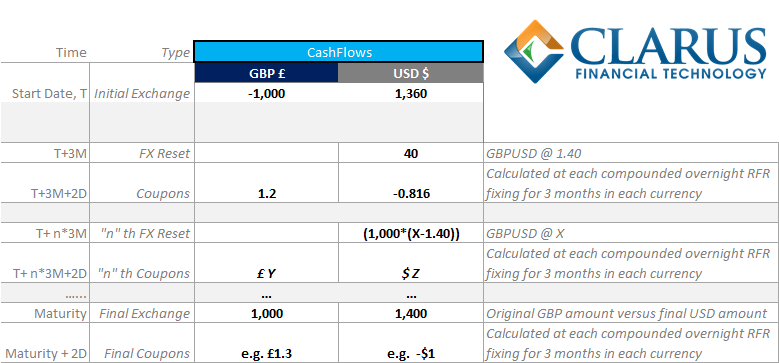

RFR vs RFR Conventions for Cross Currency Swaps – D2D Markets

As we wrote about in our LIVE BLOG: RFR FIRST IN CROSS CURRENCY SWAPS, Cross Currency Swaps have seen a particularly successful transition since September 21st. We’ll show you fresh data at the end of this blog too.

It is therefore worth laying out the conventions for these RFR vs RFR Cross Currency Swaps:

- Spot Starting.

- Initial and Final exchange of notional.

- USD SOFR vs foreign currency RFR (e.g. GBP SONIA, JPY TONA, CHF SARON, EUR €STR).

- Coupons are paid quarterly with overnight RFRs compounded daily.

- The spreads on either leg are excluded from the compounding calculations.

- All coupons have a two day payment lag. This means that all payments for non-USD RFRs match the payment dates on an equivalent USD SOFR swap. This avoids settlement risk when exchanging the coupon amounts in the two currencies. It also means that the final coupon payments will happen two business days after the “maturity date” of the cross currency swap.

- Whilst a two day payment lag is applied to the coupons, no other cashflows are delayed. This means that the Initial Exchange still takes place value spot, and the final exchange still occurs for value date of the maturity date. The final exchange of notional therefore takes place two business days before the final coupon payments take place.

- For trades that are resettable, the FX mark to market takes place every 3 months on the USD leg. The quarterly FX rates are taken T-2 before the coupon start dates and settle value T. Again, there is no delay for these FX Resets, meaning that there is a two business day gap between FX Resets and the coupon payments in each period.

For the avoidance of doubt, there are no shifts in observation periods for the RFRs in either currencies. We are simply seeing a payment delay and RFRs are always applied to their “natural” dates.

Similar conventions can be seen in the January 2020 ARRC publication, “Recommendations for Interdealer Cross-Currency Swap Market Conventions” but that document falls short of stating explicitly what the standards should be. Hopefully we are clearer above that this is exactly what is trading NOW in interdealer markets.

And finally, an @ISDA! Here are concrete examples of the current RFR Conventions in Cross Currency Swap markets 🙂

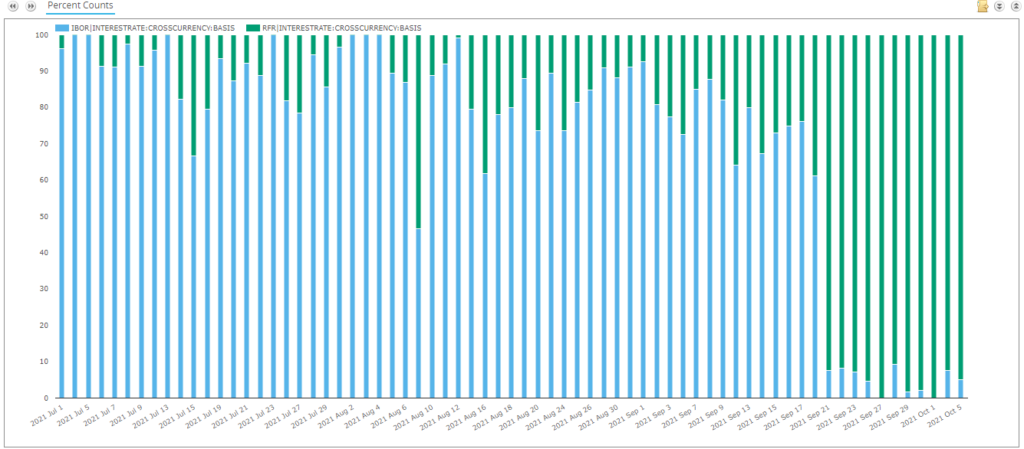

RFR vs RFR XCCY Volumes

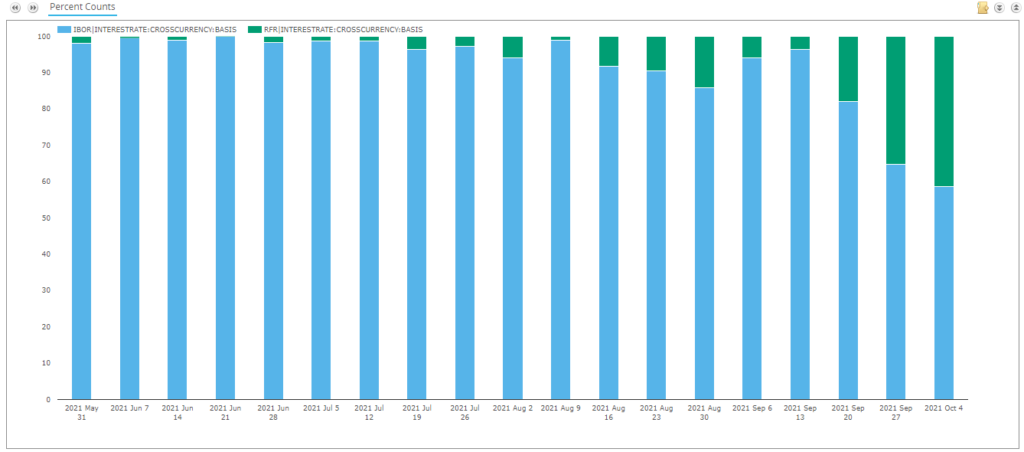

Making this relevant to what is going through the markets right now, we are seeing almost 100% of SDR reported volumes in GBPUSD, USDJPY and USDCHF transition to RFR vs RFR since the September 21st date. Our daily charts from SDRView Researcher summarise it nicely;

Showing;

- Proportion of trades (by trade count) traded LIBOR vs LIBOR (in blue) versus RFR vs RFR (in green) each day since July.

- This covers GBPUSD, USDJPY and USDCHF.

- 95% of trades since September 21st 2021 have been RFR vs RFR.

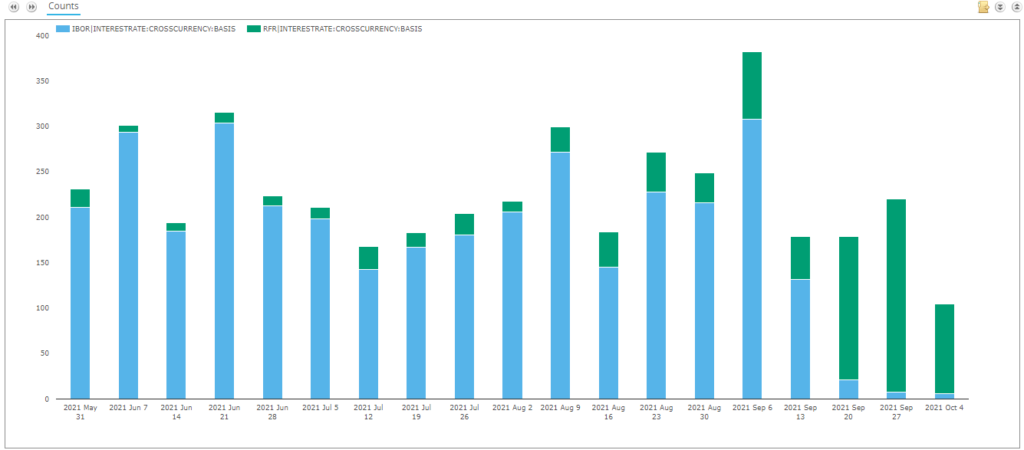

The weekly chart makes it clearer:

We are tracking slightly below the activity levels we enjoyed before September 21st (seeing ~200 trades per week at the moment) but that is well within the boundaries of variability for activity in cross currency swaps markets.

EURUSD markets are also being impacted by this transition. With 3 of the largest five currency pairs trading RFR vs RFR, it appears there is an increasing desire to trade €STR vs SOFR as well. Between 18% and 42% of trades are now RFR vs RFR in EURUSD:

Dealer to Client Markets

As we said stated in our original XCCY Swap blog:

Market Conventions

The Cross Currency Swap market has always been split in two – the Dealer-to-Dealer market versus the end-user Dealer-to-Client market. The “market standard” product that trades in the Dealer community is far removed from what an end-user client typically requires. However, it has evolved into the most efficient risk-transfer mechanism that we have for basis risk.

https://www.clarusft.com/mechanics-of-cross-currency-swaps/

The same still applies in an RFR world. Clients are very unlikely to want to trade with FX resets – they require their hedges to be fixed notional to precisely match cashflows. Equally, they may not want Floating-Floating exposures. Expect Fixed vs Fixed (which are of course NOT impacted by the move to RFRs) or Fixed vs Float to be far more common requests for clients. Finally, even if they are trading Float vs Float, there is nothing to say that both sides need to be an RFR. We have seen some SONIA vs USD LIBOR and SOFR vs EURIBOR reported to the SDRs for example. With EURIBOR continuing to be published, these structures are expected to keep on trading, but the data suggests they will mainly be in the client market.

In Summary

- 95% of GBPUSD, USDJPY and USDCHF cross currency swap markets are now trading RFR vs RFR.

- We define the precise market conventions in the D2D markets for these important hedging products.

- D2C markets will continue to see a variety of structures trading.

- The cross currency swaps market is seeing a very successful transition to RFRs so far.

Great blog Chris, as always. Could it be that your spec on the Xccy swap conventions is more detailed compared to ISDA, because you’ve done it from a practitioner’s point of view, whilst ISDA (perhaps) doesn’t have ex-practitioners working on these things and as a result, they sometimes don’t publish specs via the lens of practitioners…

When you say “All coupons have a two day payment lag. This means that all payments for non-USD RFRs match the payment dates on an equivalent USD SOFR swap.”, does this mean for a USD/JPY CCS, the business days for payment date will be NY+TKY and the payment date will be 2 NY+TKY business days after the end of each calculation period? So the lag could in theory be longer than 2 NY business days if the other currency has a holiday?

Correct. All standard interbank cross currency swaps already include a combination of the holiday centres in each currency for payment calendars (and London may also be added for CCS swaps with both legs in LIBOR) so this isn’t so different to current market practice.

Thanks Jan and it is a fair point. I guess there remains a gap in the market for specific market conventions aimed at market practitioners. One day we should do a Clarus Wiki for such things…

Very kind, thank you!