Overnight Indexed Swaps (OIS) are fixed-float swaps where the floating leg index is a compounded overnight interest rate. For short dated swaps, those less than 1Y, the coupon structure is usually zero coupon. For longer dated swaps, the fixed leg has a similar structure as the fixed leg on a regular LIBOR swap. Some of the details concerning key event dates (fixings and payments) on OIS swaps can cause confusion.

Reset Lag and Payment Lag

The OIS indices have a peculiarity concerning the fixing date (or publication date) of the underlying overnight rates, in that the fixing date can be later than the effective date of the rate. This is in contrast to a classic LIBOR fixing; for example, in our parlance, USD-LIBOR-BBA has a -2D fixing lag, whilst the USD-FEDERAL FUNDS-H.15 has a fixing lag of +1D. The need for a payment lag can be understood by considering an example in USD, suppose the calculation period end date is 2015-04-08, in which case, the last fed fund rate in the calculation period is for the period (2015-04-07, 2015-04-08) and its value is not published until the morning of 2015-04-08. There may not be enough time on 2015-04-08 to compute and agree the OIS compounded rate for the entire calculation period and so for practical reasons it is quite natural to require the payment on some day after the calculation period end date, hence a payment lag arises. A similar issue occurs with Fed Fund Swaps, however, in that case, the issue is handled not by using a payment lag, but by using a so-called reset cutoff (see Fed Fund Swap Nuances for more details). The table below highlights the conventions in several currencies.

| Ccy | ISDA/FpML Code | Fixing Lag (D) | Payment Lag (D) | BBG Ticker |

|---|---|---|---|---|

| AUD | AUD-AONIA-OIS-COMPOUND | +1 | +2 | ADSO* |

| CAD | CAD-CORRA-OIS-COMPOUND | +1 | +1 | CDSO* |

| CHF | CHF-TOIS-OIS-COMPOUND | -1 | +2 | SFSWT* |

| CHF | CHF-SARON-OIS-COMPOUND | 0 | +2 | |

| EUR | EUR-EONIA-OIS-COMPOUND | 0 | +1 | EUSWE* |

| GBP | GBP-WMBA-SONIA-COMPOUND | 0 | 0 | BPSWS* |

| JPY | JPY-TONA-OIS-COMPOUND | +1 | +2 | JYSO* |

| NZD | NZD-NZIONA-OIS-COMPOUND | 0 | +2 | NDSO* |

| PLN | PLN-POLONIA-OIS-COMPOUND | 0 | PZSO* | |

| USD | USD-FEDERAL FUNDS-H.15-OIS-COMPOUND | +1 | +2 | USSO* |

The payment lag is with respect to the calculation period end date, and consistent with the FpML field <../interestRateStream/paymentDates/paymentDaysOffset>. The payment lag for PLN has been tricky to confirm, so I have deliberately left it blank until I can get it verified (if anyone reading is certain of it, please let me know, and I will update the table).

Payment frequency = 1T ?

When looking at trade register files or trade repositories, it is not uncommon to notice a value of 1T in a column describing the payment frequency. One could be forgiven for thinking this is simply bad data, as values such as 3M, 6M, 1Y might seem more natural. However, 1T is a convention used in FpML, meaning there is a single payment at the maturity of the swap (T refers to ‘term’); it is typically used on zero coupon swap legs, in which case, one should not be too surprised to find payment frequency of 1T on the shorter dated OIS swaps.

Unadjusted Calculation Periods

Many examples discussing OIS swaps assume the calculation period start and end date are adjusted for good business days. Whilst this is commonly the case, occasionally one sees swaps with unadjusted calculation period dates. In this case, it is a little trickier to understand which underlying rates are to be used to compute the OIS compounded rate. The key step is to identify the first fixing and last fixing in the calculation period and adjust their weights to the number of days in the calculation period for which the overnight rate applies. So for example, considering a USD OIS Swap, if the calculation period end date is Saturday 4th April 2015, the last Fed Fund rate is for the period (2015-04-03, 2015-04-06), it is published on the morning of 2015-04-06, however its contribution is applied to the period (2015-04-03, 2015-04-04); that is, an accrual length of 1/360 rather than the usual 3/360. A similar `stub-like’ calculation is applied at the calculation period start date.

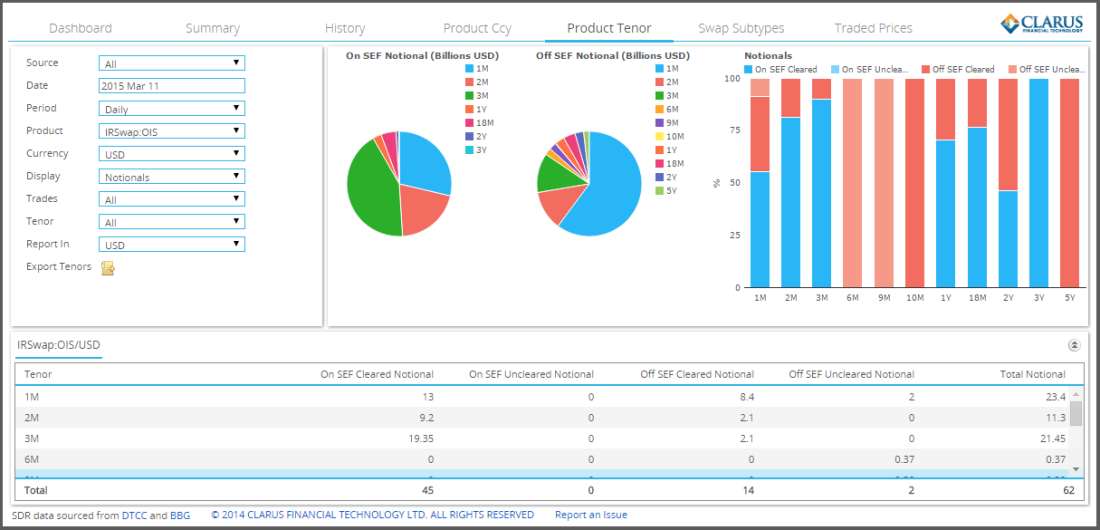

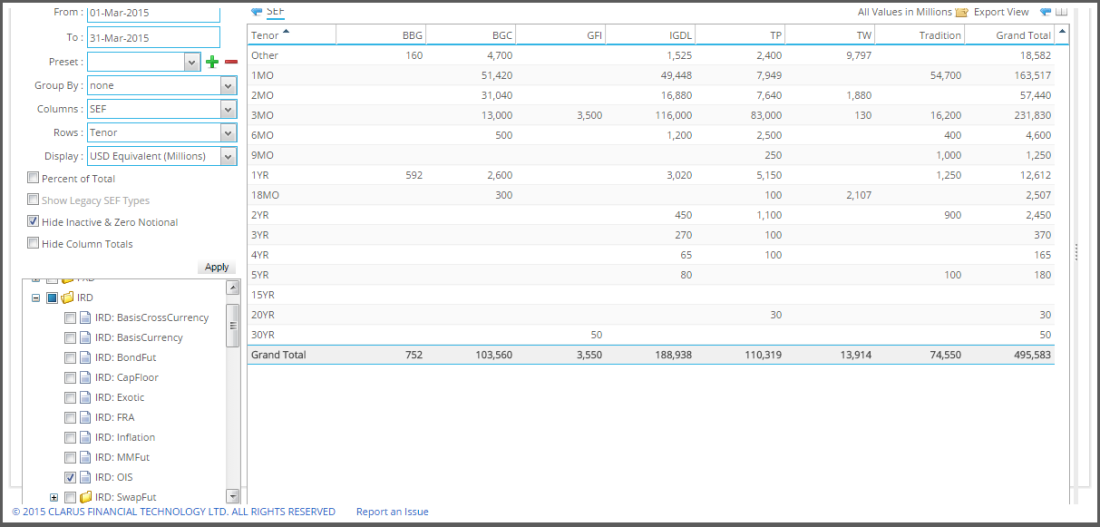

Volumes

OIS swaps tend to be relatively short dated; in USD many are traded off SEF, and one can see in SDRView that the volumes are much smaller than regular LIBOR fixed float swaps.

The on-SEF volumes can be further broken out by SEF in SEFView.

Updated 13th July 2016: Added payment lag of 2D for AUD.

Updated 6th July 2017: Added NZD-NZIONA-OIS-COMPOUND.

Updated 26th October 2017: Added CHF-SARON-OIS-COMPOUND.

Updated 27th May 2020: Corrected payment lag on NZIONA to 2D, as stated in the document, ‘Interest Rate Swap Convention’, Nov 2019, NZFMA.

Updated 10th May 2022: Corrected fixing lag to +1D, consistent with ‘Cash Rate Methodology‘, 26th October 2021, RBA.