Cross-currency swap markets are in the process of adapting to a post-Libor environment. New trades will reference the RFRs or risk a complicated process of renegotiating fallbacks (in the case of legacy trades) or incorporating the proposed ISDA fallbacks, when the 2006 ISDA Definitions change. Either way, continuing to reference Libor past 2021 will become problematic.

In this blog I will look at the latest developments, some technical issues of RFR-based cross-currency swaps and also how the AUD market is adapting to the RFRs.

Further regulatory developments

On 21st February 2019 Megan Butler, Executive Director of Supervision, Wholesale and Specialists at the FCA, delivered a speech at the Investment Association, London.

For those who missed the live speech, you can read it at this link.

Again, the message is clear and continues the theme from last month (Schooling Latter in my last blog): continuing to rely on Libor past 2021will create considerable problems. Ms. Butler was referring more to the cash markets (issuance and investing) but this will have significant repercussions in the derivatives markets.

In January and February, the US ARRC has also been active in promoting the expansion of RFRs for bilateral business loans and securitizations. The link to the announcement can be found here.

We are seeing both the UK and US markets actively promoting the use of RFRs for cash products and defining the standards that can be used to create viable markets for these products. And derivatives (IRS and cross currency) will have to adapt to provide the hedges.

Changes required in the cross-currency swap markets

Cross currency swaps are often used by cash market participants to ‘onshore’ their debt or investment portfolios. As the use of RFRs spreads in the cash markets, the cross-currency markets will have to adjust as well. A few of the considerations are:

Do you align payment dates or calculation dates?

In current market conventions, this is perfectly aligned: the payment of the interest occurs on the final day of the calculation period, e.g. every three months. In the RFR case, the payment date is offset by several days because the final rate is not known until the final day of the calculation.

This offset varies across the currencies: a great reference is OIS Swap Nuances.

It is often not possible to have the rate fixing days and the payment days the same for both legs of the swap. This can lead to complications unless closely managed.

How do you manage interest and notional payment dates?

The RFR payment offset feature is likewise problematic for the notional and interest payment dates. If you align the interest and notional payment dates, then the rate fixing dates and day counts (per period) may not be the same. But if you align the rate fixing and notional dates the payments can be different. Either option has merits and challenges.

How does a fixed/floating cross currency swap work?

The fixed side of a cross currency swap is decided by the cash product it is hedging – so far, no change. But the floating side will still have the payment/calculation period issues from points 1 and 2 above.

The markets will have to address these (and other) issues in the very near future to make the cross-currency swap markets support the cash markets and assist in increasing liquidity in RFR-based issuance and loans.

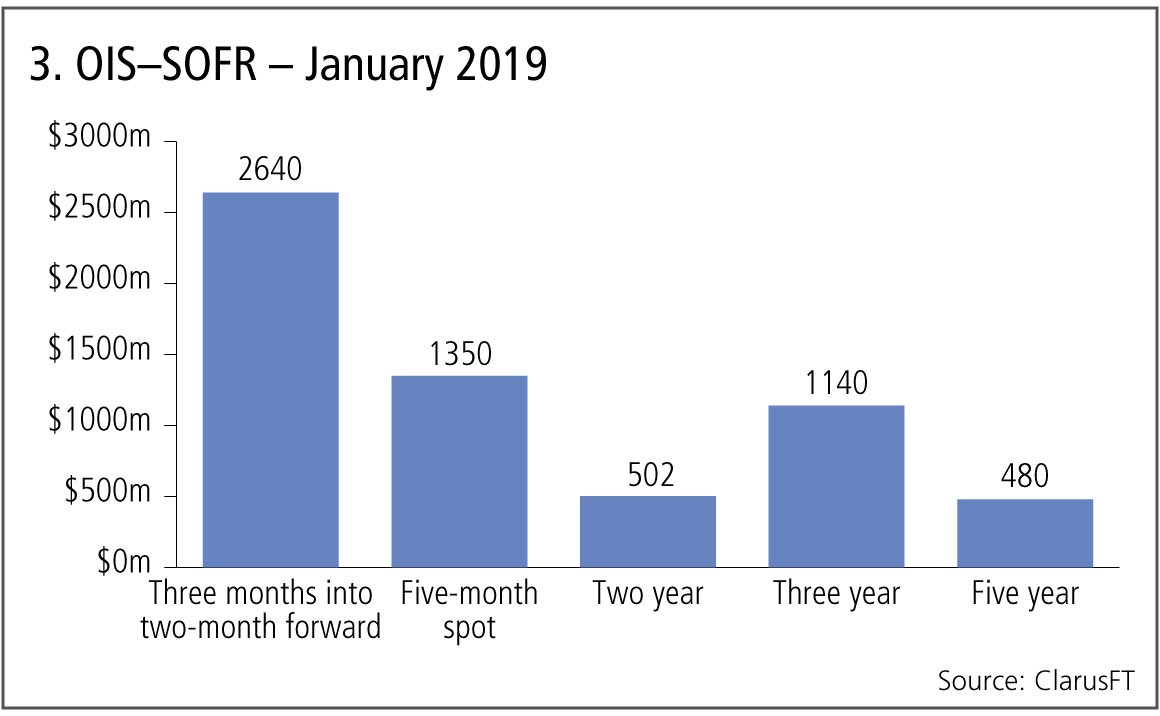

RFR developments

I commented in my February 2018 blog that the SONIA and SOFR markets would need to see an increase in liquidity in longer tenors for real increases in their use.

Amir Khwaja’s post earlier this month (and the associated Risk article) shows these markets are increasing in volume for longer tenors. I have added the chart for SOFR from Amir’s blog below.

This is a significant development that I will be watching closely over the next months.

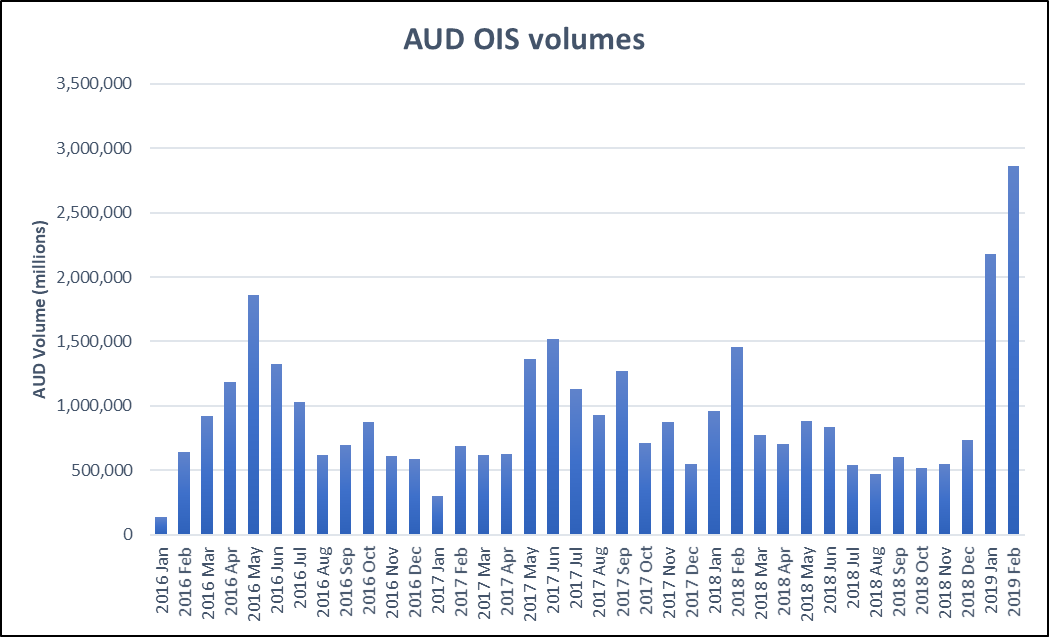

The Australian market

My ‘home market’ has seen a few interesting developments over the past months in line with those in the UK and US markets. Interest in RFR product is increasing and the first bond issue is close at hand.

In November 2018 SAFA (South Australia Government Financing Authority) announced the intention to issue a bond linked to the Australian RFR, AONIA. This issue is scheduled for 2019 and will be a first for AUD.

Also, the OIS market has seen some significant increase in turnover in the last few months. I looked at the cleared monthly volume in Clarus CCPView over the past 3 years of data.

The chart shows a significant increase over the past two months. The AUD market is increasing volumes (perhaps due to potential changes in cash rates) but it is still relatively short-dated. It does seem to be following the UK and US markets in growing the RFR markets and product range.

Where from here?

As we have been observing, the RFR markets are changing. The message from regulators is that a timely move from Libor to RFRs is highly encouraged which is leading to growth in cash and derivative market volumes.

Cash products (loans, bonds etc.) are growing in volumes linked to RFRs and are supported by a greater focus on standardized terms and conditions.

The cross-currency swap markets will need further development to support the cash markets. But this is also starting to show positive signs.

Markets outside UK and US are following the lead of SONIA and SOFR: the AUD market is in the initial stages of issuing an RFR-based bond.

I am confident that markets and products based on RFRs will continue to grow in 2019.

So, be prepared!