SA CCR for Excel

Access the power of cloud-hosted SA-CCR analytics directly from spreadsheets

For financial firms using SA CCR, we offer a free trial

CLARUS Excel Workbook or Add-in

Standardized Approach to Counterparty Credit risk

What-if analysis

Easy to Trial, Purchase and Start Using

Learn about SA CCR

Latest Posts

-

Jan, 14

What’s new in CCP disclosures – Q3 2025?

Clearing houses published in December their latest CPMI-IOSCO Quantitative Disclosures for Q3 2025. Key takeaways On 30 September 2025: Background Under the CPMI-IOSCO Public Quantitative Disclosures, central counterparties (CCPs) publish over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing, and more. CCPView has more than 8 years of these […]

Read moreSep, 24

What’s new in CCP Disclosures – Q2 2025?

Clearing houses have published their latest CPMI-IOSCO Quantitative Disclosures for Q2 2025. Key takeaways Background Under the CPMI-IOSCO Public Quantitative Disclosures, central counterparties (CCPs) publish over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing, and more. CCPView has more than 8 years of these quarterly disclosures for 44 clearinghouses, each with multiple Clearing […]

Read more -

Dec, 3

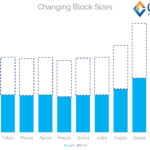

New: Kids on the Block (Sizes)

The new block sizes in SDR data make trends in the data more difficult to identify – because now only 25% of notional should be “dark” (i.e. above the capped thresholds), down from 50%. More transparency is good, but we need to be careful when looking at data from before and after the new block […]

Read moreNov, 13

We Have New Block Sizes

Block Calibration It has been a long journey to finally arrive at the “go-live” for new block thresholds on October 4th 2024. I covered it here on the blog, so rather than re-hash what has happened, please refer to the old posts linked below: Suffice to say that there have been more than a few […]

Read more -

Oct, 8

Pre-Hedging in Swaps

FMSB The FICC Markets Standard Board (see my 200th Clarus blog), known as the FMSB, recently published the paper “Spotlight Review on Pre-Hedging“. It makes great reading for anyone involved in Swaps markets – dealers, sales, trading, buyside. Read it! What is “Pre-Hedging”? According to the FMSB report, pre-hedging is the act of a dealer […]

Read moreAug, 20

Monitoring of Hedge Funds

Hedge funds are frequently in the financial news, which is not at all surprising given the size of the sector and the public profile and wealth of the founders. So it is good to see that a Hedge Fund Monitor has been released by the Office of Financial Research of the U.S. Department of the […]

Read more -

May, 14

Using AI for Market Abuse Surveillance

The EU Market Abuse Regulation (MAR) requires institutions to monitor transactions and develop specific algorithms to check for possible abuse covering insider dealing, market manipulation and other categories. One of the challenges is that calibrated monitoring thresholds tend to be conservative and consquently produce a high number of false positives. These must then be manually […]

Read moreApr, 29

Regulating the transformative power of AI in Asset management

Artificial Intelligence (AI) is a transformative technology and this article covers a number of key regulatory areas for asset management including the recent EU AI Act, bias, transparency and security. Please read on the ION Markets Blog.

Read more -

Jul, 26

FSB Paper on Liquidity in Core Government Bond Markets

I recently took a first look at Central Clearing of Bonds and Repos and in that blog I mentioned a Financial Statility Board (FSB) paper on Liquidity in Core Government Bond Markets. This paper analyses the liquidity, structure and resilience of government bond markets, with a focus on the events of March 2020; characterised as […]

Read more