- October 4th saw new block sizes implemented in the US.

- The new block thresholds are now 64% larger in USD Swaps.

- This will result in better post-trade transparency in derivatives markets.

Block Calibration

It has been a long journey to finally arrive at the “go-live” for new block thresholds on October 4th 2024. I covered it here on the blog, so rather than re-hash what has happened, please refer to the old posts linked below:

- 12th May 2020: CFTC Block Trading Consultation May 2020.

- 30th Sep 2020: New Block Trading Rules for Derivatives.

- 19th July 2023: New Block Trading Rules Will Now Start in December 2023.

- 06th Dec 2023: Dec 4th has been and gone. Where are our new block sizes please?

Suffice to say that there have been more than a few twists and turns, but we are there now!

New Block Sizes

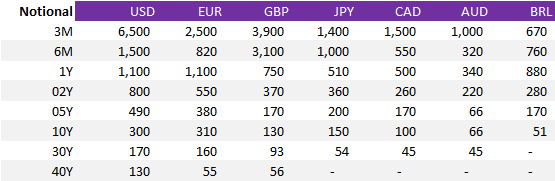

For ease of reference, the new block sizes, in USD millions of trade notional, are:

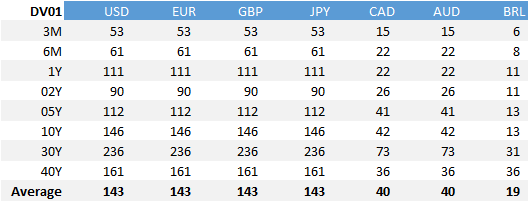

Which equates into DV01 ($000s equivalents):

Showing;

- For a USD swap to be treated as a block trade (and therefore qualify to be executed off-SEF and RFQ-to less than three), it will have a DV01 between $111,000 and $334,000 (ignoring the 6 month point that seems to have a strange calibration).

- On average, a USD swap will need to be over $233k in DV01 to qualify as a block trade.

- This is about 25% larger than for EUR swaps, which will “only” need to trade in $185k DV01 or above to qualify for block treatment.

- We then step down to GBP swaps, where blocks are less than half the size ($109k DV01), compared to USD.

Previous Block Sizes

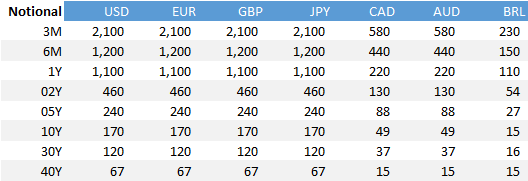

Not all of us can remember the precise Block and Capped thresholds! So here is a quick summary of the previous thresholds, in USD millions of trade notional:

Which equates into DV01 ($000s equivalents):

Showing;

- Block sizes have always varied by currency and tenor.

- The old thresholds were calibrated on very old data, and as can be seen above, weren’t exactly linear in their DV01 thresholds either.

- There were three groups of currencies, where-as the new thresholds are currency specific.

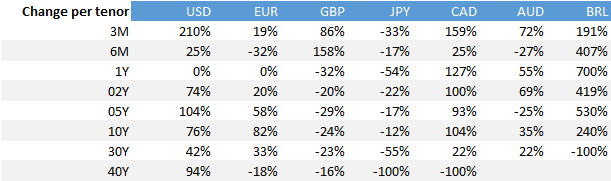

Changes

Overall,

- USD block sizes are now 64% larger in DV01 terms.

- EUR are 29% larger.

- GBP are 23% smaller.

- JPY are 47% smaller.

These changes reflect the better quality data that is now being used for calibration. They take into account the liquidity differences between markets, as well as the fact that markets have changed in the past 12 years (for example JPY).

The changes per tenor per currency are highly varied. Remember this is the first time that these thresholds have been calibrated using actual post-trade transparency data. So we really shouldn’t put too much weight on the original thresholds, other than they were familiar (and didn’t appear to cause markets any harm). I include the list of changes more for completeness than for any particular desire to analyse them:

Data Impacts

The SDR data has changed as a result of these new thresholds. Let’s see if three hypotheses hold true as a result of the new thresholds.

- We will see fewer block trades/trades above the capped threshold as a result of the recalibration:

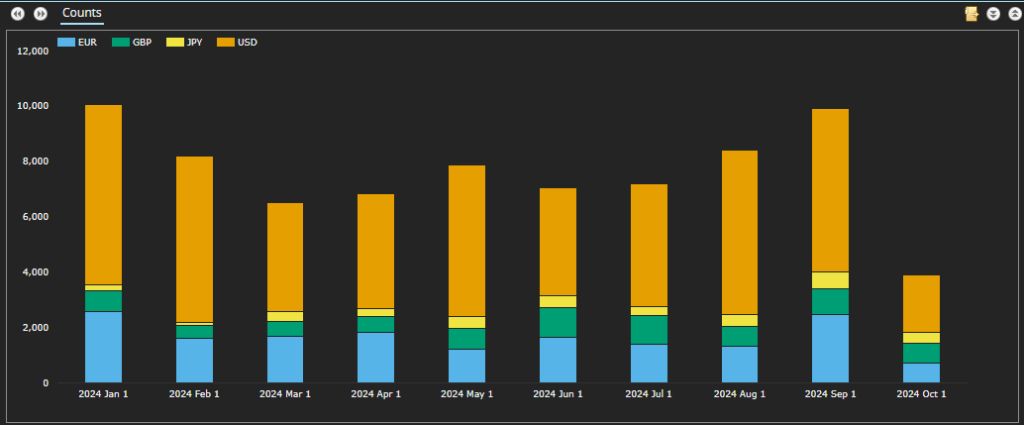

That is certainly true! October saw 3,910 capped trades reported in the four major currencies, down 50% from the monthly average in 2024.

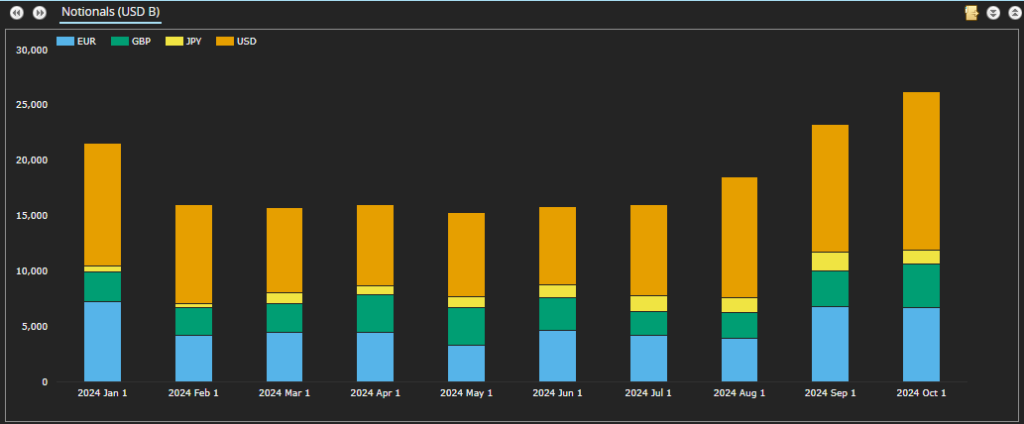

2. Notional amounts will now be higher in SDRs:

This is probably true. As we know, trading activity varies a LOT from month to month. October 2024 volumes were 50% higher than the 2024 monthly average.

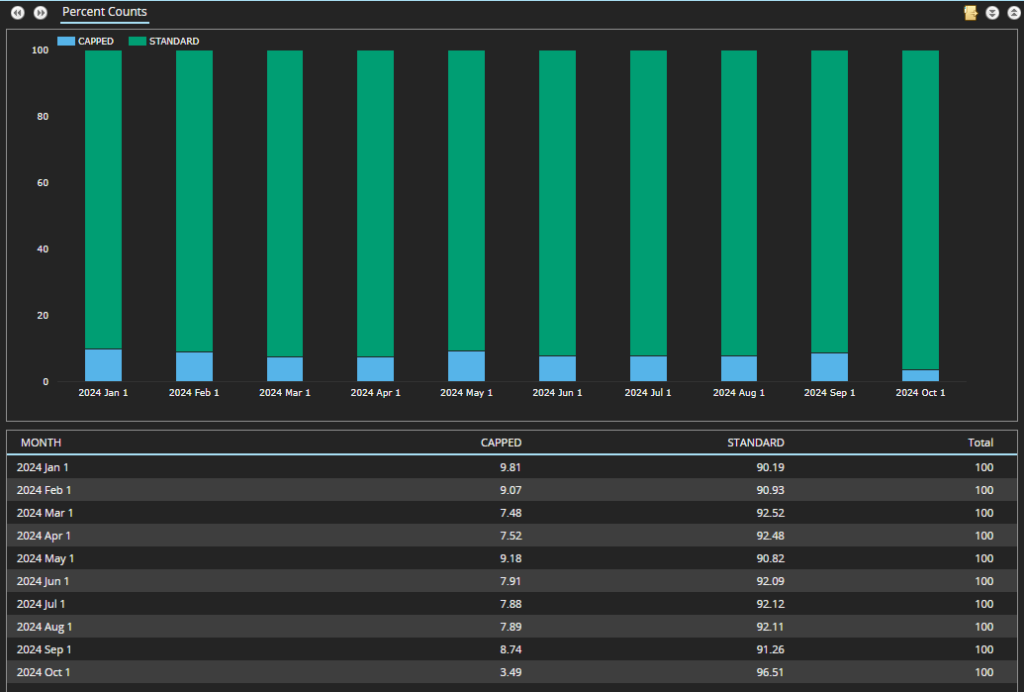

3. The proportion of capped trades being reported should be about 25%:

Wrong! Okay, I put this one in there intentionally. The calibration is not meant to apply to 25% of trades, it means that 25% of total notional remains “dark”. The distribution of notional trading activity is highly skewed toward a handful of truly huge trades, with lots of small tickets trading frequently. This means that less than 4% of trades by trade count now qualify for capped reporting. That is down from 8% as a result of the new calibration.

For Clarus Subscribers

These changes impact SDR data, and therefore only impact the data that our subscribers see in SDRView products. The data in CCPView and SEFView remain completely unchanged. The data in CCPView and SEFView are at a higher level (typically instrument-level), therefore there are no trade-level block thresholds to apply.

In Summary

- Transparency has improved in our markets.

- Higher block thresholds mean that less risk remains “dark”.

- The benefits are already there in the data, with 50% less trades above capped thresholds.

- As ex-CFTC Chairman Heath Tarbert said back in 2020 “data is the lifeblood of our markets…sunlight is the best disinfectant.”