- Cross Currency swap trading has transition quickly to USD SOFR and away from USD LIBOR in 2022.

- All of the currency pairs we look at show evidence of a transition to USD SOFR.

- Some markets are now trading RFR vs RFR Cross Currency Swaps.

- Most of the other markets now trade Term domestic rates vs USD SOFR.

- The transition does not appear to have negatively impacted overall volumes.

- 12 charts summarise transition efforts across 14 currency pairs in Cross Currency Swaps.

After the success of the first round of the “RFR First” initiative in Cross Currency Swaps, how is the uptake of SOFR on Cross Currency USD legs progressing in 2022?

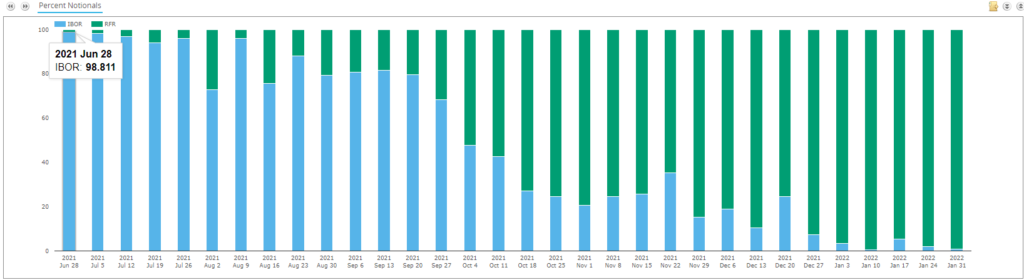

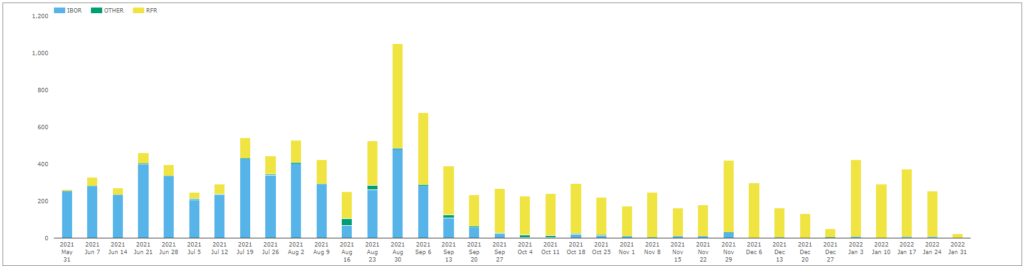

The Big One – EURUSD

Showing;

- Virtually all trading reported to US SDRs in EURUSD is now SOFR vs €STR (the green bars).

- That leaves nowhere to hide for those wanting/needing to still trade USD LIBOR in the biggest cross currency swaps market of all.

- Remember EURIBOR will still be around for a while yet, but the Cross Currency swap market (at least) won’t need to worry too much about any regulatory changes to EURIBOR’s status (at least for new trades!).

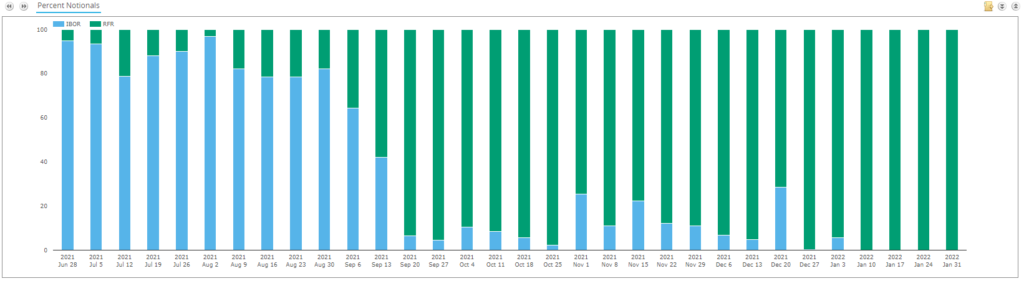

For GBP, JPY and CHF vs USD, a single chart will suffice as it looks very similar to the EURUSD one above.

The Interesting Ones

I feel like most people following this blog would have expected those two charts. So let’s move onto the stuff we don’t know too much about. What is happening in other currency pairs?

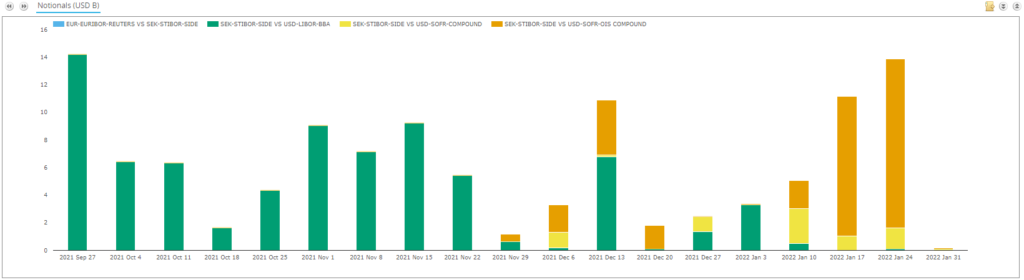

SEKUSD

In SEKUSD;

- Term STIBOR vs USD SOFR is now the preferred structure in cross currency swap markets.

- Both the orange bars and yellow bars represent STIBOR vs USD SOFR in the above chart. USD SOFR happens to be reported with a couple of different index names when reported to SDRs, but they are the same index.

- Virtually 100% of trades in 2022 have been STIBOR vs SOFR, marking another success in the transition away from USD LIBOR.

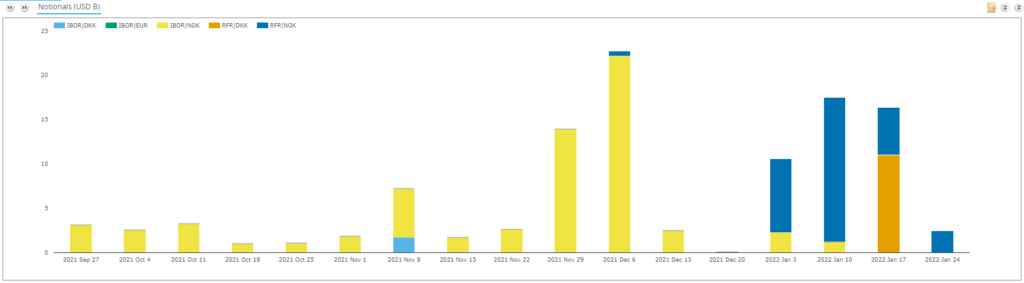

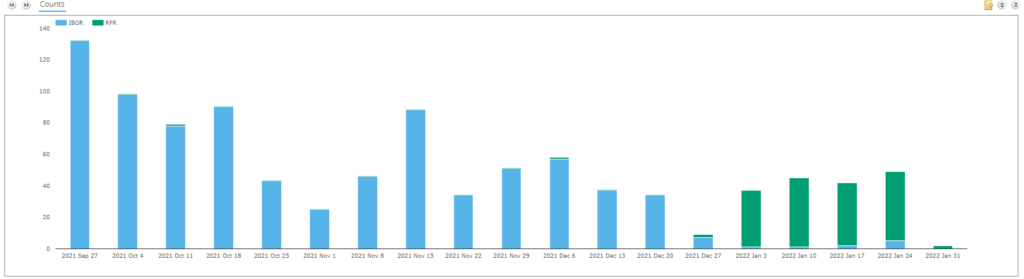

NOKUSD and DKKUSD

There are far fewer trades reported to US SDRs in NOKUSD and DKKUSD than SEKUSD, so I’ve grouped them together for now. It is fair to say:

- NOK vs USD has seen 80-100% of trades as NIBOR vs SOFR in 2022.

- Of the handful of trades in DKK vs USD (12 trades this year), 10 were in CIBOR vs SOFR.

A potential lack of European coverage and sparse activity in these two currencies combine to mean we cannot declare success in the transition away from USD LIBOR yet, but the signs are very encouraging.

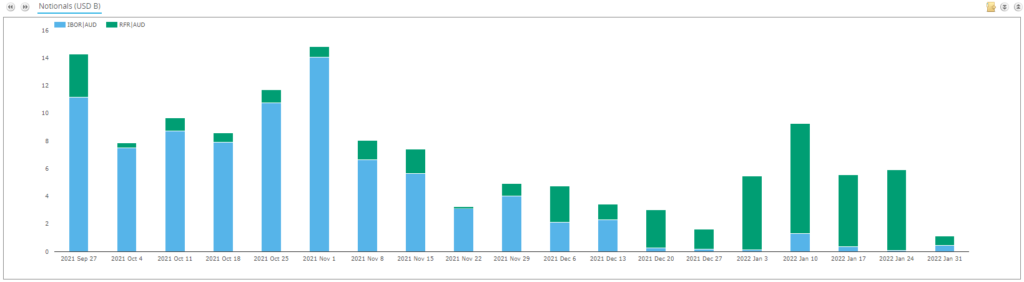

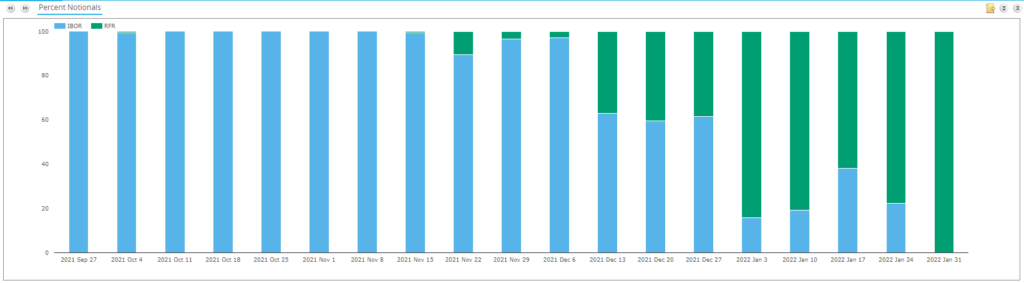

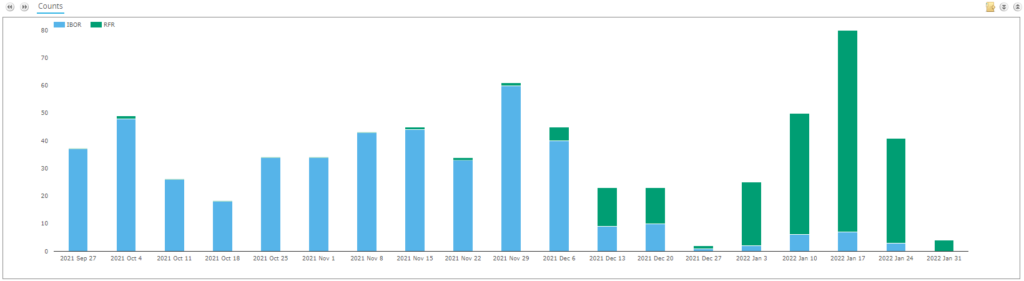

AUDUSD (& NZDUSD)

AUD has seen a huge shift, which started well before the end of the year:

- AUD BBSW (term) vs USD SOFR is the market standard now.

- (Yesterday saw only two trades, so take the final bar in our weekly timeseries with a pinch of salt please).

- Over 90% of trading in 2022 in AUD vs USD has involved a USD SOFR leg – great news for transition.

- AUDUSD has generated very similar amounts of “RFR” risk this year as have SEKUSD and NOKUSD – around $30bn YTD trading in each of the three currency pairs.

Importantly, I don’t see any market decrease in overall volumes for January 2022 compared to e.g. November 2021. The transition to USD SOFR legs has not negatively impacted activity.

For completeness, NZDUSD has also transitioned to trading NZD BBR FRA (Term) vs USD SOFR.

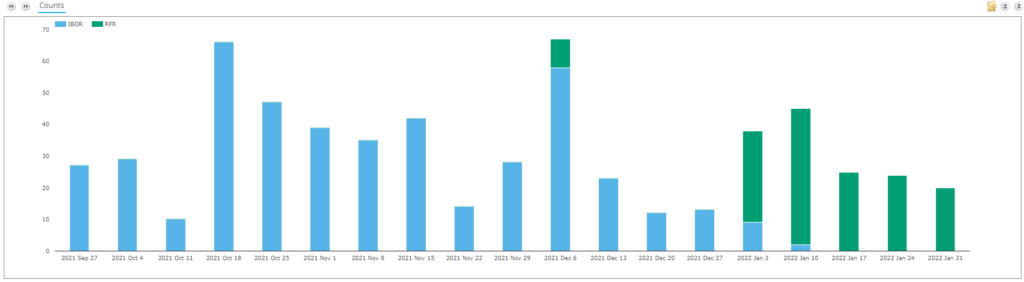

CADUSD

CAD is showing a slower transition than some of its peers:

- All RFR trading has been in CAD CDOR (term) vs USD SOFR in 2022. I don’t see any CORRA vs SOFR trades reported (yet?).

- Some weeks have seen as little as 64% of risk traded vs SOFR. The rest has been vs USD LIBOR.

- However, this looks to be skewed by some large notional LIBOR trades. On a trade count basis, CADUSD looks to be in a much healthier position to transition completely away from USD LIBOR:

We’ve seen fewer than 20 trades all year in CADUSD with a USD LIBOR leg. That is certainly a good sign.

MXNUSD

MXN is an interesting one. USD SOFR is finally being adopted. Nothing like leaving it to the last minute!

- MXN TIIE (term) vs USD SOFR is now the market standard.

- Amazingly, we’ve not seen a MXNUSD trade with a USD LIBOR leg reported since the 12th January.

- This is a great example how quickly these markets can transition.

- I’ve intentionally switched to trade counts in the chart above as the notionals are pretty small each week (~$2bn total).

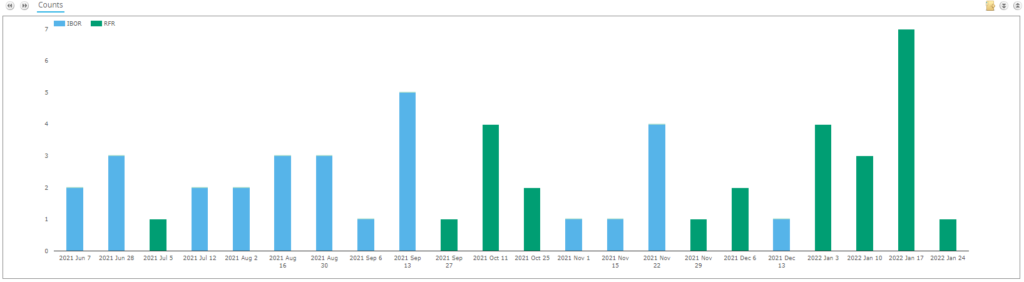

TRYUSD

TRYUSD trades as fixed TRY versus floating USD. It hence attracts both TRY Rates positions (which are volatile!) as well as the more vanilla use case for funding trades in TRY vs USD. And interestingly….

- The market standard is now Fixed TRY vs USD SOFR!

- There have been less than 10 trades in TRY vs USD LIBOR in 2022.

- It is difficult to know whether the market is struggling to digest this move or not. Volumes are volatile in this market so we need more data.

- What is incredible is that we saw no sign of this shift happening, even in the middle of December. It has been a “flick of a switch” type move.

- This really shows how broad reaching the transition away from USD LIBOR is. And how effective direct regulatory action, in terms of stopping new USD LIBOR activity, can be.

Of course, it is easy to criticise the data – this is US Persons activity reported to US SDRs – but we continue to believe this is representative of the overall market.

SGDUSD and HKDUSD

We’ve been guilty, since our last post in September 2020, of somewhat neglecting SGD markets (I blame Mark for relocating!). Despite covering the nitty-gritty of the actual rates involved as early as 2019, and raising the problems with SGD benchmarks in our responses to the ISDA Fallback consultation process, we forgot to write about the actual transition that then happened.

Happy to say, SGD markets have largely transitioned away from SOR (that had a USD LIBOR component) and into the anointed RFR, SORA:

Showing that SGD Rates markets, across IRS and OIS, have now transitioned completely to a SORA RFR product. What does this mean for SGD vs USD Cross Currency Swaps?

- The market standard is now SORA (RFR) vs USD SOFR (RFR), marking out SGDUSD as one of the few markets that has also transitioned to RFR vs RFR trading.

- However, please note that this is a very small sample. SGDUSD really doesn’t trade much, as reported by US SDRs. Less than 8 trades per week….

- Still, even smaller markets can successfully transition to RFR vs RFR trading.

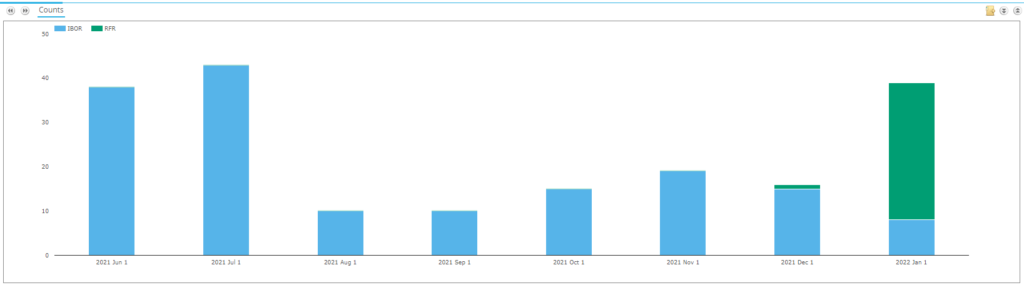

And HKDUSD cross currency?

- The market standard is now HKD HIBOR (term) vs USD SOFR in HKDUSD.

- Apologies for switching to monthly volumes, but I’m getting bored of the same old charts at this stage of the blog!

- I think the chart shows nicely that this transition really was non-existent in December.

- In 2022, 80% of HKDUSD trades have now been versus USD SOFR.

In Summary

- EURUSD, GBPUSD, CHFUSD, JPYUSD and SGDUSD now trade as RFR vs RFR Cross Currency Swaps.

- AUDUSD, NZDUSD, CADUSD, SEKUSD, NOKUSD, DKKUSD, HKDUSD and MXNUSD now trade as Domestic Term vs USD RFR for Cross Currency Swaps.

- TRYUSD now trades as Fixed TRY vs USD SOFR.

- The data suggests that the transition to USD SOFR in Cross Currency markets has gone well.