- ISDA has launched a second consultation on LIBOR fallbacks.

- This extends the number of benchmarks covered to eight currencies.

- The big one this time is USD LIBOR, which is interesting because USD SOFR has a limited history available.

- Fortunately, the New York Fed has made a proxy USD repo rate available back to 1998.

- 78% of market participants would prefer there to be consistency across fallbacks for all benchmark rates.

More than Six!

I was surprised to read the Bloomberg article below:

For the world’s biggest financial firms, getting ready for the end of one multi trillion-dollar global reference rate is a monumental undertaking. Getting ready for the end of half-a-dozen? Some would call that impossible https://t.co/dkQ6amAraw

— Bloomberg Markets (@markets) June 3, 2019

By my count, we are facing the end of EIGHT benchmarks so far, plus the pending consultation on Euribor, making NINE in total.

Did Bloomberg just choose to highlight 6 of them because #sixtimes is trending today? (Apologies, I couldn’t resist, seeing as I just got back from Madrid….).

The complete list of indices is:

- GBP LIBOR

- CHF LIBOR

- JPY – LIBOR, TIBOR and Euroyen TIBOR

- AUD BBSW

- USD LIBOR

- CAD CDOR

- HKD HIBOR

- SGD SOR

As a reminder, the original ISDA consultation settled on the Compounded Setting in Arrears Rate with Historical Mean/Median Approach. Check out our blog for exact details.

ISDA Consultation 2

The new ISDA consultation can be found here, snappily titled “Supplemental Consultation on Spread and Term Adjustments for Fallbacks in Derivatives Referencing USD LIBOR, CDOR and HIBOR and Certain Aspects of Fallbacks for Derivatives Referencing SOR“.

You can read about our coverage of the original consultation in my blog on “LIBOR Fallbacks” and read about the results of the previous consultation in our coverage “ISDA Announce LIBOR Fallback Methodology“.

I guess all anyone wants to know with this second consultation is whether the outcome will be any different, with the majority of respondents last time choosing the Compounded in Arrears with Historical Average approach.

Let’s take a look at the details of this consultation as well as some useful background.

Background 1: Current Fallbacks

First, a bit of background that covers a question we are asked here quite often. What happens today if a rate disappears?

On Page 5 of the Consultation, ISDA explains the process. It’s not great for anyone!

- The calculation agent for the trade must obtain quotes from major dealers for what the ‘IBOR would be if it were to be published.

- If an ‘IBOR is permanently discontinued, then it is likely to be for good reason. Therefore, it is very unlikely that the calculation agent will be successful in securing these quotes.

- Even if they can get quotes, this is only likely to be a short-term solution for the calculation agent, and not really a suitable approach for contracts with another 30+ years to run….

- Equally, these quotes may vary significantly across the market. That could be awkward for the calculation agent – what averaging methodology should be used if you only have 2 or 3 quotes etc.

Most notable:

None of the current fallbacks described above were designed to cover permanent discontinuations.

ISDA Consultation

Background 2: RFRs

The second bit of background worth clarifying are the Risk Free Rates for each currency. These aren’t up for discussion in the consultation – these are already appointed by the national RFR Working Groups:

- USD = SOFR

- CAD = CORRA

- HKD = HONIA

- SGD = Adjusted SOR, implied from USD/SGD FX swaps and the fallbacks for USD LIBOR .

We’ll save coverage of the exact SOR methodology for a future blog, and try to cover Thailand and the Philippines at the same time. These domestic rates are implied from FX swaps, using USD Libor as an input.

It is worth noting that both CORRA and HONIA are under-going changes – I guess to make them both more robust. Maybe we’ll also find time to cover these changes in later blogs too…it’s going to be a busy June!

USD LIBOR

Evidently, USD LIBOR is the big one here. This was touched on in the previous consultation, and ISDA highlight here that:

78 percent found it appropriate to use the same methodology across all benchmarks.

ISDA Consultation

And pleasingly went on to note a point very close to my heart:

Respondents indicated that using a consistent approach across different IBORs would allow market participants to better manage risk exposure (e.g., by mitigating basis risk in cross-currency swaps).

ISDA Consultation (with our own emphasis)

We ask all respondents to the latest consultation to carefully consider this last point and to please ask your cross currency swaps desk for their input!

Responding to the Consultation

1. The Easy Way for most Respondents

There is an easy option here, which I think Clarus are very likely to follow. If you previously responded to the July 2018 Consultation (we did) and you do not consider anything is different now, you can re-affirm that your responses should also apply to these other benchmarks:

Seeing as 78% of respondents would like to see consistency across benchmarks, I think this is going to be a common course of action.

2. The Slightly Harder Part

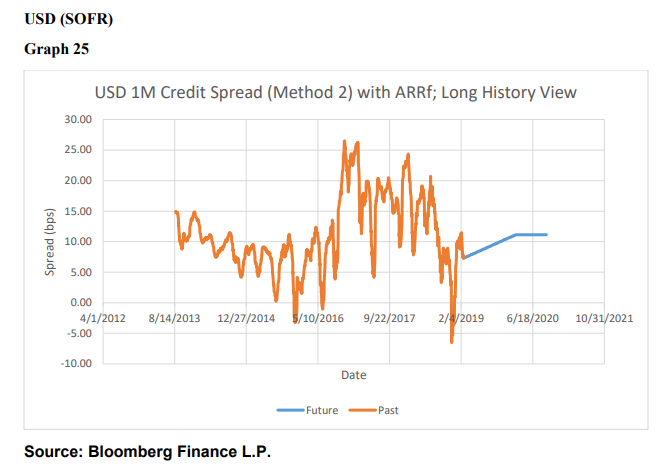

If you are responding for the first time, or feel like things have changed, then please check out our first blog for the options being proposed and respond accordingly. It is also worth noting that we have already had a go at calibrating the GBP LIBOR spread and the AUD BBSW spread. ISDA also provide a chart for 1m USD LIBOR versus SOFR to give you some idea of the spreads:

http://assets.isda.org/media/442dc439/9e9dd034-pdf/

3. The Part We All Need to Think About

The consultation contains two important new questions. Namely;

SOFR history only goes back to 2014. Should we use the “Overnight Treasury GC Repo Primary Dealer Survey Rate” as a proxy to extend the history back to 1998?

I am amazed that ISDA did not include a link to the New York Fed website to explain what this other repo rate actually is. HERE IS THE LINK!

https://www.newyorkfed.org/markets/opolicy/operating_policy_180309

The NY Fed highlight that it is unlikely that we will get a longer history of SOFR than is already available (it goes all the way back to August 2014 now), and this “proxy” rate differs because:

- It’s a Mean not a Median.

- This survey rate excludes non-primary dealers.

- This survey rate only includes General Collateral.

It is difficult to answer this question without knowing what the look-back period will be for the averaging. 5 years? 10 years? Even if it is 10 years, that will exclude 2008. Does that mean a proxy is probably okay for the first four years of the time history? It will be interesting to see the responses here.

The second new question is:

Should SGD-SOR use the USD LIBOR fallbacks as the input to its’ calculation (along with FX swaps)?

We plan to review the FX-related SGD-SOR methodology in a future blog (probably next week), so keep your eyes on the Clarus website for some pointers on this.

In Summary

- The big one for this latest ISDA consultation is USD LIBOR.

- The deadline for responses is July 12th 2019.

- We show you where to get the information for an extended history of a SOFR-like rate from the New York Fed.

- 78% of respondents to the original ISDA fallback consultation showed a preference for consistency of fallback methodologies across all currencies.

- SGD-SOR is also covered in the consultation, which uses a derived rate from FX swaps. We will cover the methodology in a future blog.