- A new Fallback Rate (SOR) will be used on SOR-referencing contracts in the event of a cessation of USD LIBOR.

- This rate should not be used in any new derivatives, and is only expected to be published for a period of about three years.

- As Clarus highlighted during the original ISDA consultation, the Fallback Rate (SOR) mixes forward-looking FX contracts with backward-looking SOFR fixings to create a synthetic SGD rate.

- This combination of backward- and forward-looking aspects is potentially concerning and highlights that fallback rates should only be viewed as a safety net for counterparties unable to trade out of SOR-referencing contracts.

Transparency

The benchmark administrator in Singapore, ABS, has done a great job making available a whole raft of resources relating to SGD benchmarks.

If you’ve not seen the latest resources from them, please check them out:

Thanks to their transparency, it really only takes about 10 minutes of your time to get a great overview of benchmark reform and transition to RFRs in the SGD market. I’ll try to summarise as best I can below, which can be read in conjunction with our original 2019 blog on the Mechanics and Definitions of SGD Benchmark Rates.

SORA

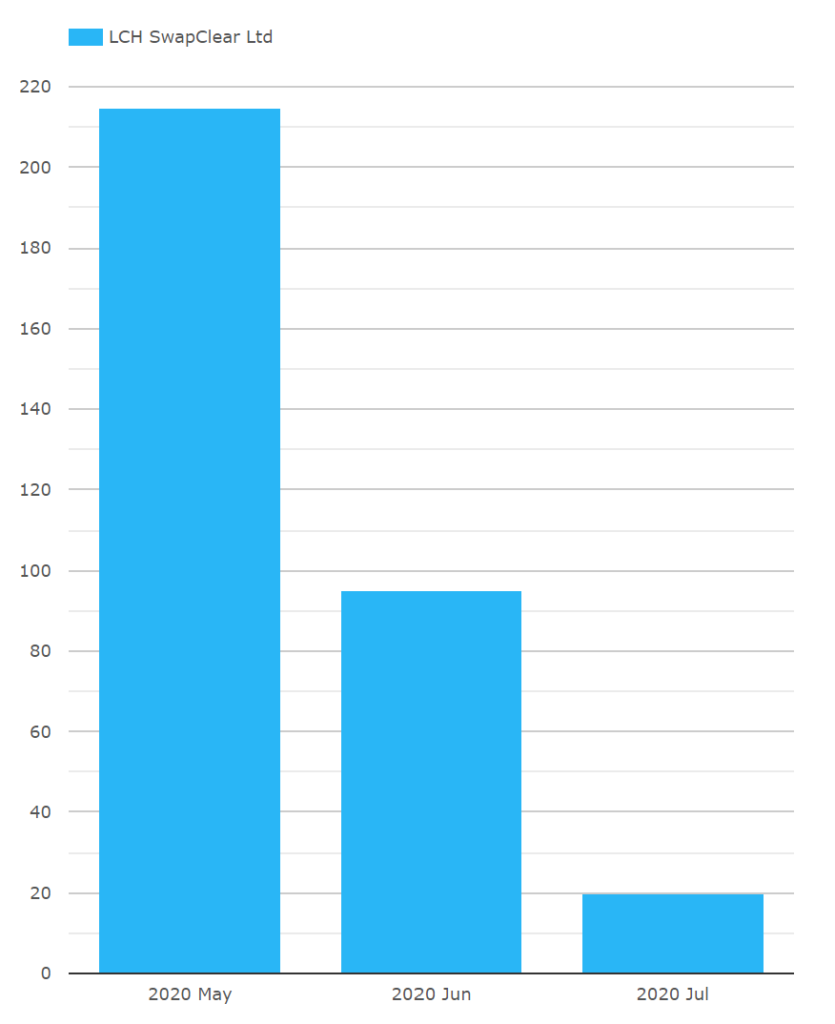

This blog will focus on the fallbacks for SOR, but it is equally important to note that the SGD RFR, SORA, has now started to trade:

As with SOFR, it looks like the market waited for a Cleared solution before trading this new benchmark. From CCPView, we can see that activity in SORA swaps remains somewhat sporadic, which is to be expected with a new index:

What You Need to Know

In terms of SGD Rates markets:

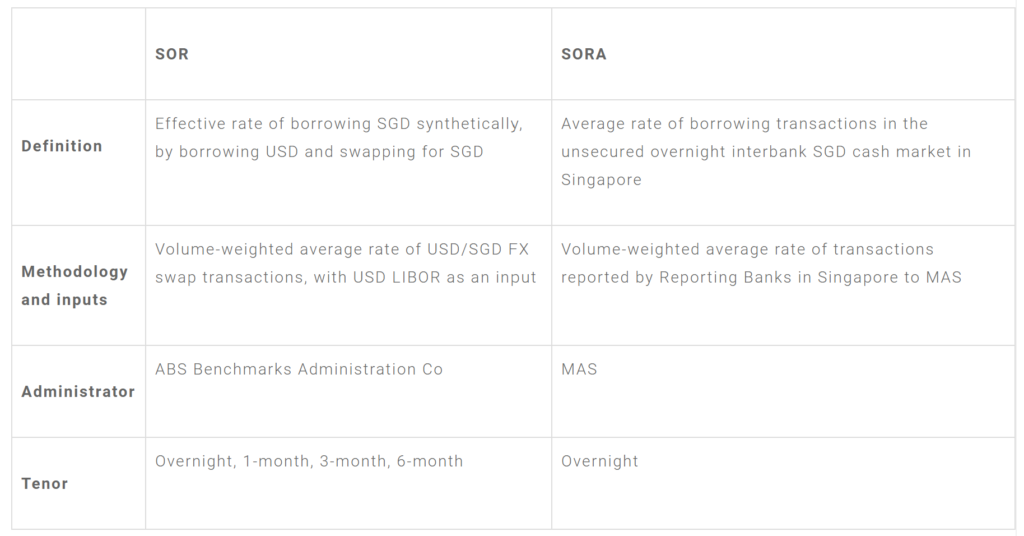

- SOR is the dominant index.

- It is currently derived from a combination of FX Fwd points and USD Libor fixings, to create a synthetic SGD rate. If this is news to you, please check out our original blog on SGD Rates for more background.

- Any cessation event in USD Libor will therefore also impact SOR.

- It therefore makes a lot of sense for trading to transition to the anointed Risk Free Rate in Singapore. This is SORA.

- SORA is administered by MAS and is calculated as the volume-weighted “average rate of borrowing transactions in the unsecured overnight interbank SGD cash market in Singapore”.

- It is therefore quite different to SOR, as summarised in the table below:

And in terms of Fallbacks related to SOR:

- A “Fallback Rate (SOR)” will be calculated and published following any cessation event in USD LIBOR.

- Fallback Rate (SOR) uses the USD LIBOR fallbacks, as published by Bloomberg.

- Recall that the USD LIBOR fallback is a compounded in-arrears SOFR rate plus the relevant spread adjustment for the tenor of LIBOR.

- However, Fallback Rae (SOR) will still be an FX Implied rate, as per the formula below:

\( \tag {1} Fallback Rate (SOR) = \left( \dfrac{Forward Rate}{Spot Rate} . \left( 1+ \dfrac{USD Libor . NoDays}{360} \right) -1 \right) . \dfrac{365}{NoDays} . 100\)

- The complete methodology is here for Fallback Rate (SOR).

- In the document, ABS notes that the Fallback Rate (SOR) will be published in-arrears, after the USD LIBOR fallback rate is published.

- This in effect means that ABS will use FX Fwds transacted value T+2, and then will have to wait until the expiration of those FX Fwds before being able to publish the rate.

- For example, 6 month Fallback Rate (SOR) will be published 6 months after the date on which the FX Fwds are actually observed:

Importantly, ABS are suggesting that Fallback Rate (SOR) is not used as a reference rate for any new derivatives. The website states (our emphasis):

Market participants are strongly discouraged from entering into new contracts that reference Fallback Rate (SOR), as it is only intended to facilitate the winding down of legacy SOR contracts where needed.

Fallback Rate (SOR) will be discontinued after about three years following the fallback trigger

ABS SOR discontinuation and contractual fallbacks

Fallback Rate (SOR)

With the methodology well understood, it just leaves us to point out the concerns that we raised when this original plan went to consultation.

Last year we responded to the ISDA consultation covering fallbacks in SGD markets. ClarusFT was the European non-financial corporation referenced below:

This concern of ours still applies. ABS have acknowledged this in their documentation, and highlight the following:

Notably, with Fallback Rate (SOR) more similar to and correlated with SOR relative to fallback rates based on SORA, the use of Fallback Rate (SOR) as the fallback reference rate would reduce the risk of value transfer and is expected to receive greater market support.

ABS SOR discontinuation and contractual fallbacks

And whilst they highlight the following risks…

This is different from SOR, LIBOR and other IBOR rates, which are “forward-looking rates” that embed a term premium and are typically available well ahead of interest payment dates. The switch from forward- to backward-looking reference rates will have implications on a range of processes from settlement, to accounting, and risk management, which market participants should be prepared for.

ABS SOR discontinuation and contractual fallbacks

….we would also strongly recommend that market participants consider the economic implications of using forward-looking FX rates combined with a backward-looking compounded in-arrears SOFR rate.

If you cannot trade out of your existing SOR exposures, then we understand the need for a fallback to act as a safety net. However, market participants need to accept that some safety nets are different to others.

On a positive note, the design of Fallback Rate (SOR) may lead to a particularly enthusiastic uptake of the new SORA index!

In Summary

- If there is a cessation event in USD LIBOR, it will impact how the current benchmark for SGD rates, SOR, is published and calculated.

- Fallback Rate (SOR) will be published in response to any cessation event in USD LIBOR. This new rate will use the SOFR-based fallbacks for the USD LIBOR component.

- Fallback Rate (SOR) will mix forward-looking FX forwards with backward-looking compounded in-arrears USD SOFR to create a synthetic SGD rate.

- It is intended only as a fallback and new contracts should not be written against it.

- The risk free rate in SGD, SORA, is a transaction-based RFR.