- Singapore has unique benchmark interest rates.

- SOR is an FX-derived synthetic SGD interest rate from FX swaps.

- SOR will therefore be impacted by changes to USD LIBOR as a result of the latest ISDA consultation.

- Cross Currency in SGD trades versus the SOR index. Why isn’t the basis therefore zero?

Singapore Interest Rates

In response to the latest ISDA Consultation, I have been educating myself about SGD benchmark interest rates.

Why?

Unlike most major currencies, Singapore has two benchmarks – SGD SIBOR and SGD SOR (Swap Offer Rate).

My first port of call is therefore SDRView to see which indices actually trade. First in SGD Interest Rate Swaps:

Showing;

- SGD Interest Rate Swaps are reported versus two indices “SGD-SOR-Reuters” and “SGD-SOR-VWAP”.

- So far as I can tell, these are the same index just going under different names.

- SGD SIBOR doesn’t get a look-in.

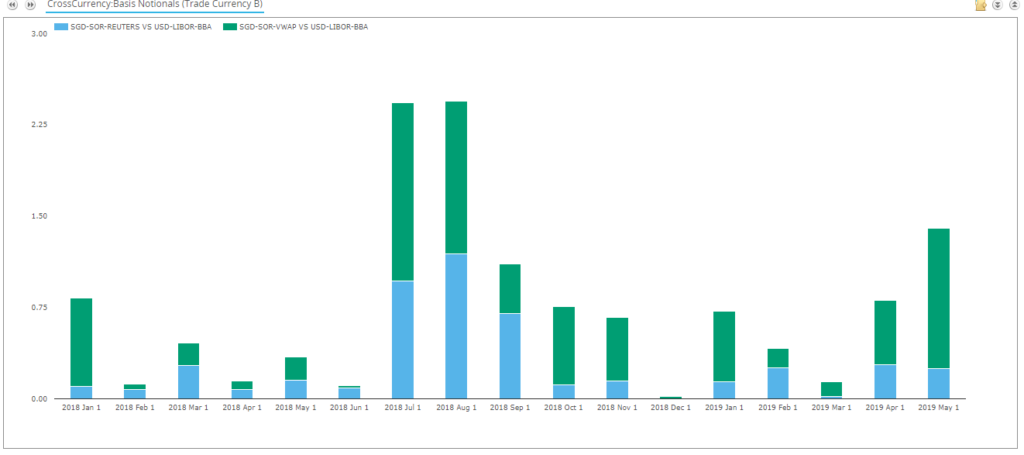

Given there was no SIBOR activity in IRS, I also checked Cross Currency Swaps to see what trades:

Showing;

- Again, there is only activity vs SGD-SOR.

- Given that SGD SIBOR doesn’t really trade, the current ISDA consultation is therefore relevant for virtually all SGD derivatives.

- Checking against the LCH SwapClear website, they only clear SGD-SOR-VWAP, and this is also true at CME.

What is SGD SOR?

Now we know what is trading in SGD dollars, let’s look at what the index actually is.

Administered by the Association of Banking in Singapore (“ABS”), and calculated by Refinitiv, SGD SOR is a:

Synthetic rate for deposits in SGD, which represents the effective cost of borrowing the SGD synthetically by borrowing USD for the same maturity, and swap out the USD in return for the SGD.

ABS Co Rate Setting Benchmarks at www.abs.org.sg

As regular readers will know, this is music to my ears! An FX-derived rate! For an ex-cross currency trader and a previous supporter of such rates, I really should have already known that this was the calculation methodology.

Gaping holes in my knowledge aside, this means that SOR will be impacted by any changes to USD LIBOR.

SGD SOR Calculation Methodology

The benchmark administrator provides plenty of transparency about the calculation methodology. For those unfamiliar with how to imply interest rates from FX Forwards, the calculation is as follows:

\( \tag {1} SGD SOR = \left( \dfrac{Forward Rate}{Spot Rate} . \left( 1+ \dfrac{USD Libor . NoDays}{360} \right) -1 \right) . \dfrac{365}{NoDays} . 100\)

This basically says that an FX Forward rate is equal to the interest rate differential between the two currencies. If you know the interest rate in one of the currencies (in this case USD), then you can imply the other interest rate.

Crucially, the FX Forwards are based on real transactions. I have no idea how representative they are of the overall market, but we do know from the ABS which transactions are included:

- Notional >= $1m.

- At least one side is in Singapore and both are considered “interbank” counterparties.

- Electronically traded via an Approved Broker (i.e. registered with MAS) between 7:30am to 4:30pm Singapore time.

Handily, ABS even provide a worked example. They have included 9 trades in their calculation of the Volume Weighted Average. 9 trades? Okay, this is for a 6 month tenor, so relatively long for FX trades, but I still hope we are talking about more daily transactions than that!

USD LIBOR changes and their impacts on SGD SOR

SGD-SOR, at the moment, therefore provides a great example of how to use the most liquid instrument (in this case FX forwards) to provide a transactional base for benchmark interest rates.

The problem is what happens with the term USD LIBOR element of the calculation.

Why is it a problem?

The FX Forward is a forward-looking measure of market expectations for the interest rate differential (USD vs SGD) for the term of the trade. If the USD Libor fallback means it becomes a compounded in-arrears rate, the USD rate is then an observed, backward-looking rate. Can we really mix a forward looking rate with a backward looking one?

In the ISDA consultation, the proposal is to use the fallback methodology for USD LIBOR to replace the USD rate in the calculation. We would then be mixing forward-looking FX Forwards with a backward-looking USD rate (assuming that compounded in-arrears is chosen).

I probably shouldn’t express an opinion on the consultation here. So below is another option for SGD SOR:

- SGD SOR Term rates become the SGD SOR overnight rate compounded in-arrears (plus a spread).

- The historic spread is calibrated via either;

- Historic Term SGD SOR versus the compounded historic SGD SOR overnight fixing.

- Historic Term SGD SOR versus the compounded historic implied SGD SOR versus the observed SOFR rate.

- Going forward, the SGD-SOR overnight rate would use forward-looking tom-next swaps but use the appropriate USD SOFR or USD Fed Funds fixing once it is known. Hence the time of publication would be aligned with the USD SOFR publication time.

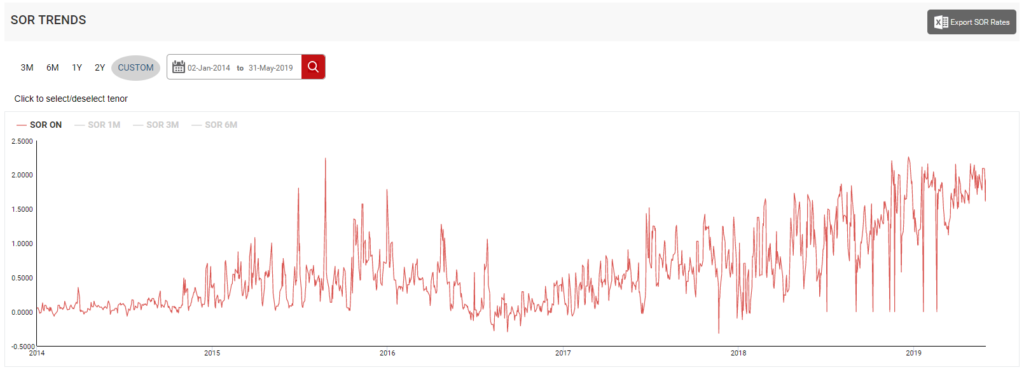

Overnight SGD SOR

The time-series of Overnight SOR is shown below, from the ABS website:

As we saw with NOK rates and the suggested NOWA methodology, using FX markets to imply an overnight rate results in a very volatile time-series. This tends to be at odds with some of the desirable properties of a reference rate that the NoRe guidelines stated:

Will an overnight SGD SOR rate qualify against those criteria? I’m not so convinced that it will be “sensitive to key policy rate” or “correlated with other money market rates”?

However, is it preferable to using a realised, backward-looking USD rate to imply a rate? We will wait for the response to the ISDA consultation to see what other market participants have to say.

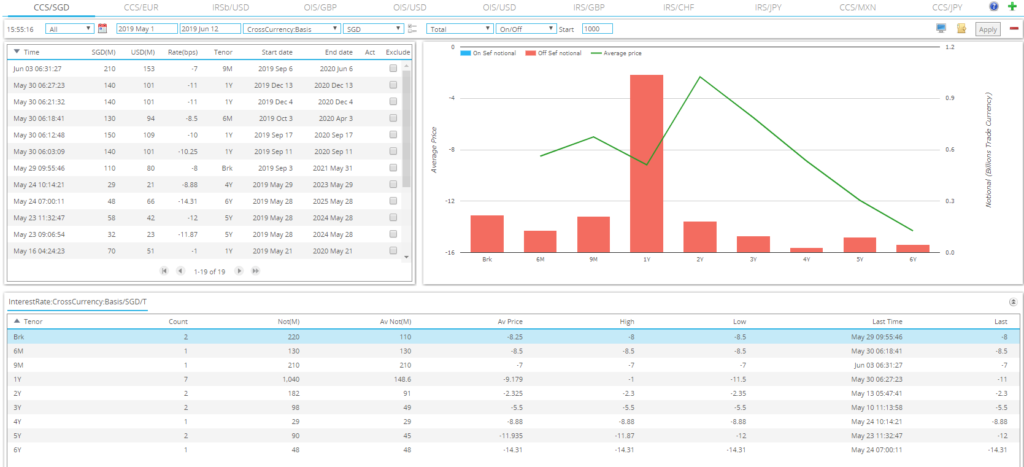

Cross Currency Basis in SGD

Having completed my crash-course in SGD SOR mechanics, I got particularly excited about Cross Currency Basis. At first pass, I assumed it would be at zero across all tenors, because the (existing) SOR calculation incorporates the implied cross currency basis at each roll period.

I couldn’t have been more wrong. There is indeed a term structure of SGD basis, shown below from SDRView Pro for the last traded prices:

After a bit of head-scratching, my conclusions as to why the cross currency basis is not at zero are:

- Term funding for Singaporean banks in USD carries a significant premium.

- The mark-to-market pain felt on a 5 year leg (for example) is too great to cope with carrying/rolling the first three/six month period on each roll date.

- Given that a Singapore bank has to be one side of the FX transaction making up the SOR VWAP, maybe they are consistently net borrowers of USD in the interbank FX market?

In terms of impact, I imagine number (1) significantly outweighs both (2) and (3).

This is a great real-world case study for basis and funding markets. USD-implied domestic rates still do not eliminate cross currency basis! The term premium of raising cash for such long periods (5 years plus) – even when that cash is collateralised in a foreign currency – is clearly significant.

We probably knew that already, but SGD-SOR serves to quantify and exemplify it.

In Summary

- Most SGD derivatives reference SGD SOR.

- SGD SOR is a domestic SGD interest rate that is implied by FX Forwards via USD LIBOR.

- If USD LIBOR ceases to exist, the USD rate in the FX calculations may need to be replaced.

- Alternatively, overnight SGD SOR could be compounded in-arrears.

- SGD SOR provides a fascinating case study for Cross Currency Basis and the term premium of funding markets.