There are some blogs I look forward to writing – this is one of ’em!

Circled in our diaries for quite some time has been Tuesday September 21st. This is when the Cross Currency Swaps market is expected to follow the lead of the recent SOFR First initiative and start the transition away from LIBOR products to RFRs. Of course, this is much more complex in Cross Currency given we are talking about two currencies.

The Bank of England and FCA kicked off the announcements on July 21st:

The specific ask of market participants is:

Specifically, the quoting conventions in the interdealer market for the GBP, CHF and JPY legs of cross-currency swaps would switch from LIBOR to SONIA, SARON and TONA respectively from 21 September.

Cross-currency swaps with a USD leg would switch from USD LIBOR to SOFR from 21 September when paired with another LIBOR currency i.e. GBP/USD would switch to SONIA/SOFR, CHF/USD to SARON/SOFR and USD/JPY to SOFR/TONA.

If the USD leg is paired with a non-LIBOR currency, or IBOR, then in line with the US authorities’ guidance on the timing for ceasing new use of USD LIBOR, the USD leg would switch to SOFR as soon as is practicable from 21 September and no later than the end of 2021.

https://www.bankofengland.co.uk/news/2021/july/fca-boe-encourage-market-participants-in-a-switch-to-rfrs-in-the-libor-cross-currency-swaps-market

Therefore today we will use the public data available from US SDRs to monitor whether CHFUSD, JPYUSD and GBPUSD have indeed transitioned to RFR vs RFR for Cross Currency Swaps. This is all taken from our data app sdrviewrt.clarusft.com/#RTView:

10:30am London

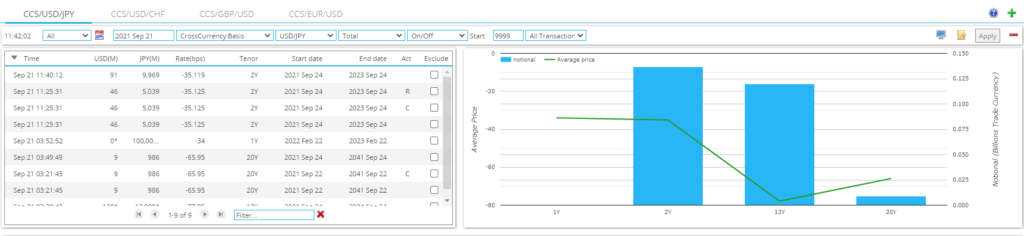

So far today I see 3 trades in USDJPY, 1 in GBPUSD and 1 in CHFUSD. How successful has the switch to RFRs been for these trades?

The simple answer is – VERY. 100% of trades reported to SDRs in these 3 currency pairs have been RFR vs RFR today. That is a great achievement for the market.

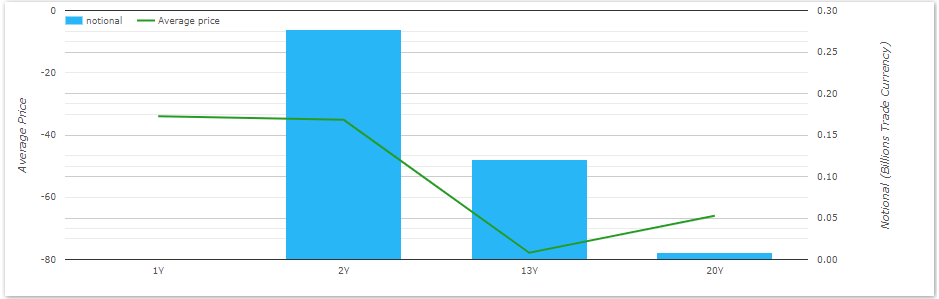

- In USDJPY, forward starting 1Y, spot starting 13Y and spot starting 20Y have all traded as TONA vs SOFR.

- In GBPUSD, spot-starting 2Y SONIA vs SOFR has traded.

- In CHFUSD, spot-starting 4Y SARON vs SOFR has traded.

Interestingly, those last two trades were cancelled and rebooked a couple of times, suggesting there are still some minor teething problems to make sure they are booked accurately!

10:45am London

More trades are ticking in:

- 2Y USDJPY has traded twice at -35.125 and both were TONA vs SOFR.

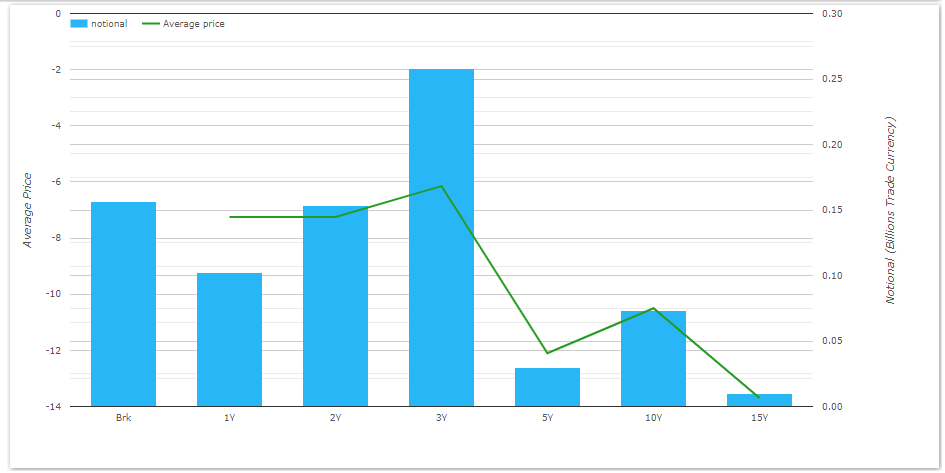

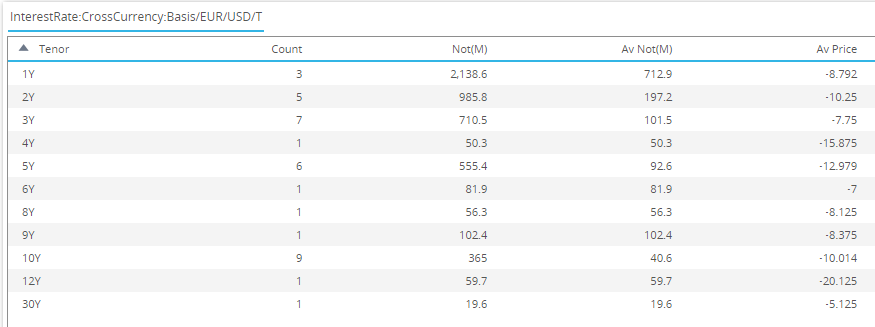

- 3Y CHFUSD has just traded in block size…..and it is LIBOR based. Doh! Swissy – the first of the currencies to break our 100% record!

To be fair to the CHFUSD market, this one does look like a client trade rather than via an IDB (interdealer broker). It is forward starting out of 2025 and carries an upfront fee. That suggests it is an end-user trade and not executed in the interbank market. Hopefully it is risk reducing and therefore offsetting existing LIBOR exposures for both counterparties!

10:55am London

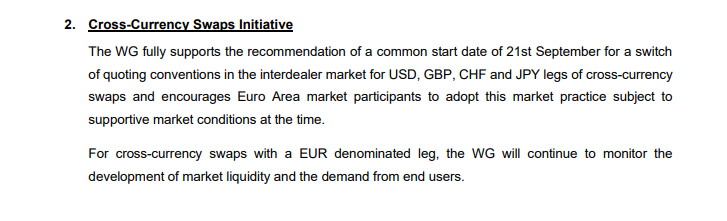

And what about the EURUSD market? Whilst the European Working Group for RFRs expressed support for the RFR first initiative, our keen-eyed readers will note that EURUSD, the largest currency pair, has not been part of this initiative. This is what the European Working Group said:

Interestingly, there have been 5 trades in EURUSD reported to US SDRs so far this morning. Every single one is EURIBOR vs LIBOR. There have been no RFR vs RFR EURUSD trades so far today.

This might be a great gauge of how successful the RFR initiative is being in JPYUSD, GBPUSD and CHFUSD! Or it might just highlight that market participants have enough on their plates today switching 3 currency pairs, never mind another.

Still, it will be intriguing to see if we do get some €STR vs SOFR trading as the US comes in later.

15:15 London

Moving later into the trading day and the success for the RFR First initiative in Cross Currency Swaps has really continued.

In GBP/USD:

- 10 trades, $783m notional.

- 90% have been SONIA vs SOFR.

- Activity from 1Y out to 15Y in RFR vs RFR.

The only trade that was LIBOR-based does look like a client trade, with a forward start date out of June 2023.

In JPY/USD;

- 6 trades, $406m notional.

- 100% have been TONA vs SOFR.

- Activity from 1Y through to 20Y.

Great to see such a successful transition today in JPYUSD!

In USD/CHF:

- 3 trades, $170m notional.

- 66% have been SARON vs SOFR.

- Activity in 4Y and 5Y for the RFR swaps.

It was nice to see that the earlier client trade wasn’t seemingly hedged in LIBOR space (or at least reported to US SDRs!).

And just a note on the data. This is by no means the whole of the global cross currency swaps market that we are seeing here. These are only the trades captured by the transparency regime in the US and hence are reported to US SDRs. We do believe that the activity is representative of the overall market and so the positives for the RFR First initiative should certainly be celebrated today!

16:15 London

We’ve had some more GBPUSD trades hit the SDRs – 7Y, £50m and 5y vs 10y in £50m. All were SONIA vs SOFR. Great to see this success in RFR trading continuing!

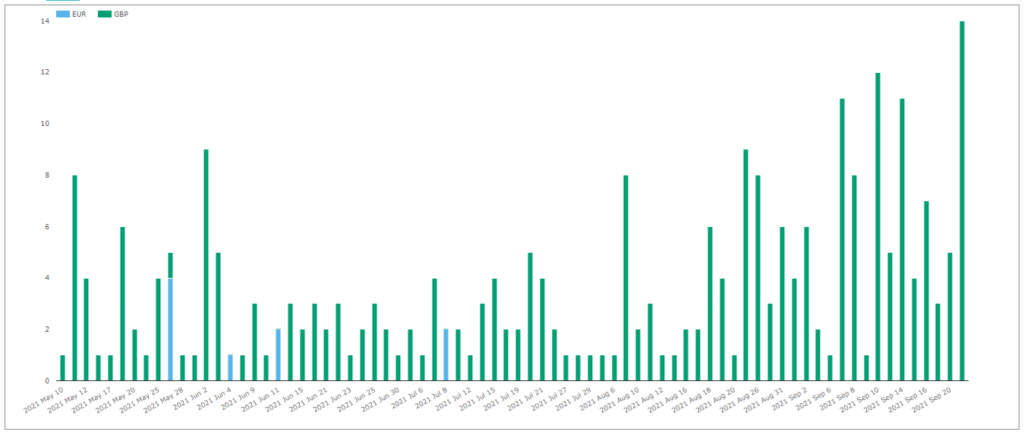

It is worth doing a stock-take on EURUSD as well. EURUSD as reported to SDRs is certainly the largest market of them all, and has seen 36 trades in total today. These are across both EURIBOR vs LIBOR and €STR vs SOFR:

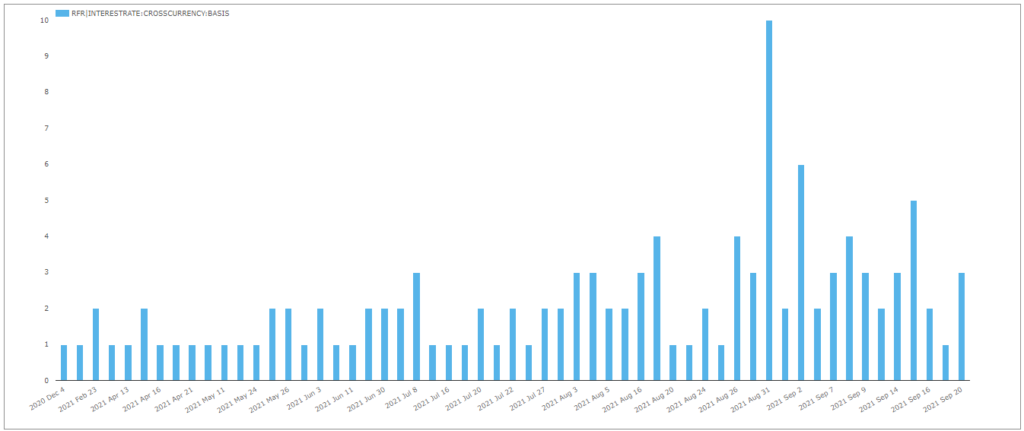

Of those 36 trades, 10 were in €STR vs SOFR. This is pretty good – 28% – and is actually only the second time we’ve seen as many as 10 €STR vs SOFR trades reported to SDRs on a single day. The last time was at the end of last month:

The data therefore shows signs that EURUSD is being impacted by the RFR First initiative as well. It’s great to have the data (at least for US markets) to be able to monitor these important changes in markets!

End of Day Wrap

As we look back at yesterday’s trading activity, we can see that RFR First in XCCY had a significant impact on the markets.

EURUSD

Despite EURUSD not being part of the initiative, there is some evidence that a degree of transition took place. More €STR vs SOFR was reported to US SDRs yesterday than ever before. Okay, it was only 11 trades, but it is something to monitor in the coming weeks/months:

GBPUSD

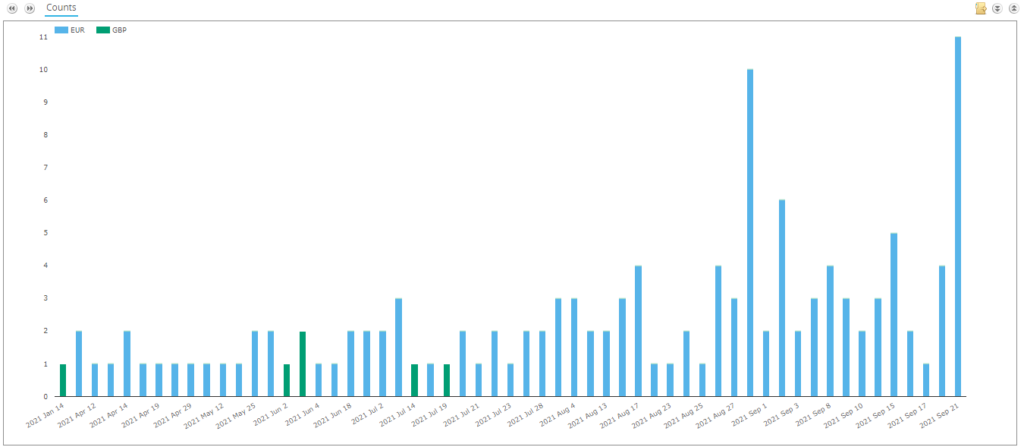

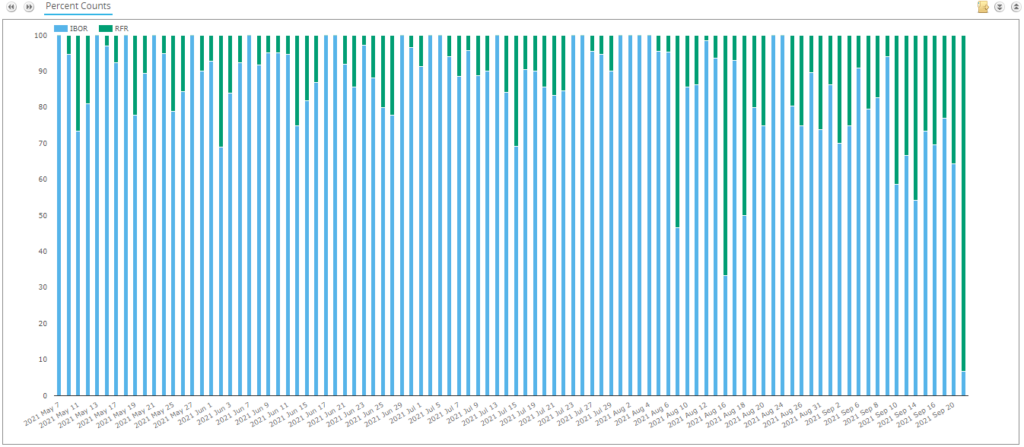

In GBPUSD, there were 14 SONIA vs SOFR trades reported to US SDRs. That doesn’t win the outright record as there were some large transition trades reported earlier this year, but it is the highest number since early May.

More importantly for GBPUSD markets, 93% of trades were reported as RFR vs RFR:

JPYUSD

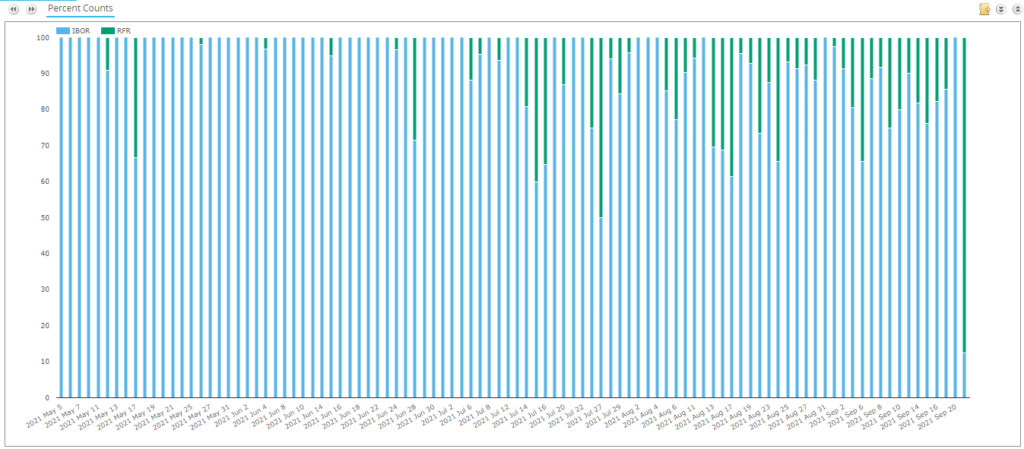

It was a quiet day of trading activity in JPYUSD overall, but we still saw 7 TONA vs SOFR trades reported. On a percentage basis, 88% of trades were RFR vs RFR, a new record:

CHFUSD

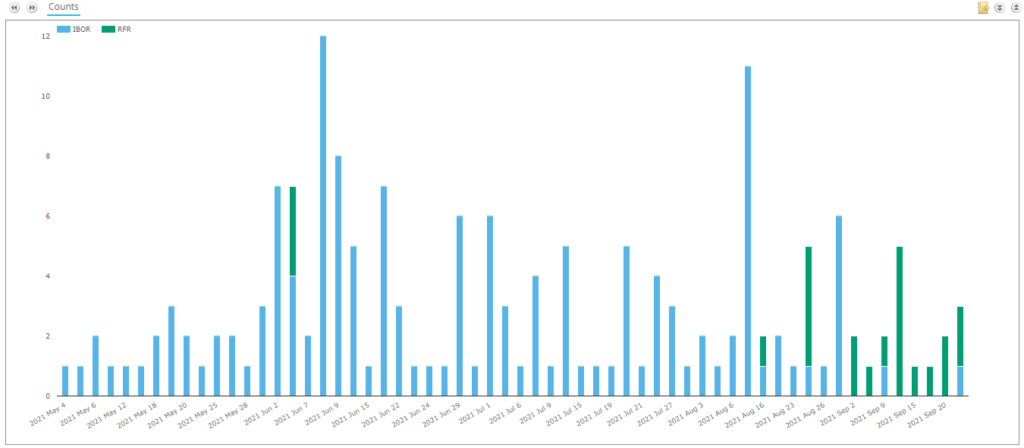

Last but by no means least, my local CHF market also had a successful transition day. There are never many trades in CHFUSD, but we’ve seen a gradual increase in SARON vs SOFR trading since the beginning of September. Whilst the numbers are low it is clear that transition is underway:

In Summary

- RFR vs RFR XCCY swaps accounted for 91% of activity in the LIBOR currencies (when measured by notional).

- LIBOR currencies saw 23 out of 26 trades reported to SDRs transacted RFR vs RFR.

- The 3 trades in the LIBOR currencies that were transacted versus LIBOR all looked like client trades, with additional fees attached and/or forward start dates.

- We consider RFR First in XCCY a success!

Finally, if we also include EURUSD in the stats, we see that 46% of XCCY swaps were traded as RFR vs RFR (by trade count). This is still a new all time high but is obviously skewed quite a bit lower by the inclusion of EURUSD in those statistics.

Is a market convention settled on already for rfr based cross-currency swaps? Do they also have 2 day payment delay like SOFR swaps for example? Are both interest and principal payments delayed, or is it interest only? What about if it is Euribor vs SOFR… Than would one leg be delayed settled and the other not?

Yes, RFR vs RFR XCCY trades with a two day lag on both coupons, so that the coupons have the same settlement date. All other cashflows settle on value date, so you have a two day lag between notional exchanges, FX Resets and coupons. I’ve not seen many EURIBOR vs SOFR trades, but I imagine the same should apply – 2 day lag on both legs for coupons only.

Pardon my rather dumb question. But in reference to Xccy swaps using RFRs how would it work?

SOFR, as I see is annual, whereas ESTR is Overnight compounded. Does this mean that the USD leg settles with an annual sofr rate where as ESTER is not known until the end of the trade?

If yes, how come, Refinitiv has ESTR/SOFR Xccy basis with a 3M pay frequency on both legs?

In other words, how does EURUSD 3M 3M basis work in lieu of different frequencies on both SOFR and ESTR?

As an example, a LIBOR based xccy basis can be derived from USD 6/3M basis, and EUR 3/6M basis. Is there such kind of basis for SOFR and ESTR?

Both SOFR and €STR are overnight rates, therefore XCCY swaps trade as compounded overnight rates on each side, with payments made quarterly.

Thank for your reply. I was actually checking on Bloomberg. Perhaps you could explain a bit? How come when you pull up a SOFR or ESTR swap, the pay frequency for these fixed/float show as annual, whereas a xccy basis on SOFR/ESTR is quarterly?

This brings me to the question whether there is some additional basis that also comes into play (for ex: when looking at fx implied yields for EURUSD)

Correct, OIS in SOFR and ESTR settle on an annual basis. Standard interbank RFR cross currency swaps settle quarterly. Remember the interest rates are daily compounded overnight rates, so there is not the same concept of term-basis here as in IBOR settings which also carry an unsecured credit exposure. I imagine that the Cross Currency Swaps chose to continue with quarterly resets for two reasons – 1) it follows on from the current IBOR-based swaps and changing fewer elements during the transition makes life simple and 2) RFR XCCY swaps still trade with FX resets, rebasing the FX rates every three months. This (potentially) reduces discounting risks on the swaps as the “off-marketness” is cash settled in USD every 3 months. Extending payments to annual would mean only annual FX resets, resulting in (potentially) larger discounting risks and larger sized FX Reset payments, increasing settlement risk. In reality, the change in risk from 3 month to annual gaps for FX resets would not be that great. However, it does help if the RFR XCCY swaps match the legacy portfolios of older swaps either on fallbacks or still on IBORs, such as older EURUSD swaps. Then at least the FX reset risk on new swaps offsets FX reset risk on old swaps as both reset every 3 months.