For my final blog of 2021, permit me a small amount of self indulgence. I will take a look at the Cross Currency Swaps markets and their reactions to the two waves of RFR First that we have had recently. It turns out I will always jump on any excuse to write about Cross Currency markets!

LIBOR Currencies

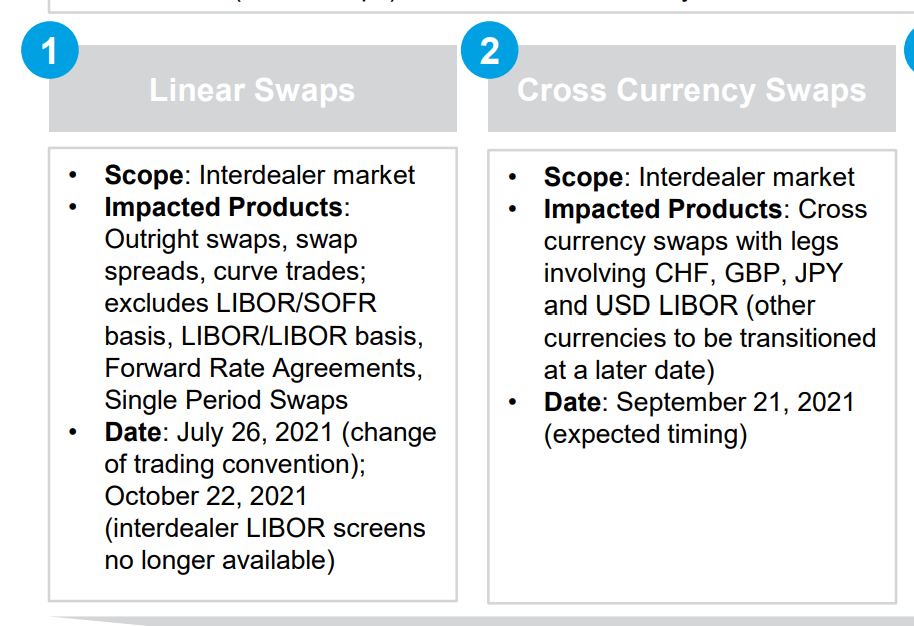

As we reported in our LIVE Blog from September, the CFTC’s MRAC kicked off the changes in Cross Currency Swap markets with an RFR first initiative targeting the LIBOR currencies – CHF, GBP and JPY.

As the Bank of England highlight in their announcement, this first phase of RFR transition in cross currency swaps would be the most “complete”, with both legs of the cross currency swap moving to RFRs:

The proposed change will involve IDBs moving the primary basis of their pricing screens and curve construction for cross-currency swaps from LIBOR to RFRs.

Specifically, the quoting conventions in the interdealer market for the GBP, CHF and JPY legs of cross-currency swaps would switch from LIBOR to SONIA, SARON and TONA respectively from 21 September.

Cross-currency swaps with a USD leg would switch from USD LIBOR to SOFR from 21 September when paired with another LIBOR currency i.e. GBP/USD would switch to SONIA/SOFR, CHF/USD to SARON/SOFR and USD/JPY to SOFR/TONA.

The FCA and the Bank of England encourage market participants in a switch to RFRs in the LIBOR cross-currency swaps market from 21 September

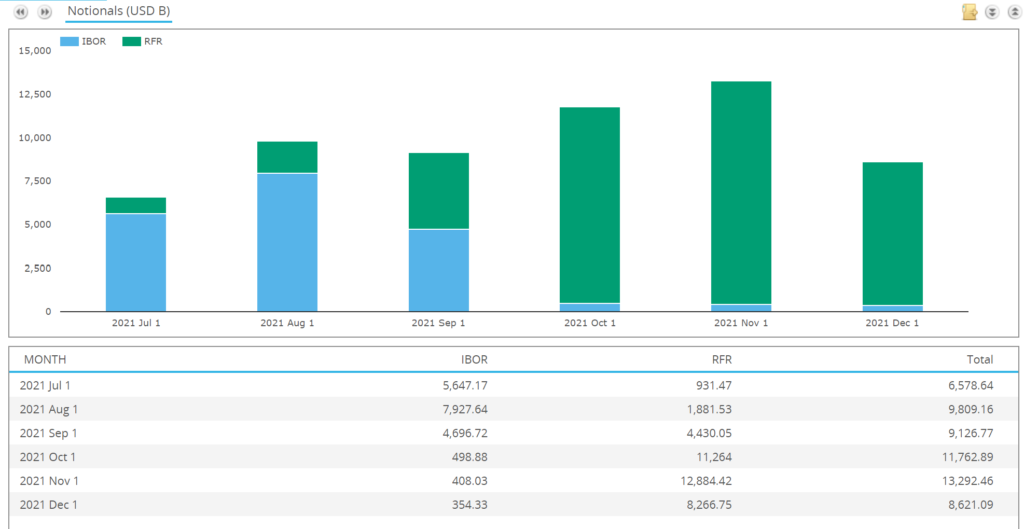

Let’s refresh the data and see how successful this move in Cross Currency Swaps has been:

We commented last week on how significant this move has been, but here is a bit more detail:

- The chart shows the volume of cross currency swaps traded in GBPUSD, CHFUSD and JPYUSD each month.

- The green bars highlight those volumes that include an RFR leg.

- When we drill-down into the trade-level details, we find that both legs are RFRs for these currency pairs.

- Over 95% of volumes have traded as RFR vs RFR in the past 3 months.

- Crucially, despite this significant change in traded product, volumes have actually been higher than in the previous 3 months (we are only partway through December as I write).

- Seeing higher volumes and a 95% uptake of new conventions can be considered a really healthy transition story for these currency pairs.

What About EURUSD?

EURUSD wasn’t explicitly included in the first wave of “SOFR First” for cross currency swaps. It was included in the latest move, which naturally covered all other currency pairs (with a USD leg).

This “Part II” of Cross Currency RFR first, was backed for EURUSD by the EUR RFR Working Group this month:

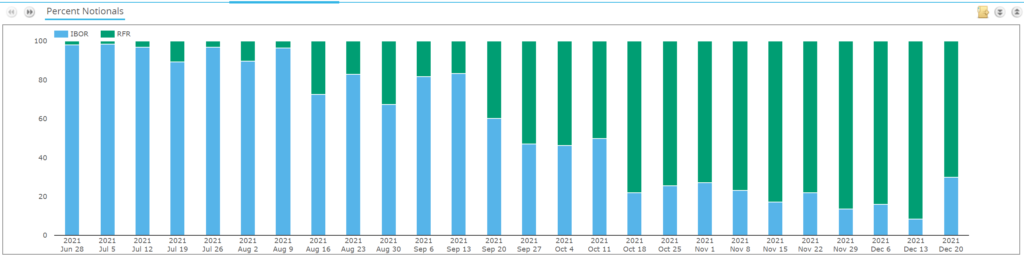

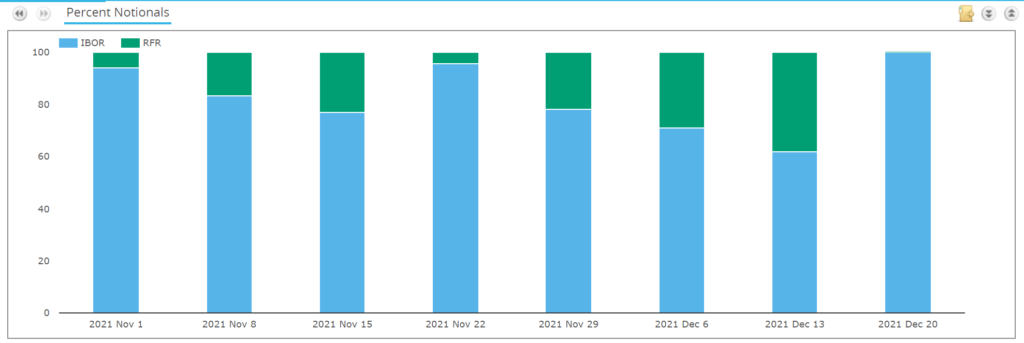

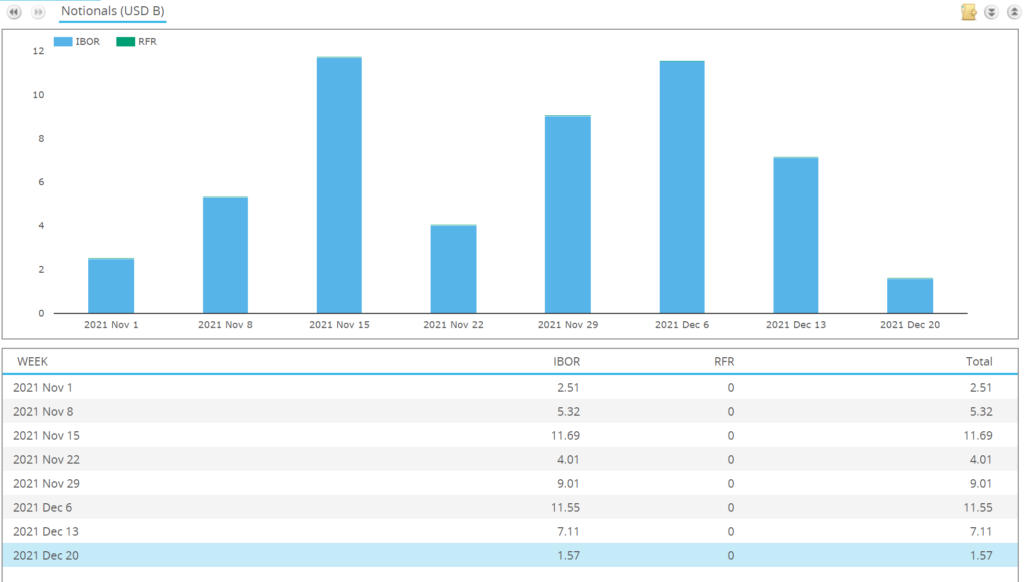

However, when we look at Cross Currency Swaps reported to SDRs, the adoption of RFR vs RFR (€STR vs SOFR) in EURUSD was well underway before this latest initiative:

Showing;

- The proportion of trades each week reported to US SDRs in EURUSD as either EURIBOR vs LIBOR (“IBOR”) or €STR vs SOFR (“RFR”).

- Any EURIBOR vs SOFR would show up in the RFR bars, but we have seen very few of these trades. And when I say few, I counted only 7 in the data!

- The data shows that by the middle of October, 78% of trades were already trading RFR vs RFR in EURUSD.

- And this has been fairly consistent ever since.

- Of course, EURIBOR is not going anywhere, but €STR is the preferred RFR.

The market appears to have decided that trading RFR vs RFR is preferable in EURUSD than trading Term vs RFR. This makes a lot of sense on a standalone basis (trading two similar indices).

However, the choice of index in any particular currency is far more likely to be down to liquidity considerations in other currency pairs.

CADUSD

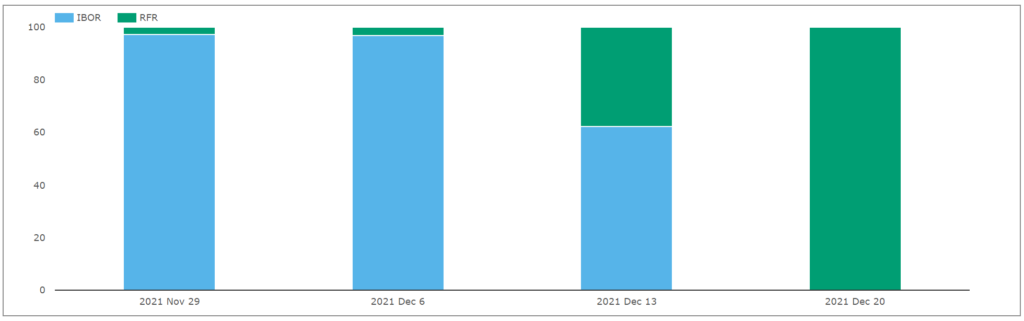

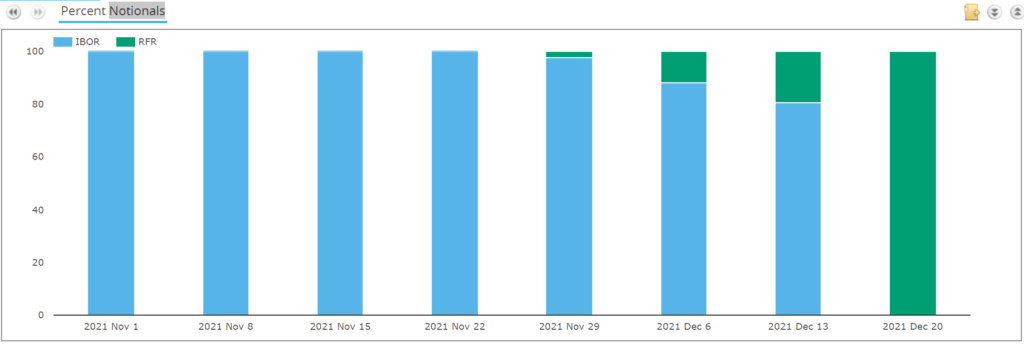

In CAD, market participants currently enjoy the choice of either CDOR or CORRA to trade versus the USD SOFR leg. After the December 13th RFR First initiative, we have seen a sharp increase in trading versus USD SOFR in CADUSD cross currency swaps:

Looking at the underlying data;

- 38% of volumes had a USD SOFR leg last week in CADUSD markets.

- We’ve only seen 5 trades reported so far this week, but all have been CDOR vs SOFR.

- There has actually only been one CORRA vs SOFR (i.e. RFRs on both legs) reported in the whole of December.

The CARR (Canadian RFR Working Group) announced on December 16th that they recommend the cessation of CDOR in June 2024, therefore I do wonder if we are due to see a pick up in CORRA vs SOFR trading next year?

AUDUSD

In AUD, market participants enjoy the choice of either BBSW (term, unsecured) or AONIA (overnight) to trade versus the USD SOFR leg. After the December 13th RFR First initiative, we have seen no significant change in market behaviour so far:

SHowing;

- AUDUSD trades with a SOFR leg already accounted for 15-25% of volumes in November this year.

- This has increased slightly to 38%.

- So far this week, we have seen only 3 AUDUSD trades reported, and all have been BBSW vs USD LIBOR.

- I do not see any AONIA vs SOFR trades recently. All of the “RFR” volumes above have been BBSW vs SOFR.

(As we look into other currencies (including AUD), it is worth noting that US SDR data does not cover the whole global market. However, USD SOFR adoption should be strongest amongst reporting US counterparties.)

Scandies

Let’s look at SEKUSD, NOKUSD and DKKUSD together. None of these currencies have developed RFR markets (yet), so any RFR volumes will be versus their domestic term rates (for now).

Showing;

- There is evidence that liquidity is moving to trades with a USD SOFR leg.

- 20% of trades had a USD SOFR leg last week.

- All 3 trades reported so far this week have been in STIBOR vs USD SOFR.

MXNUSD

MXNUSD shows a different story:

Despite MXNUSD basis volumes being almost twice as large as SEKUSD, there has been no move to adopt USD SOFR yet.

TRYUSD

Finally, we have to mention TRYUSD this week, don’t we? With the extreme volatility surrounding the currency, it is unsurprising to see no transition so far!

This has always been an interesting one for me, because volumes are in Fixed TRY vs USD LIBOR 3m. What will the USD leg transition to? I imagine the 3 month USD LIBOR index was chosen because when lending to a local you want the USD payments as frequently as possible (to minimise credit risk associated with lending the USD). It wouldn’t surprise me if the USD SOFR leg adopts monthly payment frequencies when the transition does occur to minimise credit risks even further. The annual TRY leg effectively gets USD collateralised over time in this structure, even without a CSA in place.

And on and on and on…

I haven’t even started to cover HKDUSD, SGDUSD, NZDUSD etc etc etc. But I will leave that to our subscribers (and probably an update in Q1 2022!).

I will instead wish you all a very happy New Year.

Thanks for reading and we look forward to seeing you back on the Clarus blog in 2022.