Our recent blog, CCP Basis – The Cost of Clearing Fragmentation, proved very popular and while this was published on July 30, 2019, it was actually written a few weeks earlier. As is often the case with these things, there have been major new market developments in the CME-LCH Basis, meaning we need to do another blog on the same topic.

An indicator of how unusual this is can be inferred from the number of blogs we have published each year on CCP Basis, one in 2019, one in 2018, two in 2017, five in 2016, eleven in 2015 and one in 2014.

Time to double our 2019 count.

Background

For Swaps that are economically the same, it is non-intuitive that the fixed rate should be different depending on which CCP clears the trade. If I am paying Libor 3M every quarter on a trade, I expect to receive the same stream of fixed cash-flows on another trade done at the same time with the same economic terms.

We have covered the reasons for the price difference due to the CCP in a number of blogs (see here and here). In summary these boil down to an asymmetry between payers and receivers at a CCP, requiring dealers to hedge at a different CCP and paying two lots of gross margin; the cost of which they need to recover in the price charged to the customer.

CME-LCH Basis Spreads

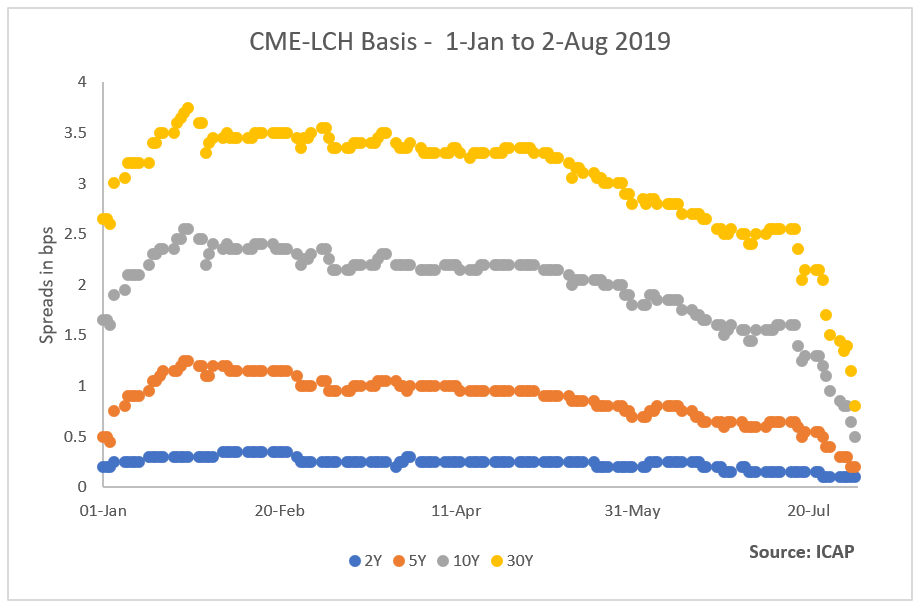

Let’s start with 2019 daily prices for major tenors, provided courtesy of ICAP.

- 30Y starting the year at 2.65 bps, rising to a high of 3.75 bps on 25-Jan, down to 3.45 bps on 1-Feb, flat-lining to 3.3 bps until 3-May, then drifting down 2.55 bps on 16-Jul, before dropping sharply on five days (17-Jul, 18-Jul, 25-Jul, 26-Jul, 1-Aug and 2-Aug) to end at 0.8bps!

- Wow that is the kind of move and level that we have not seen since Sep 2015.

- [Update on 5-Aug, we see a further drop for 30Y to 0.3 bps]

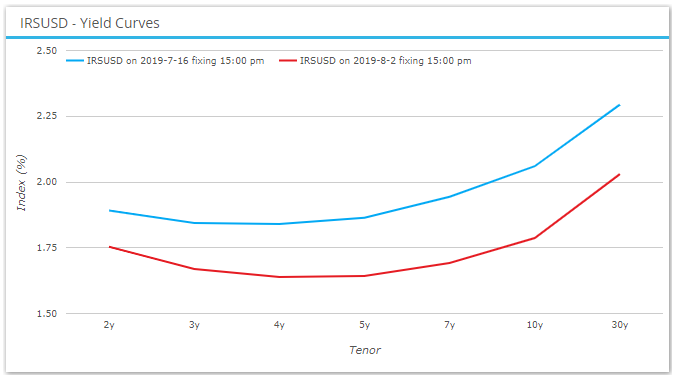

- Note also that Swap rates themselves dropped significantly over this period with the 10Y down -5bps on 17-Jul, -10.5 bps on 1-Aug and -6 bps on 2-Aug, for a cumulative drop over this period of -27 bps to end at 1.7870% from 2.06% on 16 Jul

- (See chart below, at the time of writing on 5 Aug, looks like a further drop of -10bps).

- 10Y basis spreads with the same trend as 30Y, starting the year at 1.65bps, up to 2.55 bps, flat-lining to 2.2bps, then drifting down to 1.6bps on 16-Jul, before dropping sharply to 0.5bps on 2-Aug

- Again a level the 10Y has not touched since Sep 2015

- [Update on 5-Aug, we see a further drop for 10Y to 0.1 bps]

- 5Y starting the year at 0.5bps and 0.2bps on 2-Aug

- 2Y starting the year at 0.2bps and 0.1bps on 2-Aug

- Both lowest levels since Sep-2015

Reason Why?

Searching for an explanation for the move, we hear the following:

- LCH SwapClear announced a change to its Initial Margin for Clients on 14 June 2019 that took effect on 22 July 2019, right around the sharp drop dates. This resulted in an increase of Client IM, restoring it closer to historic levels (see here for details). The maximum theoretical level of the increase was 18% (as SQRT(7/5)-1), in reality it would have been lower at an aggregate level, perhaps half that or 9%.

Why this would have resulted in a narrowing of the CME-LCH basis is open to conjecture.

One line of thought would be that the larger difference in client IM between CME and LCH, resulted in an increased preference from clients for clearing at CME and dealers competing in providing these prices were able to hedge at CME or decided not to pass the margin costs on to clients.

The drop in Swap rates was most likely also a factor as would have resulted in clients re-positioning their portfolios and needed to trade more.

Another explanation could be linked to Boris Johnson becoming UK prime minister on 23 Jul 2019, a sharp increase in the odds of a no-deal Brexit and a sudden drop in the value of GBP, which is the base currency for LCH SwapClear IM. However I am less sure of this one, as Brexit can be a convenient dumping ground for all manner of things.

In addition CME and LCH also announced a change to SOFR PAI discounting (from FedFunds):

- CME announced that this will take place on July 17, 2020.

- LCH announced this will take place on October 17, 2020 (see Risk.net)

This will cause a 3-month period of basis between LCH Fed Funds PAI and CME SOFR PAI, assuming both CCPs stick to their dates. (I would have thought members would want these CCPs to align their dates). This difference is likely to result in further moves in the CME-LCH Basis for USD Swaps next year.

If anyone has better explanations for the CME-LCH basis moves we have seen in the last two weeks, please add a comment to this blog below or contact us.

Next lets turn to what the data shows.

Cleared Volumes of USD Swaps

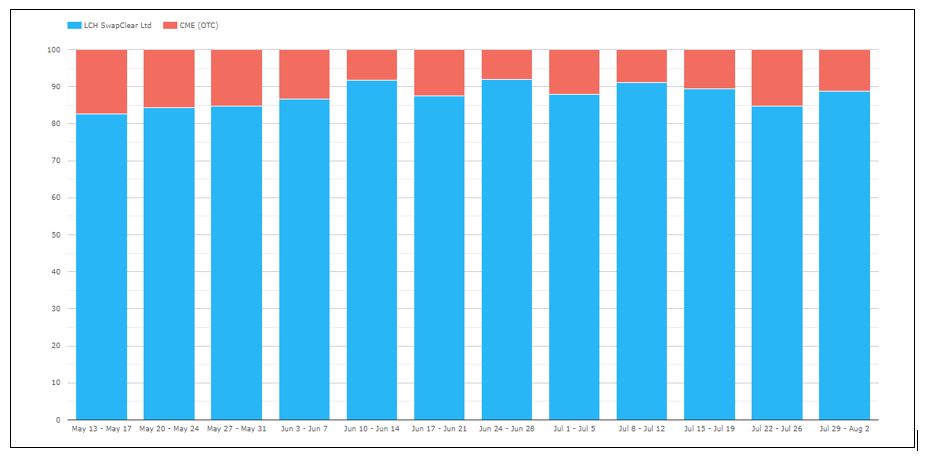

In CCPView we track daily volumes and open interest of Swaps at CME and LCH, so lets looking closely at this for the period in question. Starting with weekly volumes for the past 12 weeks, and focusing on the market share percentage of LCH SwapClear and CME OTC IRS for USD IRS.

This shows CME up in the week of 22-26 July (the second week of the sharp drops in basis) and while the share of 15.4% to 84.6% to LCH is a jump from the prior few weeks, it is similar to the CME vs LCH share in May.

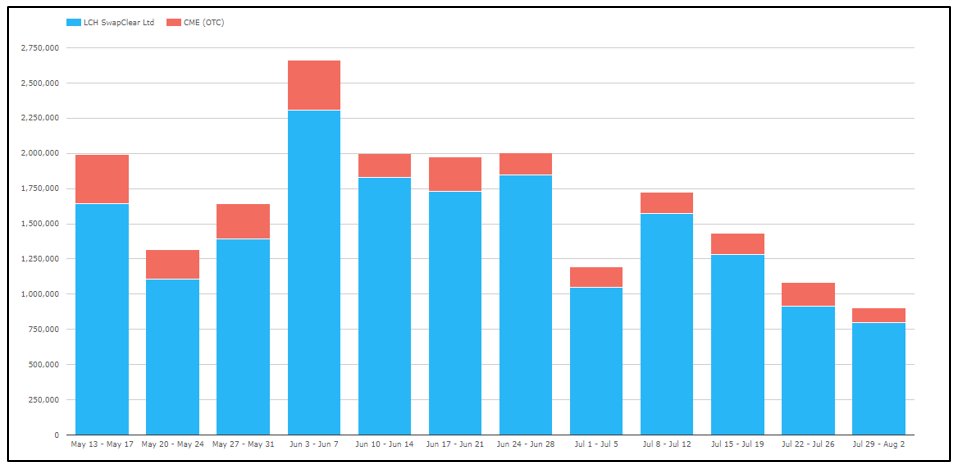

Switching the above to gross notional volumes, shows the last two weeks with low volume, par for the course in summer months.

So not a lot to see in volumes, but definitely worth keeping on eye on these.

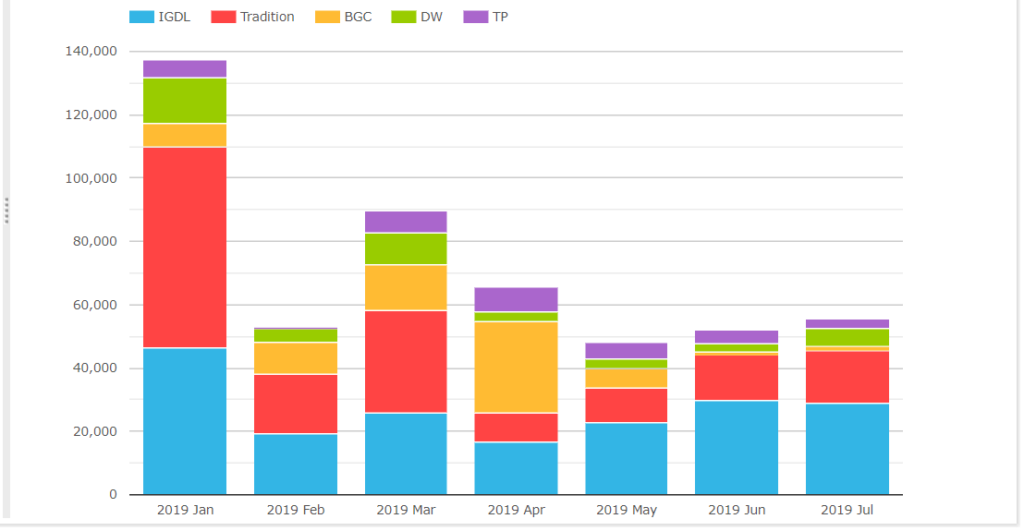

CCP Switch Trades

The market is also active in CCP Switch trading between CME and LCH and in SEFView we can track this volume. Let’s do this and show the notional in 5Yr Swap Equivalents.

Showing July 2019 is an average month. IGDL (ICAP) has the highest volume over this cumulative period and in each of the past four months, followed by Tradition.

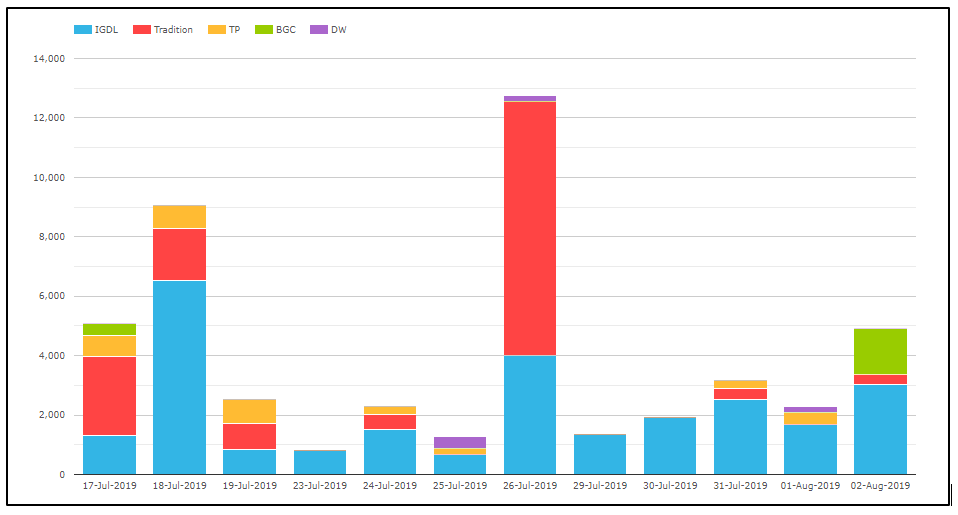

Lets look next at daily volumes for the 16-Jul to 2-Aug period.

This time we do see large spikes on 17 July, 18 July and 26 July, which are three of the four dates that we observed large drops in the CME-LCH Basis Spreads. These volumes look like dealers switching some CCP risk, but in themselves they are not large enough or unusual enough to influence the basis level itself.

Final Thoughts

The CME-LCH Basis has narrowed significantly in the last two weeks.

It is now down to levels last seen in Sep 2015. (30Y from 2.5 bps to 0.3 bps).

We suggest an explanation is the recent LCH Client IM change.

We see no material shift in volumes between CME and LCH.

But this is one to look out for over the next few months.

Last week we covered a quantitative model for the level of a CCP basis.

The question now is where will the Basis go next?

As I write this I can see that 30Y is showing 0.3 bps and 10Y 0.1bps.