We occasionally still get asked about the price differential between CME and LCH swaps. I typically refer folks to our online articles that have explained the phenomenon. Since 2014, we have written 18 separate pieces on the CME-LCH basis spread. A few of the ones that begin to quantify it include:

- May 20, 2015 – Reasons the basis exists

- May 26, 2015 – Hedging the CME-LCH Basis

- June 22, 2015 – Arbitraging the CME-LCH Basis

Since that time, our clients have begun using tools that can quantify and optimize their CME-LCH basis positions.

So I wanted to dumb it all down to try and explain the primary cost-related driver behind it.

Step 1.

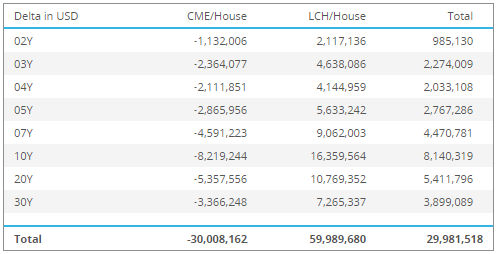

Let’s take a theoretical swap dealers portfolio that meets the hype. That is, the bank is fixed-rate payers at LCH, and fixed-rate receivers at CME. Their USD 3M Libor delta ladder might resemble something like this:

Pro-Tip: The theory goes that the reason Banks are fixed rate receivers at CME is that most buy-side institutions caught by the clearing mandate are payers (and hence the dealer is a receiver). For further reading on this, you can catch up on the buy-side institutions that are natural receivers, but are not caught by the clearing mandate: Should Bond Issuers take advantage of the CME-LCH Basis

Pro-Tip: The theory goes that the reason Banks are fixed rate receivers at CME is that most buy-side institutions caught by the clearing mandate are payers (and hence the dealer is a receiver). For further reading on this, you can catch up on the buy-side institutions that are natural receivers, but are not caught by the clearing mandate: Should Bond Issuers take advantage of the CME-LCH Basis

Step 2.

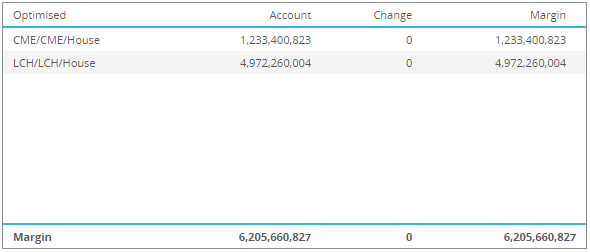

Now let’s run an initial margin calculation on these portfolios. In true “For Dummies” fashion – don’t try this at home, it’s a complicated HVaR calculation with various parameters tweaked. The CHARM tool does the calcs and gives us:

So that is saying we have to give CME $1.2bn, and LCH nearly $5bn of margin collateral (cash or securities). There is of course an opportunity cost for handing over all of this cash and securities.

Pro Tip: The CCPs will arrange finance charges for your collateral. So they might pay you an overnight interest rate on cash you pledge, or charge you for the hassle of holding onto your securities while you still collect coupons on them.

Step 3.

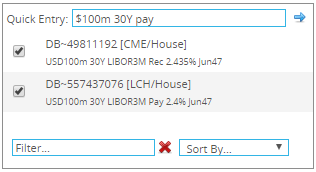

Now let’s assume you (the buy-side guy) call up and ask the bank to trade a swap. Of course you want to be a fixed-rate payer (“Rates can only go up!”). The bank now looks at what would happen to these margin obligations they have to the 2 clearing houses if they did that trade (bank would receive fixed at CME), and at the same time chose to offload that same swap at LCH (by paying fixed at LCH).

So these two trades are modeled:

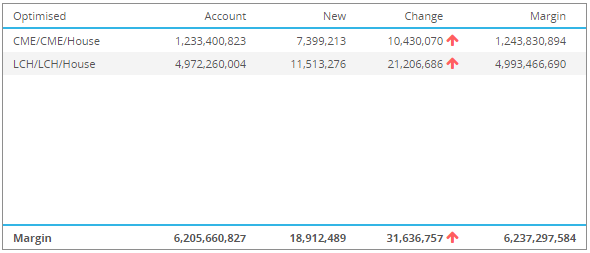

And when we update our margin obligations, we can see that they would increase at both CME and LCH if they trade with you and hedge at LCH:

Pro-Tip: Besides “Rates can only go up”, other viable reasons buy-side firms trade this swap include swapping out fixed rate coupons on bonds they hold.

Pro-Tip 2: Banks might not “unload” the swap at LCH like-for-like, but the hedging they do would ultimately represent a similar profile of risk at LCH.

Step 4.

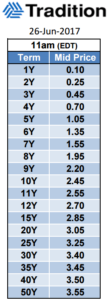

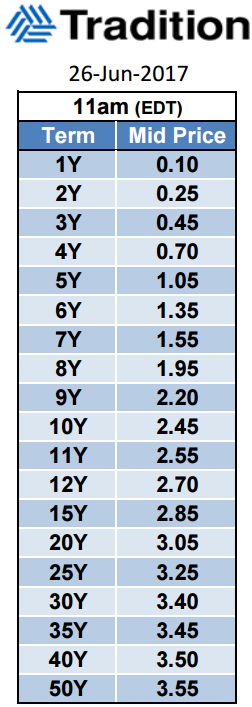

So you are saying, numbers go up, but the dealer is quoting you 3.4 basis points more at CME than LCH on your 30 year swap. Why is it 3.4 and not -3.4, or +34? (See the current Tradition quotes on the right).

The answer to our question of why it’s 3.4 and not 34, we need to look at what the margin numbers we saw cost in real terms.

So we run a process called MVA, or “margin valuation adjustment”. This requires us to compute what our initial margin will look like in the future, with and without these additional trades.

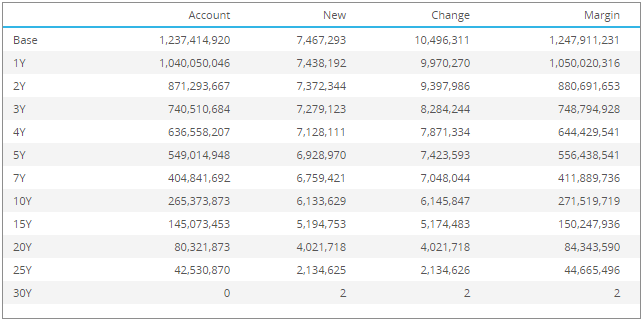

This screen below shows what our CME account with the added Fixed Rate receiver would look like:

Stepping through this:

- The First column is the forward point in time that we are computing our initial margin. Hence the “Base” row shows us our current day. And “1Y” is what our margin will be, if our portfolio only changed by decaying, in one year from today.

- “Account” shows us our Initial margin

- “New” is the initial margin of this trade at this future date, on a standalone basis, if only this trade existed in isolation

- “Change” is the increase (or decrease) in margin from adding this trade to the portfolio

- “Margin” is the new initial margin for the account at this future date.

So this screen tells us that we have to pony up $10m more in collateral today, and that amount of additional collateral will slowly taper off over the life of the trade (30 years).

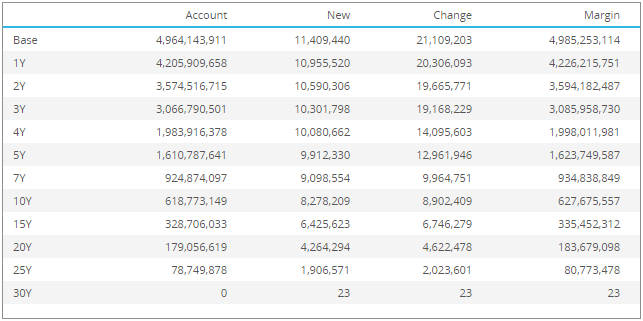

Of course we also want this same analysis for our LCH account which we’ve added a fixed-rate payer to:

This also shows an increase in margin.

Pro-Tip: A trade can increase the initial margin of an account by an amount MORE than the margin for the trade standalone. Reason being Clearing Houses begin to add on liquidity charges for large positions.

Step 5.

So ok, margins go up today. And I know how much they will go up for the next 30 years. The question remains why is the dealer charging me 3.4 basis points more at CME?

To answer this, we simply need to compute what this additional initial margin profile means to the swap dealer. So we compute the cost of this additional margin over time, given the banks own cost of funds. Just like valuing a loan of these amounts. Remember that the clearing houses might pay you some interest on the cash posted to them (eg Fed Funds), so the dealer assigns a funding spread, say 20 basis points above Fed Funds. This then yields a cost for funding this additional margin, in USD (or whatever ccy the CCP collects in):

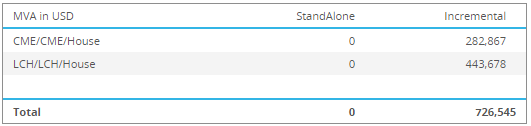

So it will actually cost the dealer $726,545 over the life of the swap to fund the margin requirements for this trade.

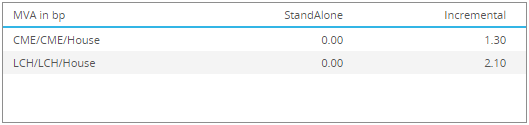

OK, so why 3.4 basis points? If we convert these numbers into basis point costs, based on the basis point risk of the trade (DV01) of $225,000, we get our answer:

This tells us that the CME swap equates to +1.3 bp and the LCH swap +2.1 bp.

And there you have it, 3.4 basis points.

Pro-Tip Conclusion

Pro-Tip Conclusion

This is a fairly simple example, and I had the luxury of crafting my own portfolio and my own funding rates to arrive at an answer that gave me a good answer. However, every bank is different and will have wildly different portfolios, and hence wildly different actual costs at CME and LCH. Hence many banks have an “axe” when it comes to swapping CME and LCH swaps.

But don’t forget that the basis market is a market unto itself, complete with speculation and panic, so it can move regardless of these costs amongst firms. But hopefully this provides some insight into how the basis arose, and what the basis represents.