Almost a year has passed since we last looked in detail at CCP Basis, which just goes to show how normal and accepted this has become in the market. Since the shock emergence of the CME-LCH Basis Spread in June 2014, we have seen regular trading of CME-LCH Switch trades to manage the CCP Basis risk and the emergence of an LCH-JSCC Basis in JPY Swaps and an LCH-Eurex one in EUR IRS.

In this article I will look at recent data for the major swap currencies, USD, EUR, JPY and AUD.

Background

For instruments that are economically the same, (if I am paying Libor 3M every quarter, I expect to receive the same stream of fixed cash-flows) it is non-intuitive that the fixed rate (price) should be different depending on which CCP clears the trade.

We have covered the reasons for the price difference in a number of blogs (see here and here). In summary these boil down to an asymmetry between payers and receivers at a CCP, requiring dealers to hedge at a different CCP and paying two lots of gross margin; the cost of which they need to recover in the price.

USD Swaps and CME-LCH

Lets start with the largest currency and the one we have the most transparency for.

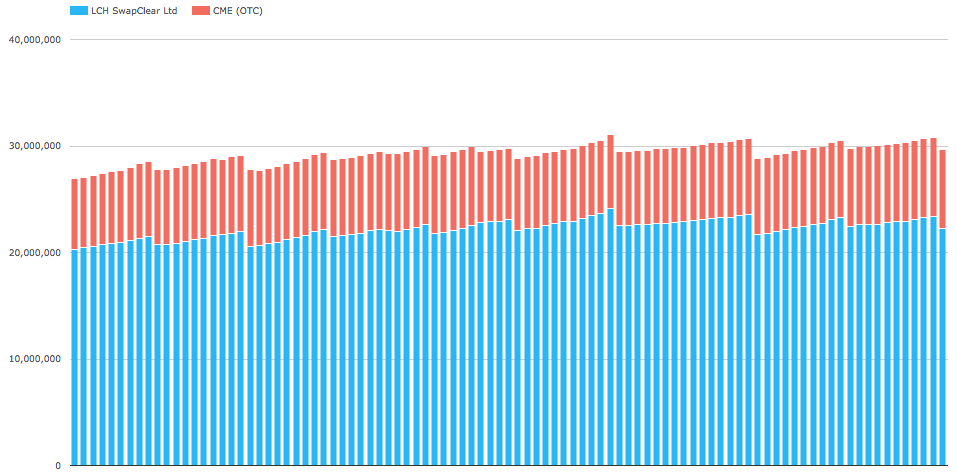

First USD Swap outstanding notional YTD at CME and LCH.

- LCH SwapClear starting the year at $20.3 trillion and now $22.3 trillion

- CME starting the year at $6.6 trillion and now $7.4 trillion

- A consistent market share of 75% to LCH and 25% to CME

- (The regular pattern of pronounced drops are from TriOptima/CCP compression runs)

So massive amounts of USD Swaps are cleared at each of these CCPs.

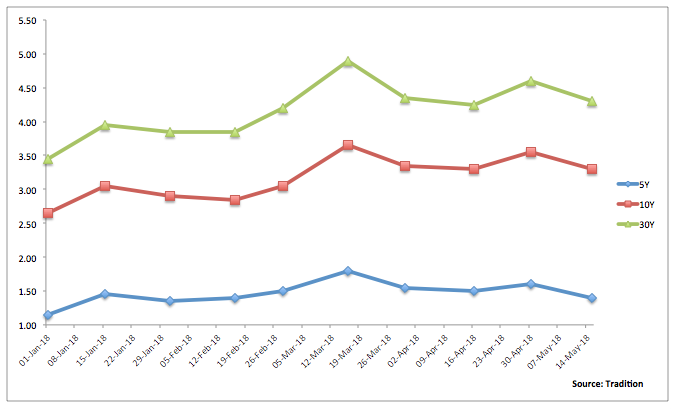

Next lets look at the YTD CME-LCH Basis price history.

- Each of 5Y, 10Y, 30Y showing a similar pattern year to date

- 5Y starting the year at 1.15bps, reaching 1.80bps in mid March and now 1.40bps

- 10Y starting at 2.65bps, up to 3.65bps and now 3.30bps

- 30Y starting at 3.45bps, up to 4.90bps and now 4.30bps

- Certainly not a static spread and one that needs to be managed

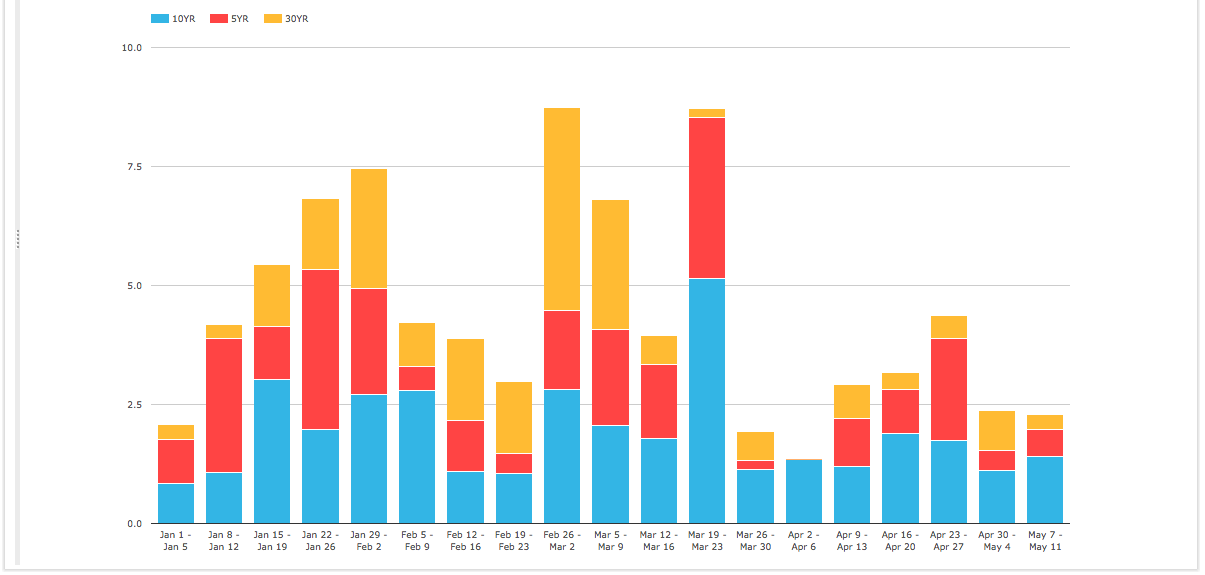

And next the volume of Switch trades that we see to manage this CCP Basis risk.

(These are trades where parties agree to simultaneously receive fixed at one CCP and pay fixed at the other).

- Showing only the 5Y, 10Y and 30Y tenor trades

- The largest week with $9 million DV01

- 10Y the largest YTD and in most weeks

- In other weeks 5Y or 30Y the largest tenor

So certainly active trading each week in significant size to manage risk or take advantage of the CCP Basis.

Thats it for USD.

EUR Swaps at LCH, Eurex and CME

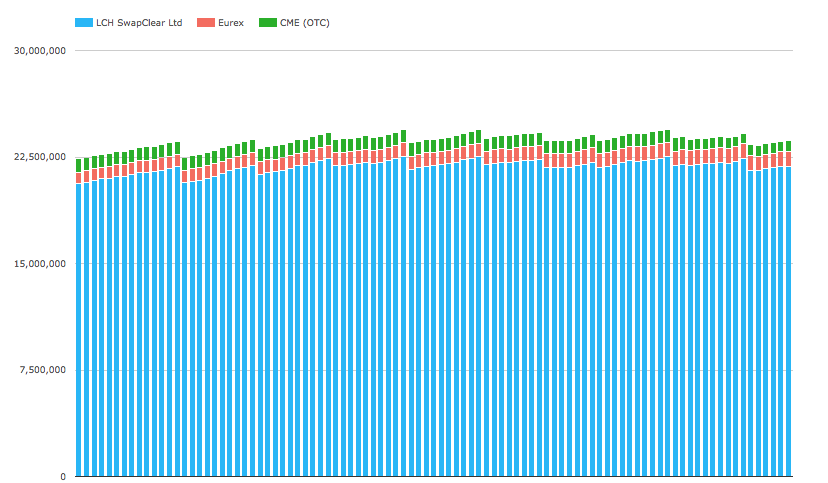

Next EUR Swap outstanding notional YTD at CME, Eurex and LCH.

- LCH SwapClear starting the year at €20.6 trillion and now €21.8 trillion

- Eurex starting the year at €800 billion and now €1 trillion

- CME starting the year at €900 billion and now €760 billion

- So recent market share is LCH 92.4%, Eurex 4.4% and CME 3.2%

- (The regular pattern of pronounced drops are from compression runs)

Compared to USD, which was 75% to 25%, we have a much higher concentration in EUR outstanding notional.

What does this mean for the existence of a CCP Basis in EUR?

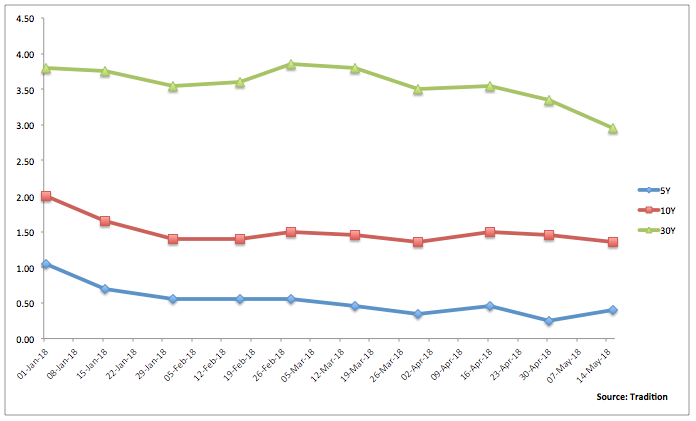

Lets look at the YTD LCH-Eurex Basis price history.

- Similar in magnitude spreads to those we see in USD

- 5Y, 10Y, 30Y showing a gradual YTD narrowing of the spread

- 5Y starting the year at 1.05bps and now 0.40bps

- 10Y starting at 2bps and now 1.35bps

- 30Y starting at 3.80bps and now 2.95bps

- Again by no means a static spread

The EUR LCH-CME Basis by contrast is static having been at -0.3bps, -0.4bps and -0.85bps for 5Y, 10Y, 30Y for most of the year, only recently 30Y narrowing to -0.3bps.

Next it would be good to see the volume of CCP Switch trades and MiFiD II transparency certainly promised such data, but those of you that follow our MiFID blogs will know that it is a challenge to even answer simple questions like how much EUR IRS 10Y trades on a given day, let alone more nuanced ones like how many EUR IRS 10Y LCH vs Eurex Switch trades.

I remain in hope that in the near future we will be able to answer such questions.

JPY Swaps at LCH, JSCC and CME

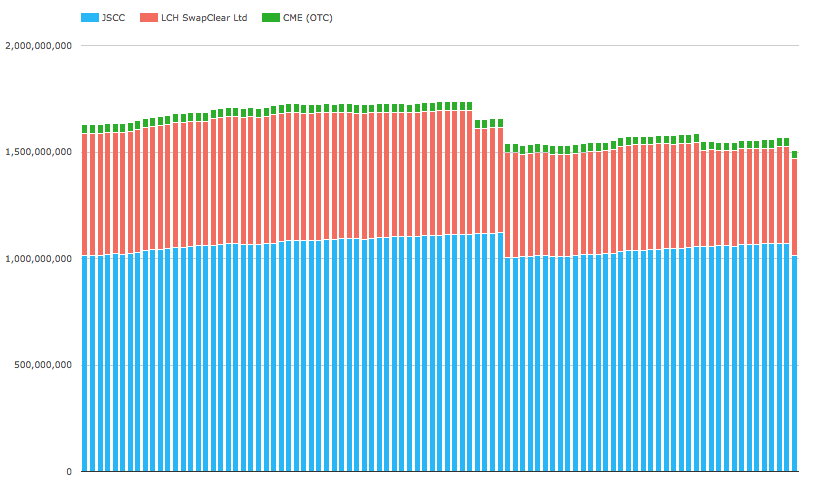

Next JPY Swap outstanding notional YTD at CME, JSCC, LCH.

- JSCC starting the year with Yen 1,015 trillion and the same now

- LCH SwapClear starting the year at Yen 570 trillion and now Yen 455 trillion

- CME starting the year at Yen 42 trillion and now Yen 40 trillion

- Recent market share is JSCC 68.5%, LCH 29% and CME 2.5%

- (The regular pattern of pronounced drops are from compression runs)

So not too dissimilar to the split we saw in USD, but this time LCH the smaller party.

I was going to look next at the LCH-JSCC Basis price history, however unfortunately I have run out of time to do so before deadline to complete this article.

So you will have to trust me when I say that it is volatile in a similar manner to USD and refer to earlier blogs where I cover this, see LCH-JSCC Basis: An Update.

As for CCP Switch trades, unfortunately the transparency in the Japanese market from Trade Repositories or ETPs does not provide such granular insight.

Now the question I want to end with is: does it follow that whenever there is significant volume at more than one CCP, there is always a basis (price difference) between the same product cleared at each CCP?

AUD Swaps at ASX and LCH

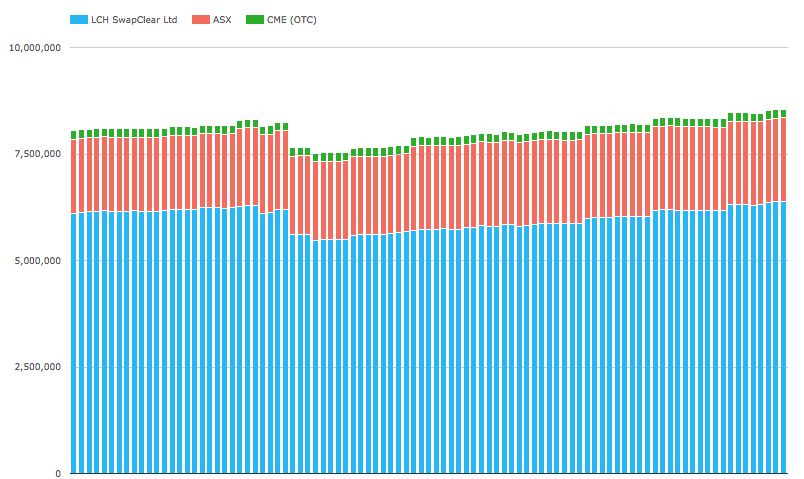

Lets turn to AUD Swaps outstanding notional YTD at ASX, CME and LCH.

- LCH SwapClear starting the year at AUD 6.1 trillion and now AUD 6.4 trillion

- ASX starting the year at AUD 1.7 trillion and now AUD 2 trillion

- CME starting the year at AUD 200 billion and now similar

- So recent market share is LCH 74.5%, ASX 23.2% and CME 2.3%

Not too dissimilar to the split we saw in USD.

Final Thoughts

So we should expect an LCH-ASX Basis in AUD Swaps.

However there does not appear to be one. Why?

I can only assume because some of the requisite conditions for a CCP Basis are not present.

The liquidity pool at ASX, while smaller, must have evenly matched supply and demand from payers and receivers and the maturities cleared shorter in tenor, so dealers do not have to turn to LCH to balance their positions.

So while dealers have become wary of a CCP Basis emerging, it need not exist.

And if it does emerge, the market will trade it to manage risk.

It will be interesting to keep an eye on Swap markets in 2018 and 2019.

As regulations and political events unfold.