- ESTER will be the European Risk Free Rate (RFR), following an announcement from the European working group.

- This means that ESTER will replace EONIA (and EURIBOR) as the most important interest rate in Europe.

- Pre-ESTER data is now available, including volumes.

- The race starts now to be the first to trade ESTER swaps!

What You Need to Know about ESTER

We covered ESTER’s background in-depth during our previous blog, including the indices that ESTER beat in the race to be chosen as the Risk Free Rate (RFR) for Europe. In summary;

- ESTER will be administered by the ECB.

- ESTER “stands for” Euro Short Term Rate.

- It is based on transaction data collected as part of the daily money market statistical reporting from the 52 largest euro area banks.

- Average daily volume of included transactions has been around €30bn.

- Average spread to EONIA has been around 9 basis points (ESTER below EONIA).

- EONIA’s typical “heartbeat”, where it spikes at regular Maintenance Period start dates due to reserve requirement front-loading, is not so apparent in ESTER.

- The ESTER website is here.

- ESTER will start publishing before October 2019.

Why is ESTER Important?

Several reasons.

- EONIA (as it stands) will cease to meet “the criteria of the EU Benchmarks Regulation and will therefore see its use restricted as of 1 January 2020”. Hence ESTER will largely replace EONIA.

- EURIBOR will probably go the way of LIBOR with its’ existence beyond 2020 questionable. The chosen RFR in Europe, now defined as ESTER, will (probably) form the base for LIBOR fallbacks.

- EONIA is one of the most successful OIS markets around the globe. It is the only OIS market that sees significant outright volumes trade beyond two years. Transition from EONIA to ESTER must at the very least preserve this market structure – and hopefully see liquidity shift from EURIBOR swaps to ESTER swaps.

Decision Time

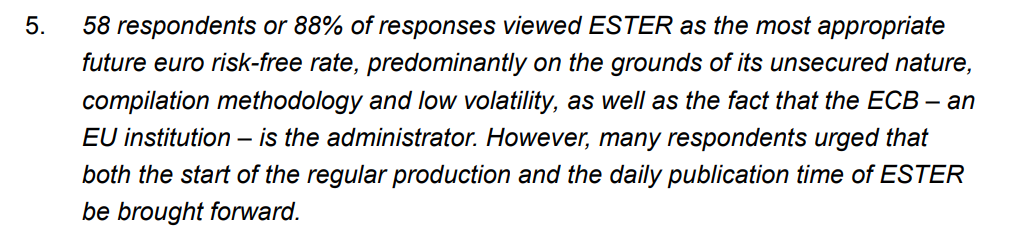

Back in August, the public consultation on European RFRs (see our blog here) had found that 88% of respondents agreed that ESTER was the best replacement available for EONIA. That is convincing support for the new rate!

The three main points that respondents highlighted were:

- It is an unsecured rate – so as similar to EONIA as possible.

- Compilation methodology – note this doesn’t explicitly reference the volumes underlying the rate (which are lower than a secured rate) but it is transparent and easy to understand (no complex filtering of “specials” or by clearer).

- ECB is the administrator. So Central Banks are becoming the de-facto provider of rates. The RBA (AONIA), BoE (SONIA), BoJ (TONAR), Fed (SOFR, Fed Funds) and now the ECB (ESTER). Switzerland stands out as having SIX be the administrator of SARON here!

It looks like only the US (SOFR) and Switzerland (SARON) are going ahead with secured rates as their chosen RFRs.

ESTER History

Now that ESTER has been chosen as the preferred RFR, the ECB has also released “pre-ESTER” rates. These are rates using the same data as ESTER will use. (Although please note that cancelled trades are removed from pre-ESTER even if cancelled after 9am the following day. I can’t imagine this makes much difference?).

The rates are available from the ECB Statistical Warehouse.

So, onto the data….

ESTER Rates

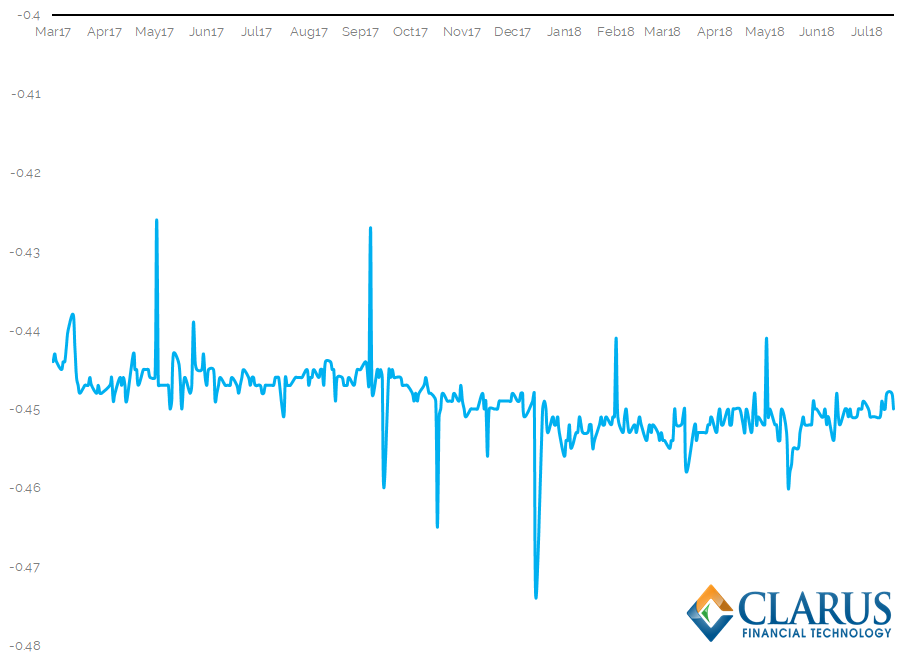

The so-called “pre-ESTER” data is available back to March 2017:

Armed with the data, the chart shows:

- ESTER appears somewhat more volatile than when we first presented the charts from the original consultation. But please bear in mind, the rate has still only moved in a six basis point range in the past 18 months. I don’t think this can really be described as “volatile”!

- There is some evidence of a “turn” at the end of the year, with the rate on 29th December 2017 three basis points lower than surrounding dates.

- Otherwise, it doesn’t show the distinct “heart-beat” of EONIA around ECB maintenance periods. But that effect in EONIA has really waned in the QE era anyway, so there’s nothing to say it won’t develop in ESTER as QE is unwound.

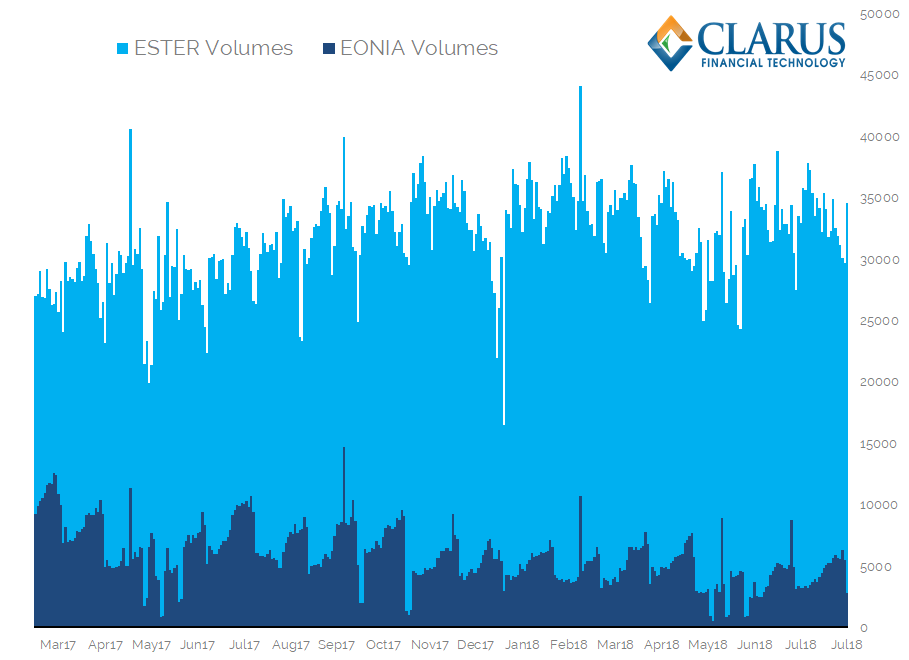

ESTER Volumes relative to EONIA

How do ESTER volumes compare to EONIA?

This is covering a little bit of old ground, but it is worth stressing.

The chart shows that;

- ESTER volumes are significantly (and consistently) much higher than EONIA.

- The daily average volume in ESTER is €26bn higher than EONIA.

- The relative difference between ESTER and EONIA volumes seems to be increasing. It averaged €29.3bn during July 2018.

- I can just about recognise the “heartbeat” of EONIA volumes in this chart. They are clearly lower at the start of a maintenance period as reserves are front-loaded. That pattern is more difficult to see in the ESTER data – i.e. I’m not sure it happens.

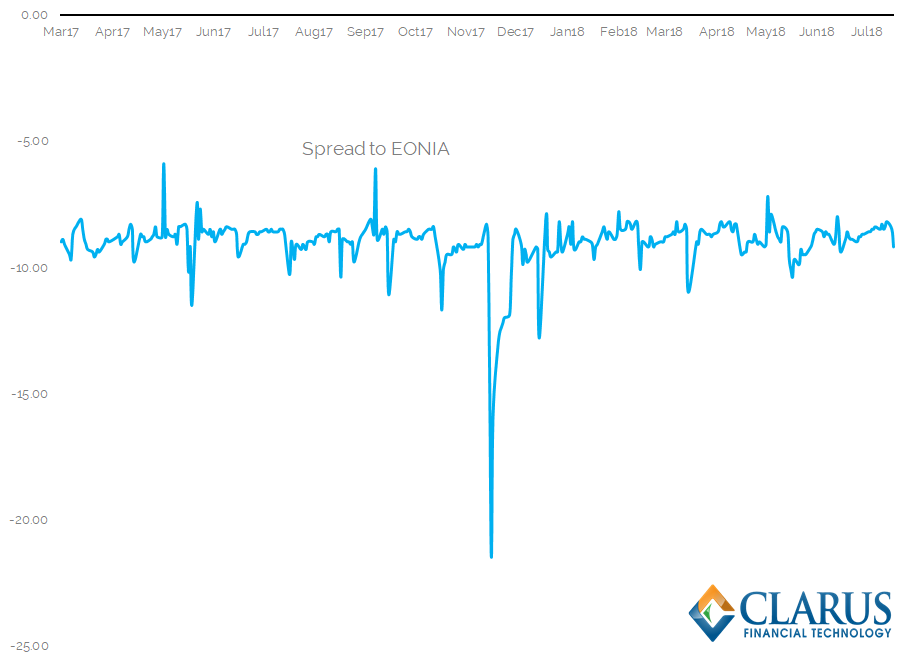

ESTER spread to EONIA

The transition to ESTER trading will be interesting. The starting point will be to look at the history of the rate relative to EONIA.

In the US, current basis spreads between Fed Funds and SOFR are razor-thin – the basis trading around 1 basis point last time that I looked. Will the spread between ESTER and EONIA be so tight?

Showing;

- ESTER is consistently below EONIA, to the tune of around 9 basis points.

- This spread has ranged from -5.9 basis points to -21.5 basis points.

- I remember when we first looked at SOFR, we also saw a consistently negative spread (SOFR below Fed Funds).

- That wasn’t a structural thing with SOFR however – we have since seen SOFR fixing above Fed Funds. The one year basis, for example, has been trading around one basis point.

- There might be a structural reason for ESTER to always be below EONIA – with a wider array of transactions being captured, particularly outside of the banking sector.

Who will be first?

Now we’ve got a defined RFR in Europe, who will be first to:

- Trade a bilateral ESTER swap?

- Clear an ESTER swap at a CCP?

- Trade a cross currency swap ESTER vs SOFR?

The race is on…..will it be the same players who traded the first SOFR swaps?

Admittedly, we will have to wait for the ECB to start publishing ESTER. This is stated “by October 2019.” It would be nice to see that date come forward, to “as soon as possible”.

In Summary

- ESTER will be the RFR for Europe.

- ESTER is administered by the ECB and published daily.

- It is based on around €30bn worth of unsecured money market transactions each day.

- Trading will now start to transition away from EONIA (and EURIBOR) to ESTER products.