- We have now had six SOFR swap trades hit the SDRs.

- Both Basis vs Fed Funds and Outright OIS has traded.

- All trades have been $50m and one year maturity.

- It looks like they were all cleared at LCH.

- The first swap was done on the TP-ICAP SEF.

SOFR

Everything you need to know about SOFR can be found here. Or rather, it was until this happened yesterday:

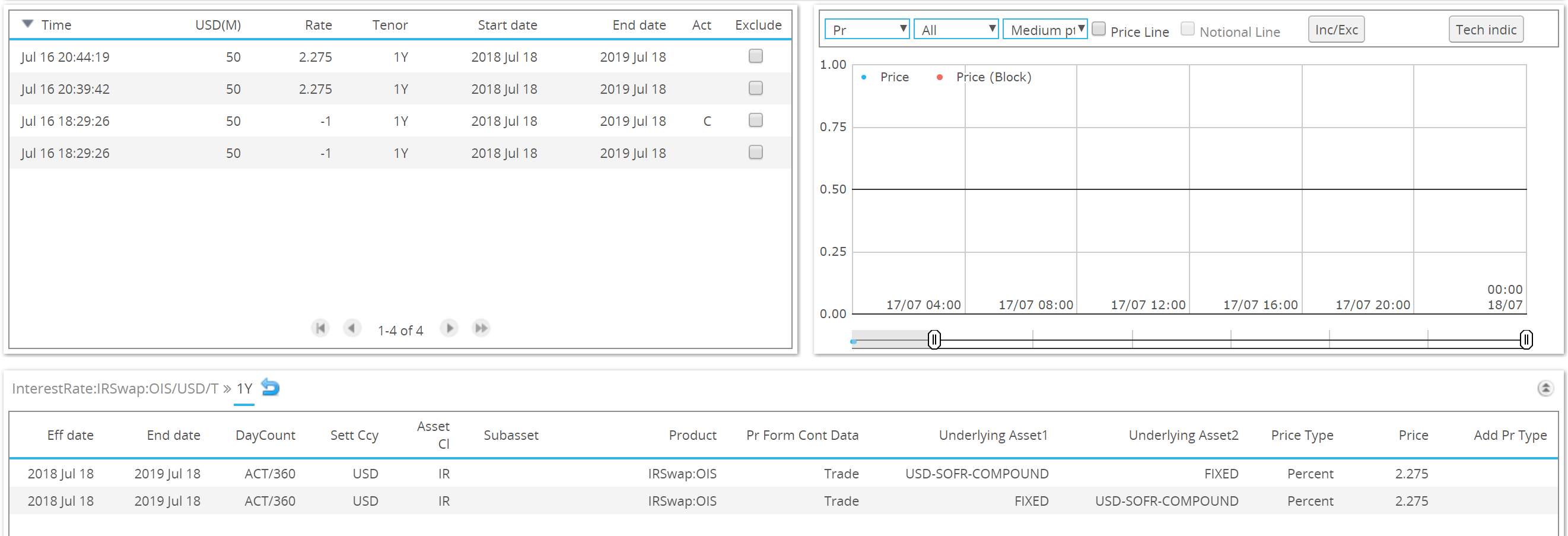

July 16th 2018 18:29 CET

Look at that – July 16th, 18:29 CET we see the first ever SOFR outright OIS trade hit the SDR. It was a one year trade, out of spot and was in a huge $50m notional!

Look at that – July 16th, 18:29 CET we see the first ever SOFR outright OIS trade hit the SDR. It was a one year trade, out of spot and was in a huge $50m notional!

It was traded at a rate of….oh, -1 basis point. Uh-oh, looks like something went wrong. As you can see in the top left panel above, it was immediately canceled.

July 16th 2018 18:57 CET

But wait! It’s back….it looks like some 28 minutes of discussing whether it was transacted as an outright or basis resulted in the same trade being reported as a basis swap versus Fed Funds. I’m sure this is just typical teething problems with these new swaps:

Finally we have the anatomy of the first SOFR trade laid bare.

- It looks like it traded at SOFR -1 basis point vs Fed Funds flat.

- 1 year tenor

- Spot starting

- $50m

- USD SOFR daily compounded.

- USD Fed Funds daily compounded.

- 3m vs 3m coupons, both legs ACT/360 day count. Gary will be updating his OIS Nuances blog shortly…

- It was Cleared! – that’s a coup for the CCP involved – see below.

- Transacted ON SEF! – a coup for the SEF involved, which we later learnt was TP-ICAP.

- Reported to DTCC – a coup for the SDR to be ready in time.

- We also just heard that these were all done via MarkitWire – impressive again for all these infrastructure providers to be ready.

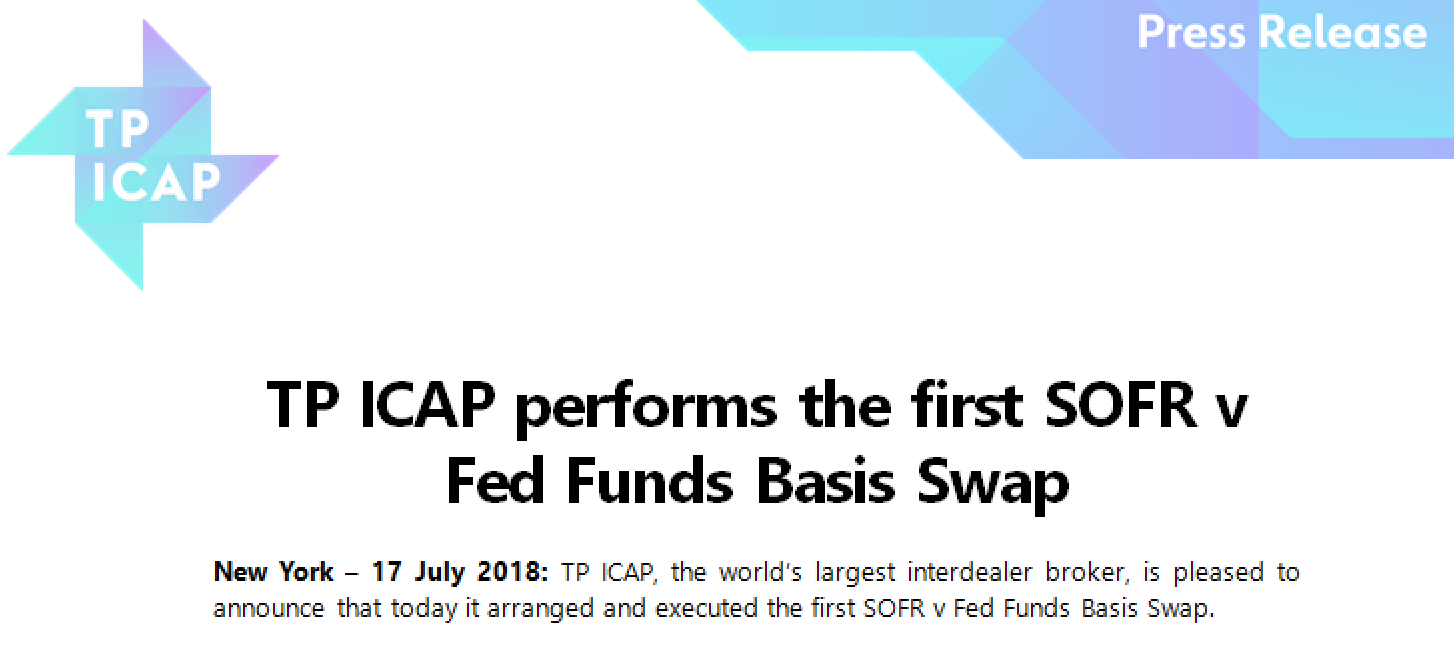

TP-ICAP have also given us a press release about this now. Very impressive work to have got the first trade done on-SEF!

July 16th 2018 20:39 and 20:44 CET

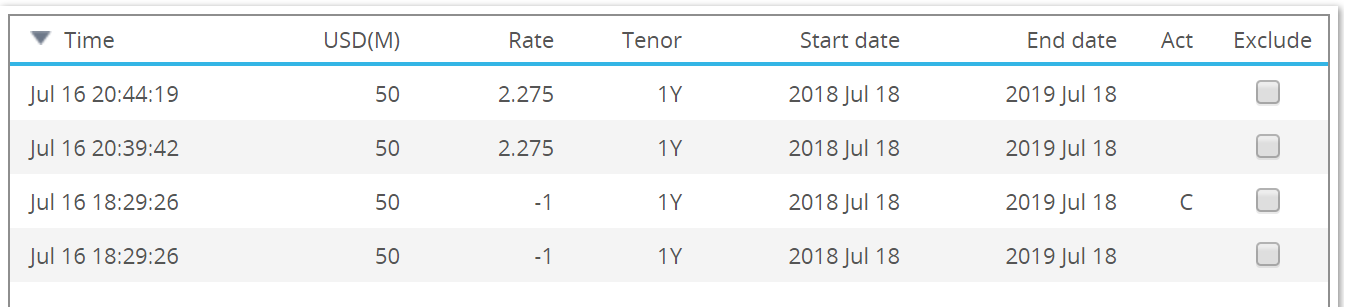

However, instead of waiting for the press releases, you could have been watching the SDR data and seen that the outrights were very quick to get in on the action! 1 year went on to trade in $50m clips TWICE at 2.275%:

- Fixed rate of 2.275%

- 1 year tenor

- Spot starting

- Each in $50m

- USD SOFR daily compounded to a zero coupon frequency.

- Zero Coupon fixed rate on an ACT/360 day count.

- It was Cleared!

- It was transacted off-SEF.

July 16th 2018 20:57 CET

Hold on….there’s more. You wait three months for a trade, and typical, they all come along at the same time! This time, it’s different:

- SOFR -1 vs FF flat (again).

- 1 year tenor

- Spot starting

- $50m

- USD SOFR daily compounded

- USD Fed Funds daily compounded (all of this is consistent with the first trade)

- But this swap traded 1y vs 1y (or zero coupon vs zero coupon) on an ACT/360 day count.

- This was again Cleared.

- This was transacted Off-SEF. Maybe SEFs are so far only listing 3m vs 3m structures? If you are trading bilaterally, you might want to minimise settlement risks with 3m coupons, but if the swap is cleared there shouldn’t be too many concerns whether these swaps are going to see 3m or 1y payments (as it is directly netted versus daily VM at the CCP).

July 16th 2018 21:04 CET

And the activity continues!

- SOFR basis at -1 vs FF flat (yup, again).

- 1y, spot starting, $50m, traded off-SEF and again traded 1y vs 1y.

Phew, we need a breather….

July 17th 2018 14:15 CET

With the market digesting that overnight, we had to wait again until the New York morning for another trade. This time, it was again 1y basis, again at -1 basis points, again it was Cleared and this time it was traded on-SEF.

It’s great news that both SEFs and CCPs are involved on day one for a new product – proving that innovation is alive and kicking.

In summary, our basis “tape” looks like this:

Which CCP Cleared the trades?

You may have seen Pimco’s remarks today re: SOFR and discounting. That gave me a hint as to where these swaps were cleared.

As per conventions from cross currency (and single currency basis), we tend to put the spread on the leg that is the “basis” to the discounted leg (e.g. xccy has the spread on the non-USD leg, and is discounted into USD). Given these swaps had the spread on the SOFR leg, I had a hunch therefore that these were cleared at LCH (and hence discounted into Fed Funds).

And from what I can see on the website, SOFR clearing is now live at LCH, for both basis vs Fed Funds and outright OIS:

The CME website, on the other hand, states that clearing will commence in Q3 2018. So it looks like LCH were involved on these first swaps. Which means at the moment they have been discounted into Fed Funds.

The CME website, on the other hand, states that clearing will commence in Q3 2018. So it looks like LCH were involved on these first swaps. Which means at the moment they have been discounted into Fed Funds.

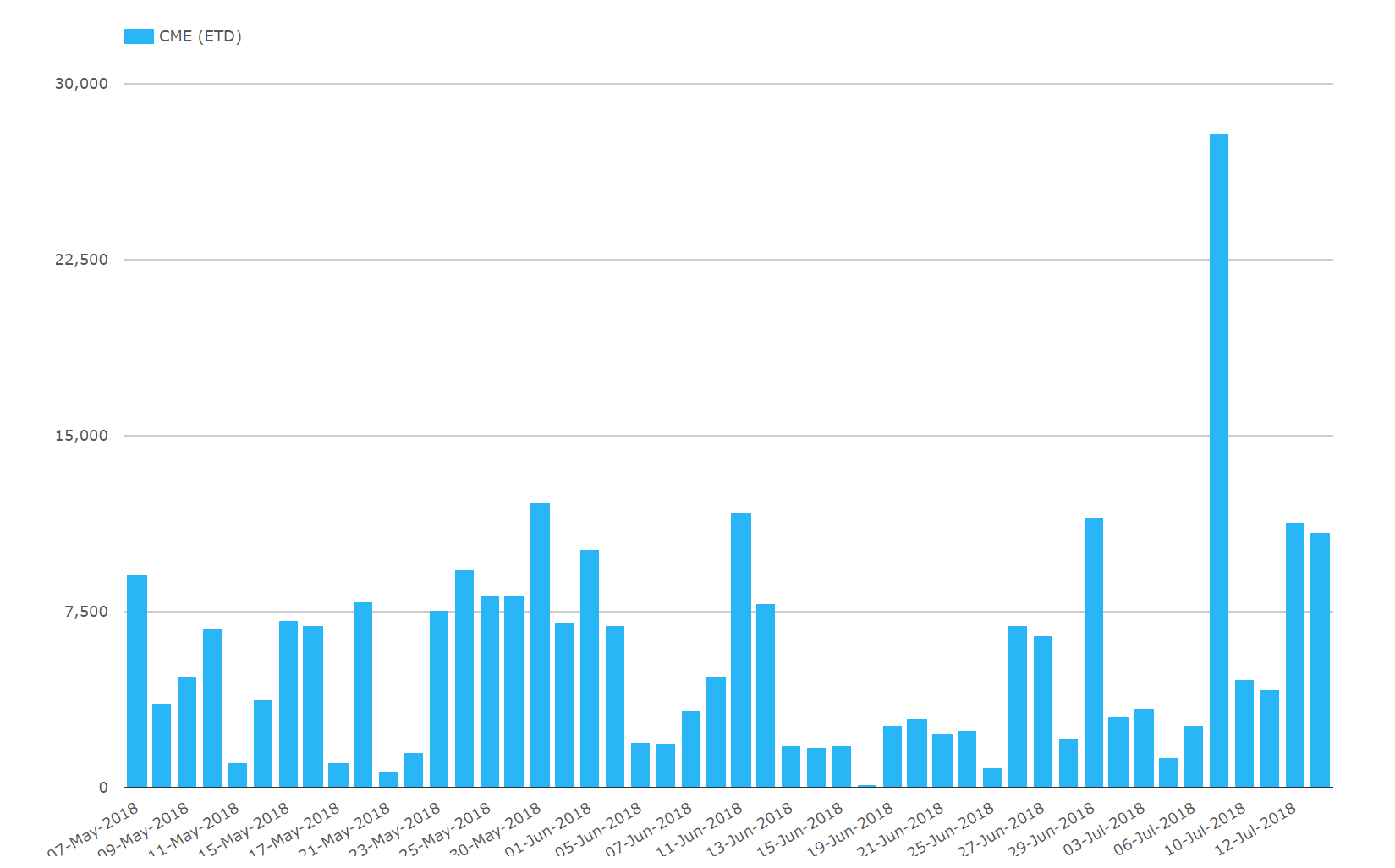

Of course, CME on the other hand have a very successful futures franchise to consider, and we’ve already seen much larger positions traded in futures. Look at the SOFR futures volumes from CCPView:

Even on a slow day, the SOFR futures are trading in over $2bn notional equivalent. Okay, it’s a shorter maturity (1 month or 3 month), but still it shows that OTC is playing catch up to futures right now.

Even on a slow day, the SOFR futures are trading in over $2bn notional equivalent. Okay, it’s a shorter maturity (1 month or 3 month), but still it shows that OTC is playing catch up to futures right now.

All swap trades have so far been $50m of 1 year risk, so let’s wait until this really starts trading in $1bn+ clips in the short-end before getting too excited. Eventually, maybe the action in this basis may be just as impressive as we have seen in Libor-OIS this year.

Final Update

July 19th 2018 15:57 CET

We have a very neat “Alerts” feature that sends all SOFR trades straight to my inbox. It’s the ideal way to stay on top of this new market:

Try it out for yourself via SDRView Pro (free trials available).

Try it out for yourself via SDRView Pro (free trials available).

In Summary

- SOFR vs Fed Funds basis has now started trading.

- We have only seen one year trades in small size to begin with.

- It’s great news that these new transactions were first transacted on a SEF.

- We believe that LCH cleared these swaps, and they will accept trades up to 51 years in tenor.

- Basis trading has some way to go to build up volumes and a term structure now!