Clarus will be talking about Libor reforms at the FoW Derivatives World event in London tomorrow, December 6th 2017. For more information on the event and to register, please check out the link below. It should be free to attend for most of our readers.

Libor Reform

Before we end 2017, I wanted to run through what has been going on with Libor reform since we last wrote about it in September. Whilst it’s tempting to think of this as “next year’s problem”, plenty has already happened.

We’ll split this into three areas today – monitoring SARON volumes, updating developments in Europe, and looking at Transition Plans.

SARON

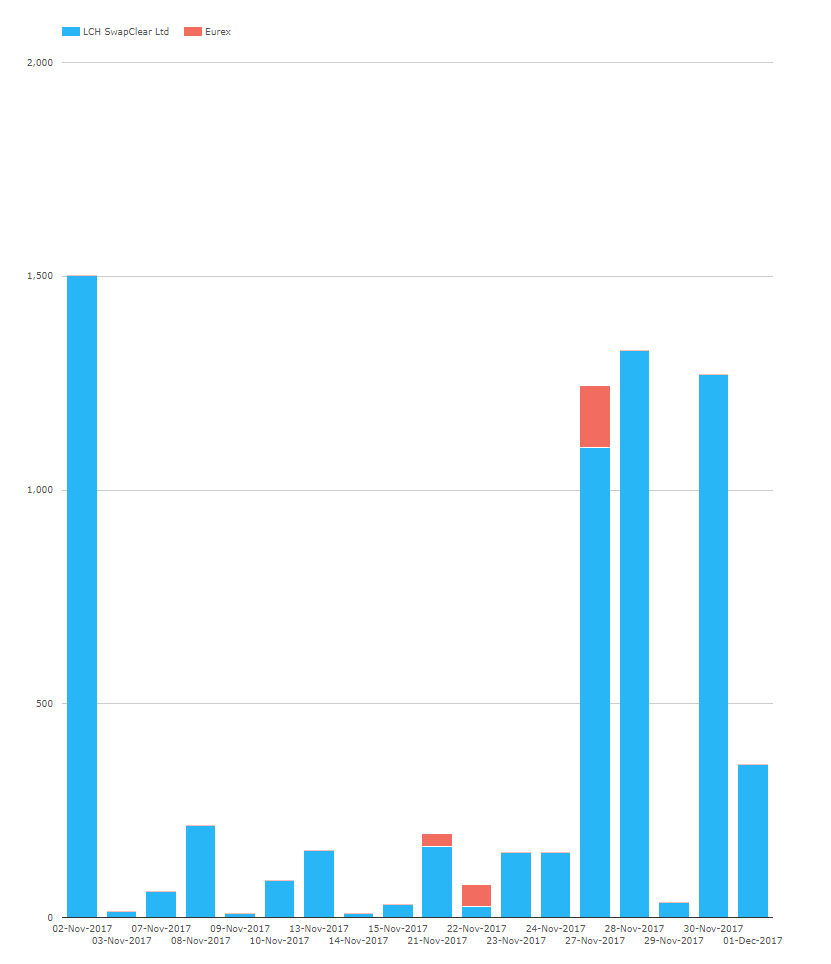

We continue to monitor volumes and Open Interest in CHF SARON swaps. For our background blogs, please see here and here. Last week saw relatively large volumes trading at LCH, with activity on three days at Eurex as well:

Showing;

- Much larger levels of activity since our previous update.

- We had three trading days last week with volumes over CHF1bn.

- SDRView Pro shows only one more trade (i.e. involving a US person) since our last update. It remains a European market – hardly surprising.

- Interesting to see some trading at Eurex. Remember that Eurex ceases accepting new trades versus TOIS as of December 4th. It is therefore very likely that these Eurex-cleared trades have also been versus SARON (see next chart).

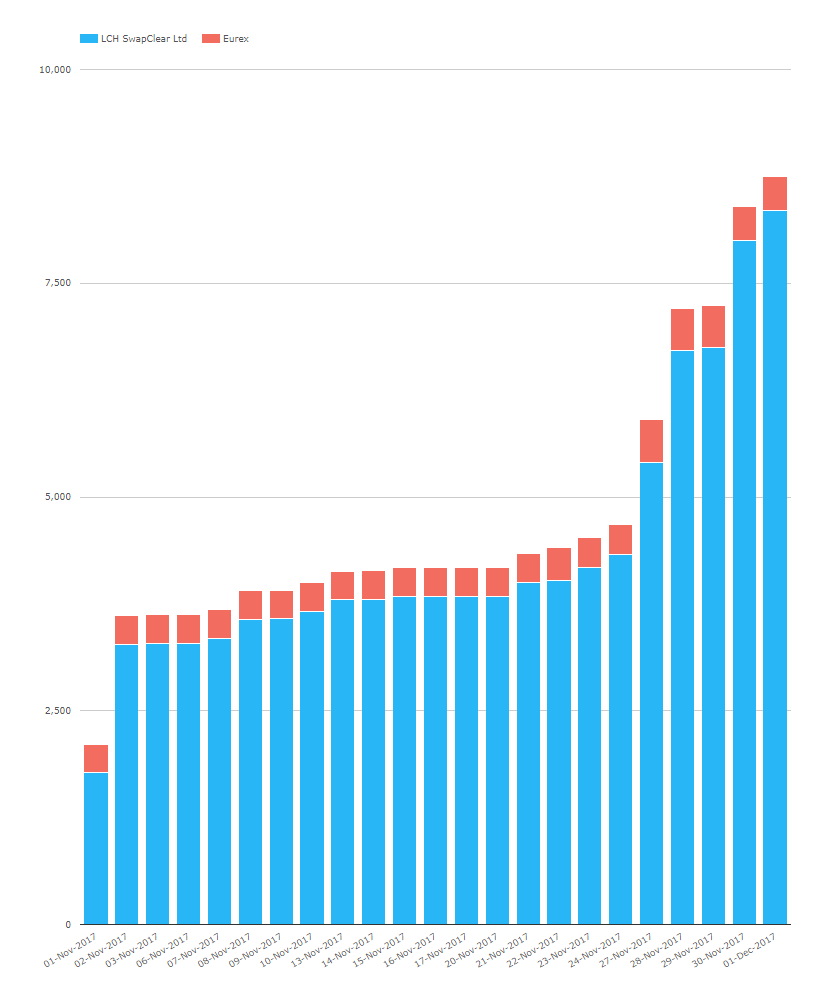

Let’s look at Open Interest changes at both Eurex and LCH:

Showing;

Showing;

- All new trading activity appears to be adding to Open Interest.

- Open Interest at LCH increased by CHF4bn last week – it basically doubled.

- Eurex Open Interest peaked at CHF495m, and has since shrunk to CHF405m. I assume this is some old TOIS contracts maturing.

- Recall that Eurex will cash-settle all outstanding TOIS contracts on 11th December (i.e. next week). Let’s see if they can repeat the LCH “trick” of ensuring there is no actual Open Interest remaining as of this cut-off date!

Is SARON teaching us anything about LIBOR?

CHF IRS is a small market. Aside from the fact that I used to trade Swissie (and now live here), why focus on SARON? Well, because it is the first market to see a transition to a “new” risk free rate. In particular;

- SARON has replaced TOIS as the discount rate at CCPs. TOIS was unsecured, SARON is a secured rate.

- There was no term SARON swaps market even three months ago. Trading did not start in earnest until CCPs (Eurex and LCH) made SARON swaps available for Clearing.

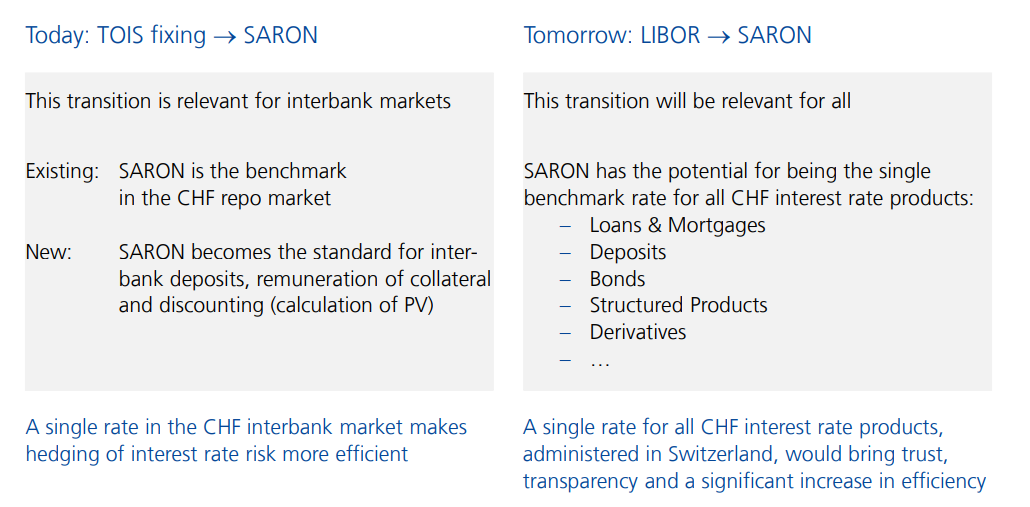

- The Swiss National Working Group on Reference Rates see the transition from TOIS to SARON as the first step in the replacement of LIBOR in CHF IRS trading:

It is rather obvious to state, but if SARON trading had failed to take-off at all then we’d be really worried about replacing LIBOR. So far, replacing TOIS is acting like a microcosm for what might happen when we come to replace LIBOR.

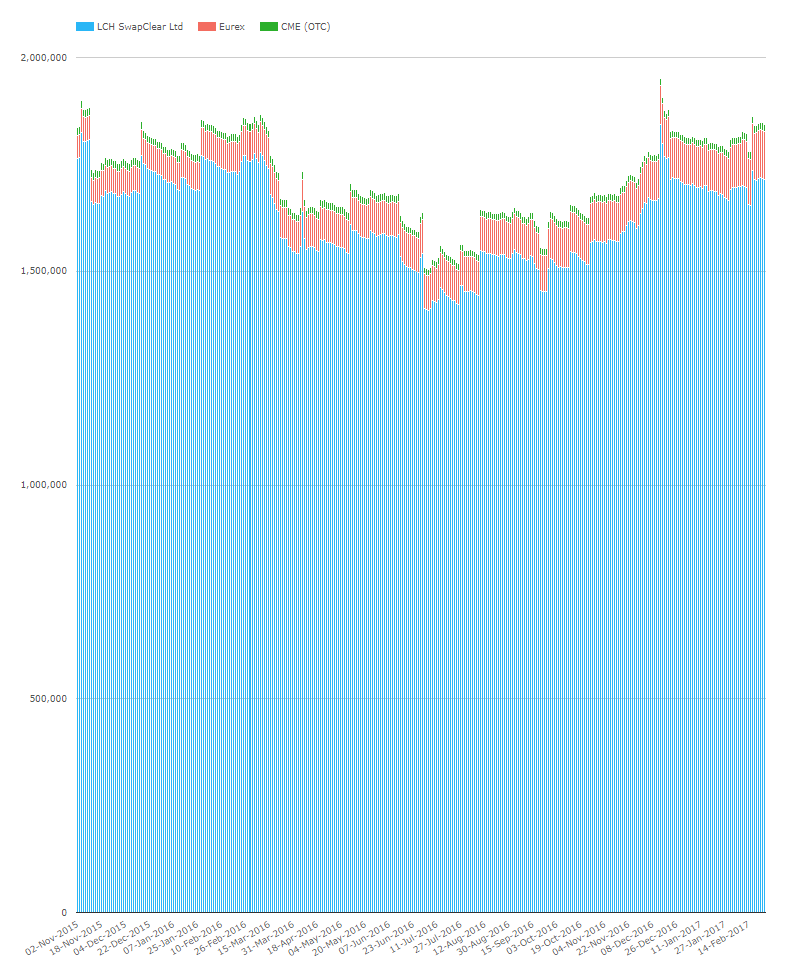

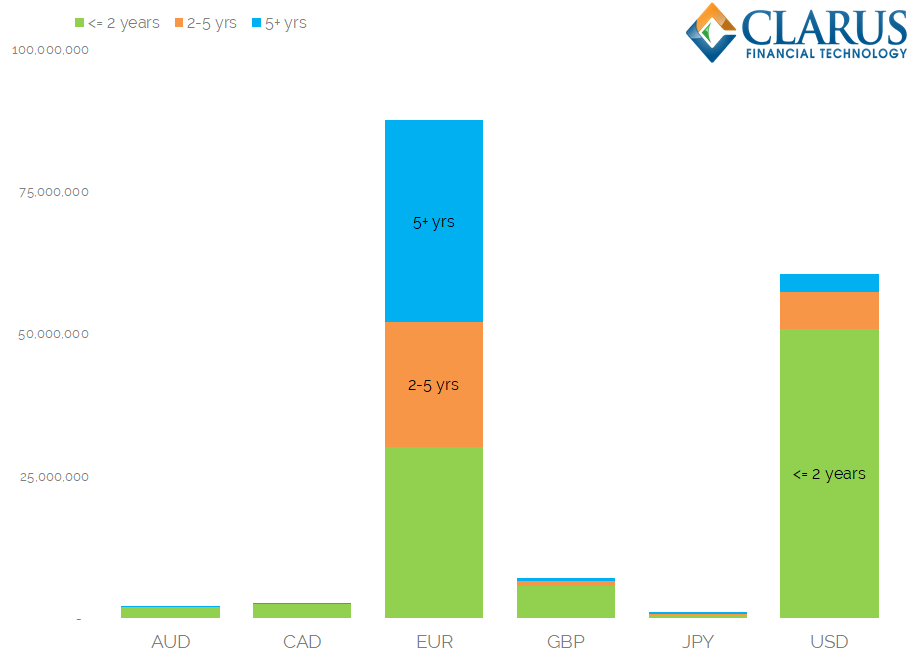

And remember that it IS a microcosm. Open Interest in LIBOR-based CHF swaps is currently 200 times greater than SARON swaps. I can’t imagine these swaps naturally running off to zero by 2021….just look at the current Open Interest in Libor-based CHF swaps below:

In fact, looking at the development of Open Interest in CHF Libor swaps makes us wonder why Compression isn’t being more effective in that market? One thought I have is that compressing to standardised dates on the existing LIBOR curve offers a simpler transition away from Libor in the future:

In fact, looking at the development of Open Interest in CHF Libor swaps makes us wonder why Compression isn’t being more effective in that market? One thought I have is that compressing to standardised dates on the existing LIBOR curve offers a simpler transition away from Libor in the future:

- Valuation and risk differences of long-term contracts can be realised on the known Libor curve into standardised dates (e.g. IMMs).

- Fewer outstanding contracts to transition.

- Less valuation uncertainty at the point of transition.

- Lower notional, lower gross risk, virtually identical net risk.

- Fewer valuation differences between fewer counterparties.

Transition plans should start earlier rather than later. Which brings us on to Europe…

Europe

Whilst Switzerland is leading the charge in new rates, the United Kingdom is leading the charge in reform of existing rates with SONIA. But the rest of Europe was somewhat behind. It wasn’t until September that the ECB announced work on a new risk free rate – the announcement that spurred me on to this series of blogs. As of last week, we also now have more information on the Working Group that will steer this process:

It sounds similar to the Working Group for SONIA. It will initially be driven by the banks who are active in the market and have direct exposures to the existing risk free rates. Makes sense.

It sounds similar to the Working Group for SONIA. It will initially be driven by the banks who are active in the market and have direct exposures to the existing risk free rates. Makes sense.- The ECB also states that

Its terms of reference are publicly available and the group will regularly report on its meetings. This is to ensure transparency throughout the entire process of identifying and adopting new risk-free rates.

- We strongly support this drive for transparency. For example, we think that trade-level transaction reporting versus new Risk Free Rates should be considered a beneficial feature of the new markets. This in-built transparency should be used in a positive manner to encourage the uptake of new risk free rates. Otherwise, it would be all too easy for a small group of market makers to try to create a new, opaque market where they are able to monetise information asymmetries.

- The Working Group will have a particularly interesting market dynamic to balance. EONIA is the only OIS rate traded with substantial activity beyond two years – thanks to a healthy invoice spread market versus Eurex-traded futures (Schatz, Bobl and Bund contracts). We need to maintain, support and foster this level of activity in long-dated OIS trading, even as the EONIA fixing itself is reformed.

Transition Planning

CHF markets are already in the midst of the transition. The next step is to start moving away from old Libor contracts. With this in mind, I note that ISDA have recently announced their intention for a Roadmap. Maybe I’m being overly analytical, but I note that nowhere do they mention a “protocol”. From ISDA:

Maybe such a fundamental change to contracts such as reference indices cannot be catered for by a protocol? The most famous protocol (that I know of), was the CDS Big Bang in 2009. Refreshing my memory, I note that this “hardwires” an auction mechanism following a credit event. Maybe the industry plans to explore some enforced participation into a series of auctions for Libor contracts?

Maybe such a fundamental change to contracts such as reference indices cannot be catered for by a protocol? The most famous protocol (that I know of), was the CDS Big Bang in 2009. Refreshing my memory, I note that this “hardwires” an auction mechanism following a credit event. Maybe the industry plans to explore some enforced participation into a series of auctions for Libor contracts?

The only concrete transition plan that I have seen laid out so far is from Darrell Duffie at Stanford. As part of the SIX conference, he suggested an auction methodology. His full presentation is well worth watching.

In Summary

If any of this has piqued your interest, Clarus will be talking about Libor Reform at the FoW Derivatives World event in London tomorrow. Anyone interested to learn more can register below. I’m up at Midday, assuming my flight is on time…..