- We look at the consultation for forward-looking term rates in ESTER.

- The number of cleared EONIA swaps is surprisingly low, suggesting a transaction-based methodology will be ruled out.

- A quote-based system is most likely, but this could replicate existing problems we have with EURIBOR.

- We note that CCP basis also makes the collation of quotes potentially more difficult.

Risk Free Rates in Europe

2018 ended with a new public consultation on RFRs in Europe. Launched on the 20th December (just what we wanted before our Christmas break!):

Which ESTER-based methodology would be best suited for producing a fallback rate for EURIBOR-linked contracts? Share your views with the working group on euro risk-free rates by 1 February https://t.co/kA5f6Zl5kt pic.twitter.com/2eUykaIuaA

— European Central Bank (@ecb) January 8, 2019

It covers:

- The need for a term rate in Europe if EURIBOR disappears.

- Specifically, the need for a forward-looking term rate in markets outside of OTC derivatives.

- Methodologies that could be used across transactions, quotes and futures markets to derive these term rates.

I fully admit that I rolled my eyes at the thought of another consultation on RFRs, having recently responded to the SONIA and ISDA ones. And of course keeping ourselves informed on what is happening at the ARRC. However, I’m glad I took the time to read this one, as there are some interesting facets of the European transition.

The tone of the consultation is also very much in line with John’s recent blog on Non-Dealer Users of RFRs: The need for term rates, along with what we aim to achieve with CLARUS01.

Europe

I have particular sympathies for the European market in respect of the transition to RFRs:

-

OIS activity by currency and tenor. EUR markets are the only OIS market that see substantial activity longer than 2 years. The EONIA OIS market is already large, and is the most widely traded long-dated OIS market out there. Much of the duration being traded is thanks to invoice spreads traded versus Eurex bund contracts in the interbank market. We are still waiting for GBP and USD OIS markets to embrace similar long-dated OIS trading.

- Despite this, EONIA is not compliant with the European Benchmark Regulations (BMR). So, despite having a pre-existing pool of liquidity, EUR swap markets are going to have to transition to a new RFR, ESTER. Which isn’t being published yet.

- There are loads of mortgages across Europe linked to EURIBOR. Whilst there are efforts to reform EURIBOR to make it compliant, it is possible that both EONIA and EURIBOR disappear at some point. The mortgage link brings a retail aspect to the impact of Libor reform and RFRs that is largely missing for the US and UK (most USD mortgages are fixed rate, whilst floating GBP mortgages are linked to “bank rate”, not LIBOR).

- European banking remains rather dislocated, with different market dynamics in different countries. The impacts on EURIBOR fallbacks for e.g. derivative hedges versus the underlying transactions could differ from country to country.

With that mindset, I took a look at the “Second public consultation by the working group on euro risk-free rates on determining an ESTER-based term structure methodology as a fallback in EURIBOR-linked contracts”. Catchy title, eh?

Forward Looking Term Rates

Perhaps this is obvious, but I think it is important to note that this consultation is supportive of the work ISDA has done on LIBOR fallbacks, and John notes in his blog this week that it is important that those fallbacks are consistent across all ‘IBOR indices, so as not to completely mess up my favourite Cross Currency Swap market!

But remember that the ISDA work on fallbacks only strictly applies to products governed by an ISDA master agreement – i.e. OTC derivatives. We could see different fallbacks for different asset classes.

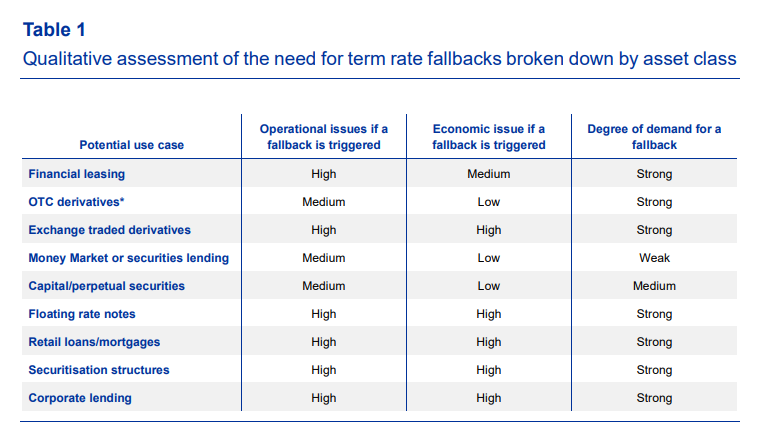

This consultation in Europe therefore draws a distinction between the ISDA work on fallbacks, and the need for a forward-looking term rate for (broadly speaking) other asset classes. The impact assessment is below for all the potential asset classes:

The answers to this are going to be interesting as:

- The derivatives industry as a whole will probably suggest that OTC derivatives are fine, we can deal with backward looking compounded fixings plus a spread – there is no need for a term fixing. This means that all OTC derivatives contracts will be fungible and there won’t be differences across currencies. Everyone can use CLARUS01!

- The same should really apply for Exchange Traded Derivatives. There is no particular need for these to have a forward-looking rate.

- It might also be argued that the large margins on retail loans and mortgages should be great enough for banks to take a pragmatic view and just offer a 30-day payment period for interest amounts. The convexity risk isn’t large enough to wipe out the margins!

- It will be interesting to hear what the other areas of finance have to say. Which of the above really has an “essential” need for a forward-looking term rate?

Methodologies

Assuming that some areas do require a forward-looking term rate, the irony is that this will almost certainly have to be based upon transactions in OTC derivatives (which don’t really need a forward-looking term rate).

This consultation includes 3 possible methodologies based on OTC derivatives (transactions, quotes and hybrid), plus one using futures data (similar to the ICE methodology).

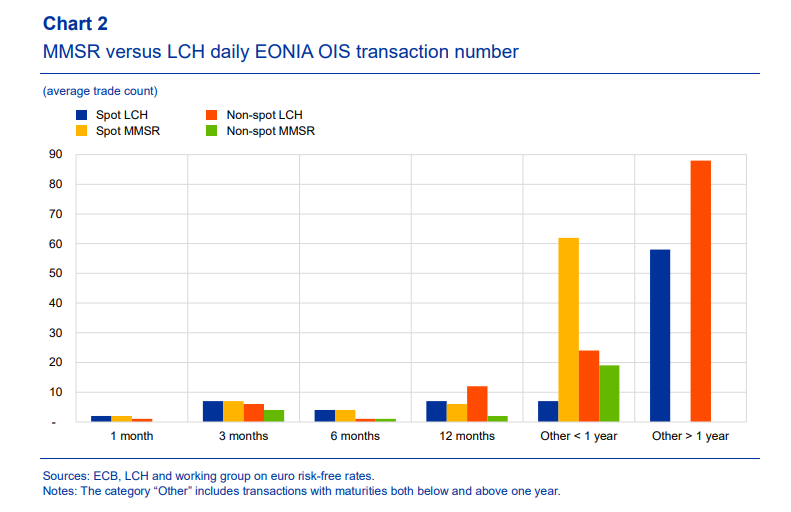

There is some interesting data here, not least the number of EONIA OIS trades at LCH:

- There are an average of 2 spot starting 1 month EONIA trades cleared at LCH per day. Including forward starting swaps increases this to 3 per day.

- There are 13 spot and forward starting 3 month EONIA trades cleared at LCH per day.

- The most active maturities in terms of number of trades are all greater than 1 year.

- This data covers the period July 2017-June 2018, which saw a complete lack of volatility in EONIA.

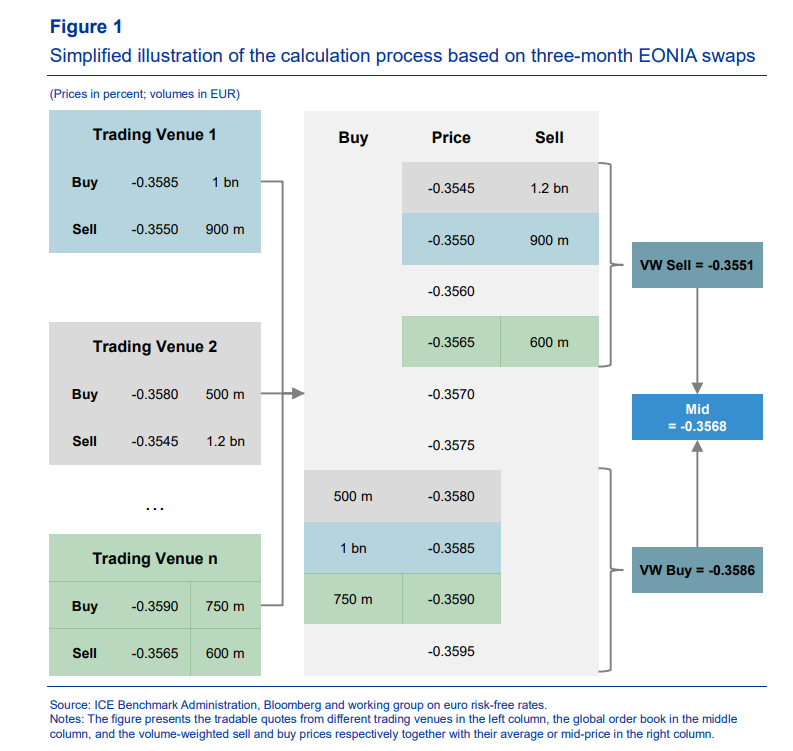

I was quite shocked at the tiny number of transactions. Unfortunately, it points towards the fact that any forward-looking term rate fixing will be quote based. There is a nice pictorial of a VWAP calculation provided:

Basis

A notable downside of current market infrastructure is the potential for identical products to be priced differently across CCPs. This is an explicit acknowledgement that a swap traded at LCH is not directly fungible with a swap traded at Eurex or CME. We remain concerned that any development of a quote-based fixing may be hamstrung by this differential, as we may see “Term ESTER at LCH” fixing along with “Term ESTER at Eurex”. This makes the idea of “simply using quotes” more complicated than ever before and raises the question of which CCP-rate we should fallback to. Tricky….

In Summary

- Ideally, all areas of finance will rally behind backward looking compounded in-arrears RFRs as the preferred ‘Ibor fallback.

- This consultation suggests that this may not be the case and it will be interesting to see which asset classes truly believe that a forward-looking term rate is “essential” to business.

- Given the small number of transactions, a quote-based rate would be most likely. Again, this risks recreating the existing problems we already have with EURIBOR.

- CCP Basis could further complicate these quotes as separate term rates for different CCPs may need to be maintained. Which CCP will existing term rates roll back to?