Dealers and market participants

Over the last year it has become obvious that Libor will not have a long-term future; so why are market participants still writing derivative and loan deals as well as issuing bonds linked to Libor?

Liquidity in markets linked to new benchmarks is gradually increasing but still falls short of dominating Libor-based product. We have seen growing trade volumes and issuance referencing SONIA and SOFR but something is missing: could it be a term RFR (TRFR) rate set at the start of the relevant period?

For example, 3 month Libor sets at the start of each 3 month period and ‘fixes’ the rate for the next 3 months.

The feedback from a number of Outreach surveys shows a significant proportion of market participants would be active users of TRFRs. These surveys include:

- Bank of England consultation on term SONIA RFRs in July 2018; and

- US ARRC (Alternate Reference Rate Committee) consultation on FRNs in September 2018.

Although dealers did not indicate a preference for TRFRs, many of their customers would likely be active users.

Why use TRFRs?

The Outreach consultations have highlighted a number of reasons why many participants and customers find TRFRs much more appropriate than the compounded RFR (settled in arrears) approach used in SONIA and SOFR OIS markets.

- Fewer system changes are required. TRFRs behave similarly to Libor in systems as the rate can be entered at the start of the relevant period. This is particularly important for loan and securitisation systems as well as many derivative systems.

- Cashflow management can be predicted and accommodated in similar ways to current methods. Many users have processes that require forward planning for funding and settlement of cashflows. Knowing the cashflows well in advance rather than only a few days allows for better liquidity planning.

- Hedge effectiveness of derivatives to underlying exposures. There is strong demand for TRFRs from users of cash instruments (e.g. loans and securitisation) which requires derivative hedges to be matched to the exposures and reference the same TRFRs.

TRFRs minimize the changes and forecasting issues for many market participants across many products that currently reference Libor. Derivative markets are often used to hedge these exposures and would likewise need to reference TRFRs.

The challenging transition from Libor to RFRs would be made easier by minimising the changes required for many products and users.

A faster transition to RFR products and markets

The question I posed at the start was, why are trades still being done referencing Libor?

Something is missing to allow a faster transition from Libor to RFR based products and trades. And recent research suggests one of those ‘somethings’ is a TRFR that allows for a much easier adoption by many users.

Market makers and dealers can accommodate the compounded, settling in arrears methodology (as recently described by ISDA and summarised by Chris here) but a significant group of users will find operational problems with this approach.

A TRFR would very likely reduce many of these operational issues for users and facilitate a faster and easier transition from Libor to RFR based markets.

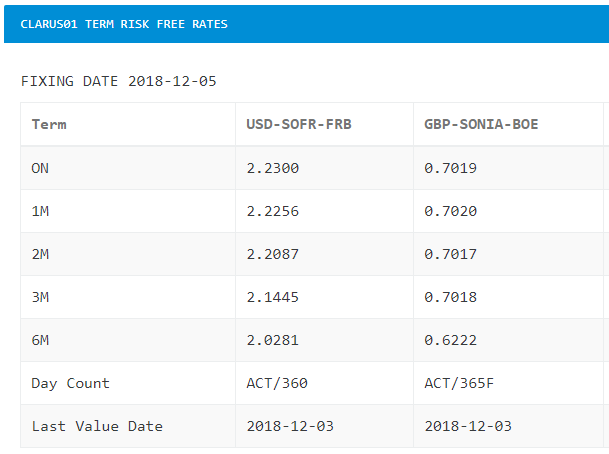

For this reason the freely available Clarus01 page provides exactly these TRFRs.