Guest Blog Series

Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

A wise man once asked me: Why don’t we all trade OIS instead of Libor swaps?

The answer-in-a-nutshell goes something like liquidity, customer demand and habit.

Certainly, if you look in the futures space, liquidity is concentrated overwhelmingly in Libor-linked products. Corporate customers hedging commercial loans require a Libor hedge, and they therefore also need a comparative cost of bond issuance in Libor terms.

However, CCPs pay OIS rates on margin accounts. Therefore, any customer operating in the cleared world is ultimately subject to OIS discounting. With mandatory clearing enforced, why do we need to bother with Libor swaps at all – particularly for financial counterparties?

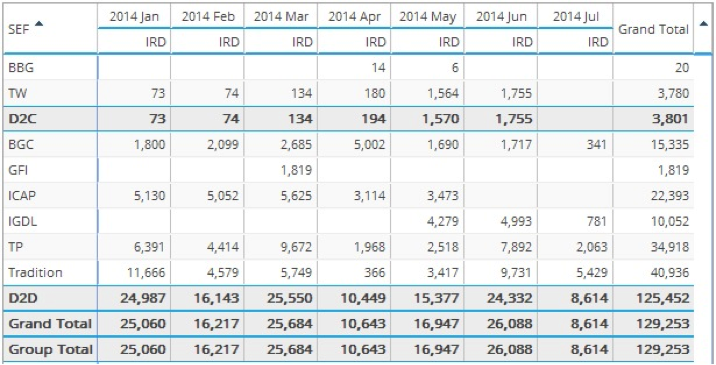

The data shows that Libor-linked products are still de rigueur. Using SEFView, we can see a distinct lack of customer (D2C) activity in EUR OIS (Eonia swaps) during 2014:

The figures above are shown as 5Y USD equivalents. Comparing a like-for-like duration traded versus Euribor linked products, we see €129bn vs €847bn. If over 6.5 times the duration is trading in Euribor, are OIS products that relevant?

In a word, yes. We are beginning to see some very interesting figures come through in EONIA space. Following on from last week’s FRA Wars, last month’s trading figures in Europe are somewhat surprising. From SDRView, we see that for EONIA swaps, the headline figures read:

- 1218 swaps traded

- Only 323 of these swaps start within T+6 days

- Broken dated swaps are the most common tenor – 372 swaps

It therefore follows that forward starting, broken dated swaps are the most commonly reported Eonia swaps. Off the top of my head, I assumed this reflected either ECB-dated swaps or very short-term repo-related hedges. After-all, Eonia is a short-end product, right?

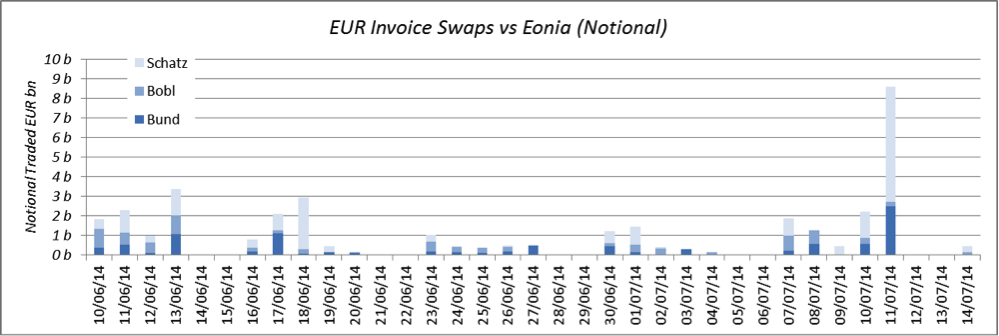

I couldn’t have been more wrong. What we actually see are a plethora of hedges sharing the same dates as the Eurex Schatz, Bobl and Bund contracts – commonly referred to as Invoice Spreads. Indeed, of this particular subset of Eonia swaps, over 76% match the Eurex contract dates.

Breaking this down, the volumes are on the up as we progress through the month. If we look at it in notional terms, there was a huge amount of activity on 11 July:

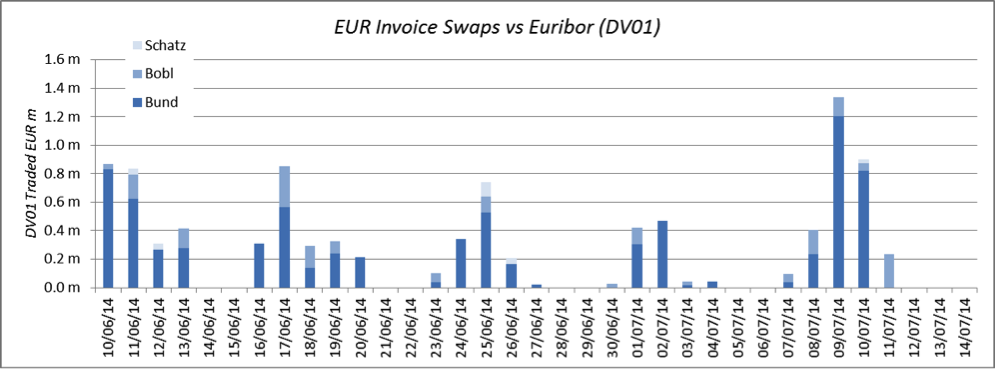

All of this in isolation is a mere curiosity. A case of data-mining for data-mining’s sake. However, we can demonstrate that these so-called invoice-spreads now trade in Eonia space more than in Euribor space. If we look at the DV01 traded in invoice swaps v Euribor we see the following for the past month:

Showing that:

- A total DV01 of €9.8m EUR traded in Euribor-linked invoice spreads

- Bund hedging makes up over 78% of the total

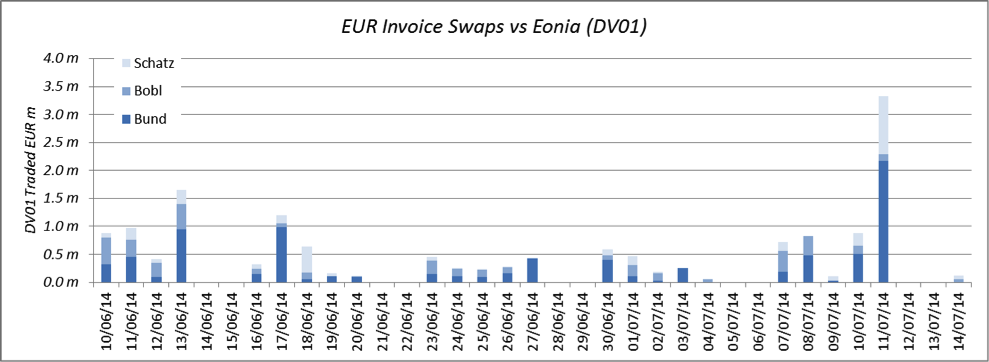

It is worth putting this data in perspective. From my previous blog, approximately €290m of DV01 trades for all Euribor-linked swaps in a similar month-long period. However, these relatively small areas of the market are often first to highlight new trends in the data. And this appears to be the case here, as there is a greater DV01 traded vs Eonia than Euribor for these products:

- €15.5m of DV01 traded – 1.58 times more than in Euribor invoice spreads

- 53%, 25%, 21% split Bund, Bobl, Schatz

- There was an enormously active day on 11 July, when over 20% of the month’s risk traded.

I think we can make a reasonably good stab as to why this trend is occurring. The precise product we are looking at is the almost exclusive realm of swap dealers. It is a product that allows liquidity providers to transform Bund-futures liquidity into Swap liquidity. These market participants mark all of their exposures back into OIS space. They are therefore pioneering the move into more suitable risk-management behaviours.

However, whilst I am a big proponent of these risk management changes, it does result in a rather strange market structure. The original question might be extended to say “If Libor is a made-up number, why not trade OIS?” It is difficult to refute that – but we are now seeing moves towards a swaps market that trades “made-up” swaps. Why would any sane market choose to focus liquidity on swaps that start the tenth day of every quarter and mature according to a Cheapest to Deliver German government bond basket? You really couldn’t make that up….