- The Bank of England is running a consultation on term SONIA reference rates.

- We take a look at a complementary solution.

- We produce compounded SONIA in-arrears term fixings to help end-users adopt SONIA.

Making Our Lives Easier

François Jourdain, Chair of the Working Group on Sterling Risk-Free Reference Rates, recently stated that our industry needs to “make our lives a little bit easier”:

He was referring to what can be done to aid the transition away from Libor towards SONIA (and other Risk Free Rates, RFRs).

One of his particular comments at the BoE Markets Forum back in May this year really struck a chord with Clarus. François said that it would be helpful to have an ACT360 or ACT365 term-equivalent to a SONIA compounded in-arrears rate.

So we’ve created an app just for that within CHARM.

The BoE consultation on SONIA Term Rates

Generally, I share the opinion of François Jourdain that “people are a little bit afraid of compounding”. Amongst the reasons why, I’ve heard it said that:

- Some systems are not set-up to cope with daily compounded rates. Whether these are legacy internal systems, or simply vendors charging for additional complexity, is a moot point – it has been noted in some Working Groups that it may represent an implementation challenge for RFRs.

- Most people understand a simple annualised interest rate as being equal to “interest rate * fraction of year”. Our lives would be easier if RFRs also operated in the same manner, instead of being “compounded in-arrears”.

This is true for a subset of the market. When talking about the adoption of RFRs, we are not just talking about the liquid, cleared OTC derivatives market. We have to consider all users of LIBORs. As such, the BoE consultation on term SONIA puts it very well:

Derivatives markets participants are ‘fluent’ in the direct use of overnight rates, where payments are calculated based on an average of realised daily rates. But an important subset of end users in loan and debt capital markets report that term rates are essential for their business needs.

It is well worth reading Annex 2 of the consultation to look at the 13 potential uses of term rates under consideration.

And Of course, you should respond to the 10 questions posed by the consultation itself to make sure we get the right answers as an industry!

From a Clarus viewpoint, we believe that if a Term Fixing cannot be created from existing data in SDRs or Trade Repositories – or via MIFID II Data – then it probably isn’t anchored in enough transactions for it to avoid the same problems LIBOR ran into.

We therefore prefer the idea of publishing simple fixings, that act like a term rate, but take the SONIA in-arrears compounded rate instead – to be consistent with the professional users of derivatives.

Convenience

The BoE consultation mentions that the recent EIB Sonia FRN incorporated a 5-day payment lag to make the administration of coupon payments simpler. Can something similar be made to work for other end users of SONIA and other RFRs?

LIBORs were so convenient – and hence became such a widely used benchmark – because:

- LIBOR were term rates.

- You put in a fixing at the start of the period in your system.

- You didn’t need to pay anything until the end of the period.

- It was unusual for a LIBOR trade to compound.

All of this means that some end-users (such as a corporate) would know their cashflows up to three, six or even twelve months in-advance when trading a floating rate LIBOR swap. This was a nice-to-have in the early days of derivatives trading, but has now seemingly morphed into “this is how we’ve always done things, we don’t want to change” intransigence.

However, it should be stressed that the convenience in knowing where your cash-flows will be next month is almost certainly offset by the fact that your “hedge” is not going to be as effective as if you were trading versus overnight rates. A twelve month LIBOR fixing will not hedge you against any changes in central bank rates over the next year.

A forward-looking term rate also has an inherent credit component built into it (LIBOR specifically has bank credit). But if we moved to any other term fixing it would naturally incorporate some element of counterparty credit into it.

Tail Winds

RFR adoption needs some tail-winds.

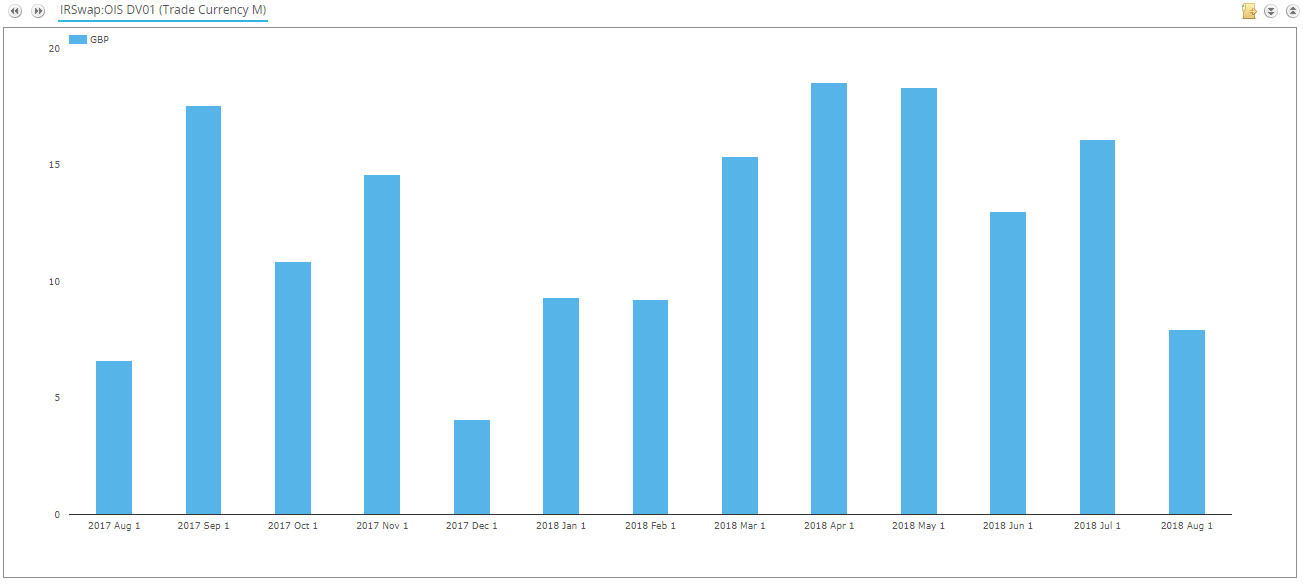

SOFR swaps have started trading. And SONIA volumes have seen all-time records traded in May 2018:

Showing;

- DV01 risk traded each month in SONIA linked products and reported to US SDRs.

- We can see that for overall risk traded, 2018 has been a stellar year. Records were hit in April, May and July wasn’t far behind.

- In terms of notional cleared, LCH saw £3.5trn cleared in May 2018 – an all-time record.

- We also know that SONIA trading has increased to 15% of total risk traded in GBP IRS.

However, we need to be realistic and recognise that more still needs to be done.

There’s an app for that

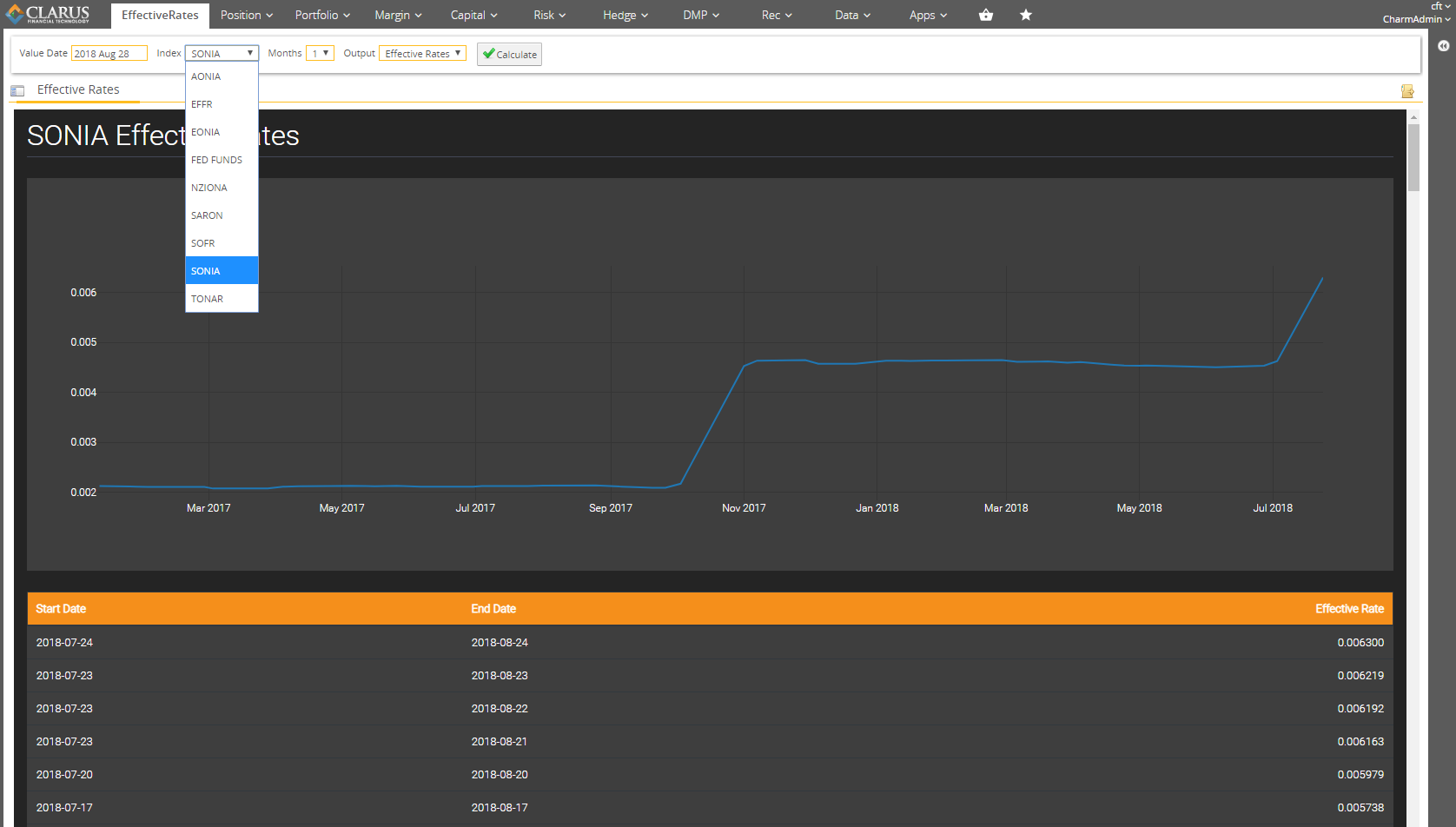

In direct response to the BoE Markets Forum, we’ve developed an app within CHARM to create these term fixings in-arrears from all of the RFRs that we have blogged on.

Showing;

Showing;

- Our Effective Rates app.

- We use the history of overnight RFR fixings to compound and create the equivalent, annualised term interest rate (1 month rates are shown above).

- The fixings are calculated in-arrears.

- Taking the “Effective Rate” column allows users to apply the standard formula of “fraction of year * interest rate” to calculate their cashflows for the specified period.

- The app calculates 1 month, 3 month and 6 month tenors.

Our readers can have a play around with the embedded version below for the 3 month SONIA fixings. Please let us know your feedback.

Publishing

We’d like to hear from anyone working on RFR projects and who is interested in consuming the output of these calculations.

To make your life easier, what is the best way for us to publish these rates?

They will soon be available as part of our microservices tool – so you can easily get a CSV file, and they can already be exported from our app.

Do you have any other suggestions to make these fit into your current eco-system? We are familiar with how banks would consume these, but really want to hear from our end-user audience.

This isn’t about performing the calculations, or providing an IT solution, it is about giving RFR adoption the tail-wind it needs to thrive.

As an aside, it is also worth thinking about the new SONIA futures. The 3 month contracts from both ICE and CurveGlobal settle against these compounded in-arrears rates, whilst the 1 month contract from ICE is versus an average SONIA fixing. Does anyone else need an average one month fixing? Let me know.

In Summary

- We produce SONIA-in arrears fixings for 1 month, 3 month and 6 month terms.

- These act like term rates, but are fixed at the end of the period.

- There is evidence that this simple solution can help end users to adopt RFRs.

- We want to help create tail winds behind the RFRs to ensure their successful adoption.