The conversation on the use of RFRs (Risk Free Rates) has been developing over the past few months and in this article I will focus on cross currency swaps.

The current development of markets in RFRs

In most cases the focus has been on single currency swaps where the development of markets based on RFRs has been slower to develop than many expected.

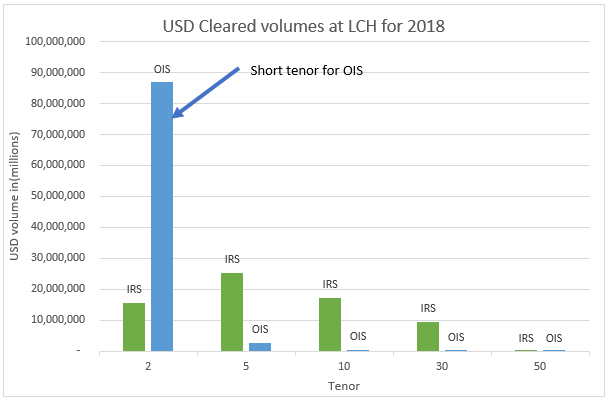

For example, CCPView shows USD IRS cleared at LCH has a volume weighted average tenor of around 10 years with USD 69 trillion cleared over 2018. In comparison, the USD OIS market cleared around USD 90 trillion over the same period but with an average volume weighted tenor of 2.1 years. The volumes are comparable but the OIS market has a much shorter tenor.

(Note our tenor granularity is limited to 2Y, 5Y, 10Y, 30Y, 50Y, so OIS could well be much shorter than 2Y).

As the SOFR market develops the tenor of the OIS trades will likely increase to match the IRS more closely, keep an eye on CCPView for this over the next few months.

I also note that the GBP IRS and SONIA markets show very similar results to the USD LCH-cleared tenors.

Cross currency swaps

Cross currency basis swaps present a number of problems that do not exist in single currency swaps:

- If one side triggers to a fallback (e.g. Libor cessation) then does the other side (e.g. JPY) trigger automatically?

- How are markets going to develop RFR-based cross currency markets? Are they RFR on one side (e.g. SOFR) and non-RFR on the other side (e.g. CDOR)?

- How do we align payment dates when RFR markets have different payment date offsets?

- How do users use the new RFR markets to hedge underlying risks (e.g. bond issues) which may be based on fixed rates or RFRs that are not compounded?

Work is progressing quickly on these issues and we will see further information and consultation from US and UK working groups.

But one word of warning: the new markets will likely be based on single currency conventions (as are the current IBOR markets) to enable transparency and efficient system changes. In this case, the end-users will have to take great care to ensure their derivative hedge actually aligns with the risk!

ISDA developments

In late December, ISDA released a summary of the responses to the fallback consultation. If you have not read this yet I highly recommend you do so soon. The responses are varied and hold much valuable information on the concerns of many market participants. The Clarus response is frequently quoted (we think we are the “European nonfinancial corporation” referred to in the summary of responses), and of particular note for this blog, ISDA chose to highlight:

A European nonfinancial corporation commented that “[i]f two currencies use different fallbacks, then FX products referencing these LIBOR rates – e.g. Cross Currency basis swaps – can no longer fund themselves in an economically equivalent manner. This has the potential for large disruption and re-pricing of risks in these markets.”

The consultation was focused on GBP, CHF, JPY and AUD markets but had an additional section on the applicability to other currencies like USD and EUR. The common view was that the results should be applied where possible to all currencies to avoid expensive and complex process changes. So expect to see similar fallbacks from future consultations!

In summary, ISDA is going ahead with developing fallback language consistent with the ‘compounded in arears’ RFR calculation and a ‘historical mean/median’ spread calculation. The compounded RFR preference was widely expected and showed up as a clear winner in the consultation. But the responses were more even in the spread calculation with the preferred version somewhat ahead of the alternative (forward curve method).

Chris in his recent blog commented on the implications of these outcomes. This highlighted the challenges of implementing the spread basis curves particularly the dependence on the assumed timing of the cessation trigger event. Is this 1st January 2022? Or should it be another date?

The implications of the preferred spread calculation are complex and can lead to differences in valuation among market participants. This can be a source of disagreement for restructuring, variation margin calculations, novations and closeouts in derivative markets.

What to watch in 2019

2019 is shaping up as an interesting year for RFR market development. I will be watching:

- When OIS trading volumes overtake Libor volumes in longer tenors;

- Cross currency swap conventions and trading based on RFRs;

- Implementation of the new ISDA fallback language; and

- Development of RFR products suited to end users.

As the new markets develop and grow in volume the existing, Libor-based markets could become less liquid especially as 2022 approaches and a Libor cessation is more likely. The basis market for switching from old to new markets will also be something to watch closely.

If the liquidity shifts quickly then all market participants should be prepared with process, system and valuation changes.

I really expect important changes to derivative markets in 2019: we should all keep well informed.