CLARUS01

Are you currently using LIBOR01? What will you do if (when?) Libor is no longer published?

We have a simple solution – use CLARUS01 instead. Find it at rfr.clarusft.com.

What is CLARUS01?

Libor. Risk Free Rates. Benchmark reform. We believe that Interest Rate trading is about to fundamentally change.

Clarus want to help during that transition phase and beyond.

If you are already using LIBOR01 we want to make your transition to new RFR trading as simple and easy as possible.

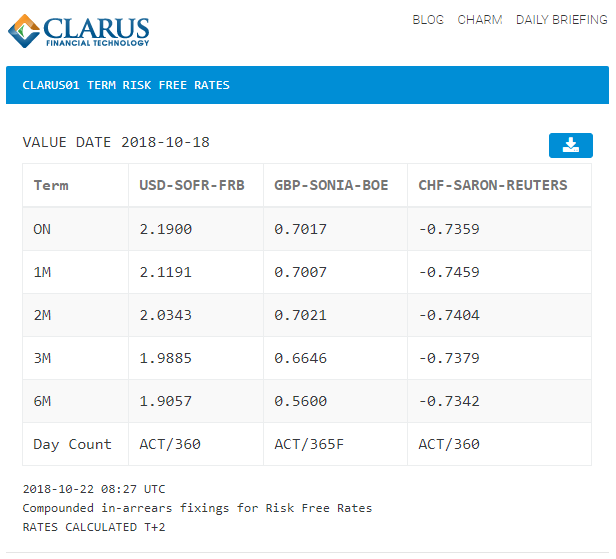

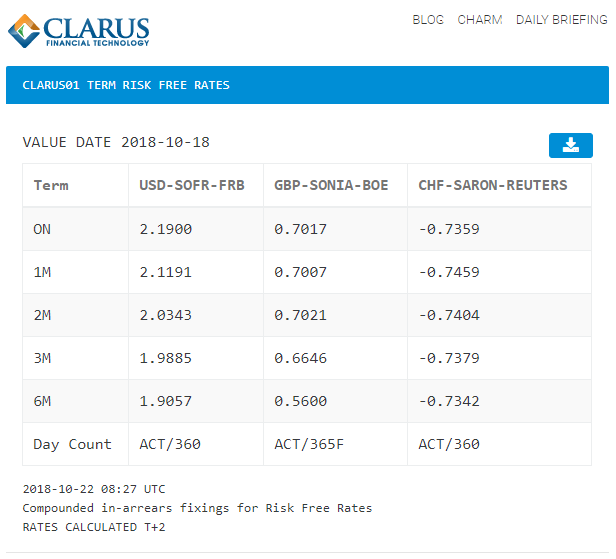

We therefore provide term fixings in-arrears for USD SOFR, GBP SONIA and CHF SARON at rfr.clarusft.com.

This list will extend in the future as we get more data and clarity from other currencies (e.g. we are waiting for EUR ESTER to be published).

Why CLARUS01?

CLARUS01 provides the answer to two questions.

Question 1: How can I easily trade new RFR swaps?

CLARUS01 allows you to treat an OIS trade exactly like a vanilla, LIBOR swap. No need to worry about daily fixings or compounding. Our fixings act just like a LIBOR term fixing. They are compounded, in-arrears fixings. This means that you just need to look up a single fixing for a single interest rate period.

Question 2: What am I going to do if LIBOR stops publishing?

CLARUS01 provides the most likely fallback calculations for LIBOR if the fixings are no longer published. We believe that this is very likely to happen after 2021.

CLARUS01 – Inspired by the Bank of England and ISDA

CLARUS01 has been created in response to two recent industry-wide consultations.

First, the Bank of England consulted on Term SONIA Fixings (so-called Term Sonia Reference Rates, TSRRs). We blogged on this previously, stating;

“It would be helpful to have an ACT360 or ACT365 term-equivalent to a SONIA compounded in-arrears rate.”

The BoE consultation has extended its deadline to Friday October 26th. Clarus have already responded and we strongly encourage all market participants to do so. In our response, we stated:

We believe that a transition to SONIA for end users would best be achieved by changing market conventions, rather than introducing TSRRs. Clarus are calculating SONIA term fixings in-arrears. We aim to do this for all RFRs [at rfr.clarusft.com].

We do this because we believe that the market is best served if end-users of derivatives use the same fundamental building blocks as are used in cleared and listed derivatives markets. This ensures that all markets referencing SONIA are aligned.

Using term fixings in-arrears means that end-users do not need to implement compounding into their systems. Clarus calculate the equivalent term rate for a period and this can be applied in exactly the same way as previous LIBOR fixings. Compounded rates are restated into an equivalent simple term rate.

If end-users require cash-flow certainty for longer than the payment lag of a SONIA swap, they can perform a rolling hedge to match the payment dates of their underlying instrument.

Secondly, ISDA consulted on LIBOR Fallbacks for AUD, CHF, GBP and JPY markets – with preliminary thoughts on USD and EUR also vetted. We blogged on the ISDA consultation previously. It closed on Monday October 22nd. Clarus responded with the following:

A Compounded setting in-arrears is our strong preference. As a provider of data and analytics, Clarus would like to help the broad market uptake of this solution. To achieve this we are now publishing the compounded setting in-arrears at rfr.clarusft.com.

The best way to replace Libor, a forward-looking rate, is to include all of the overnight fixings that take place during the time-period that a term Libor fixing encapsulates. Anything else will necessarily use an overnight rate that does not correspond to the exact period to which we are calculating interest.

We are strong proponents of the Forward Approach [for spread adjustment]. We believe that this will minimise value transfer, enable smooth transition for both short-term and long-term Libor/OIS positions and leverages current market best practice. The Forward Approach should encapsulate all current market information and avoid any unfair bias to particular market participants.

How Does CLARUS01 Work?

Access CLARUS01 at rfr.clarusft.com.

The Rates are available for download to csv, making them simple to consume for everyone.

Anyone wishing for more flexibilty (e.g. custom date periods and accruals), should contact us for full access to our Effective Rates app within CHARM.

Risk Free Rates are coming

Make sure you are prepared for Risk Free Rates.

Make sure you are prepared for LIBOR disappearing.

Check out CLARUS01 at rfr.clarusft.com today.

Interesting article Chris! However, it looks like the rate shown up in the Clarus01 is in-advanced (backward looking) instead of in-arrears (forward looking).

Thanks for the comment! It’s difficult to exactly clarify terminology here. Clarus01 mirrors the current fixing process for a vanilla OIS transaction. But instead of users having to consume the fixings daily and compound them, we do all of those calculations in the background. We then publish a single fixing for the period, and that fixing is published at the end of the period. Hope that clarifies!