SOFR Futures and Swaps – November 2019

Last week we covered SOFR Market Developments covering the comparison of SOFR derivatives volumes vs Libor and FedFunds, which highlighted the massive growth that needs to happen for SOFR to surpass Libor as the primary interest rate reference index. Every firm active in Futures and Swaps should be tracking the uptake of SOFR trading and […]

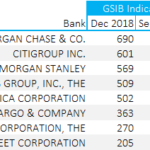

G-SIB Scores for US Banks

We detail the GSIB methodology for US banks, referred to as “Method 2” in the literature. We calculate the GSIB scores for 8 US banks as at December 2018 and September 2019. We find that the Method 2 scores are particularly penal for Morgan Stanley. It will be interesting to see how these scores change […]