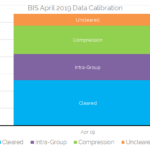

What Is the Total Size of Rates Markets?

Rates markets have grown to stand at over $350tn in monthly volumes. Our data product, CCPView, provides transparency data covering 93% of these global volumes on a daily basis. We benchmark our data versus periodic BIS data below. Data analysis needs to be timely and accurate. Contact us today for a CCPView subscription. During recent […]

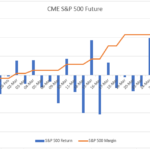

CME S&P 500 Futures Margins in March 2020

In a recent blog, procylical margins in the time of covid-19, I reproduced a chart from a BIS Bulletin showing that IM requirements for US Equity Index Futures doubled during March, the peak of the covid-19 market crisis. Today I will take a detailed look into these margin changes, concentrating on the S&P 500 index. […]

US Treasury Market Volumes During COVID

We have started collecting post-trade transparency data for US Treasury trading. I’m sure a lot of market participants have been analysing this data already. Our particular Clarus angle is to compare these UST trading volumes against the rest of the Rates trading landscape – specifically Bond Futures (at CME) and versus cleared Interest Rate Swaps […]

Every Single Street in the City of London

As the Covid-19 lockdowns come to an end, I wanted to write something different from the usual and so today I will look back at how I spent some of my free time. Many of us took on new activities and projects; one of mine was to walk every single street in the City of […]

What You Need to Know About CNY Swaps

CNY Swaps are the 9th most traded interest rate swap at CCPs. The market is quite standardised, with 90% of volumes in just three tenors. Clearing is split between Shanghai Clearing and LCH SwapClear. 60% of the market is now cleared. When I took a look at trends in 2019 for swaps market data, I […]

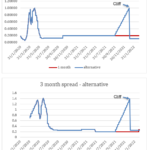

ISDA Fallback Spreads – Predicted and Alternative Scenarios

ISDA continues to make progress towards providing more certainty about the way forward for derivatives post LIBOR. This includes the calculation of the ‘fallback spread’ which is to be applied to the preferred fallback compounding methodology to minimize value transfer when the fallback is triggered. The fallback spread is calculated as the 5-year median difference […]

Backtesting of margin models

Given the recent increases in initial margin that I covered in a few recent blogs (see Procyclical margins in the time of Covid-19 and Crashing rates and swap margins), I wanted to look into backtesting of margin models. Background Backtesting is a well established practice, widely used by all CCPs to check the adequacy of […]

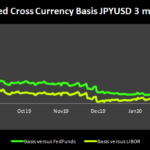

$300bn FX Swap Rollover

June sees $295bn of 3 month USD funds provided by central banks expiring. With the Bank of Japan accounting for 50% of the outstanding amounts of these facilities, USDJPY cross currency basis (and FX) will be a focus for these maturing funds. The price differential between the central bank facilities and market-based pricing has shrunk […]