Clarus Top Blogs of 2016

For my last blog article of 2016, I would like to highlight our top blogs and themes of the year. Top 10 New Blogs in 2016 First the new blogs that we published in 2016. FRTB – What You Need to Know FCM Rankings – Q1 2016 Margin Valuation Adjustment FRTB – Internal Models or Standardised Approach FCM […]

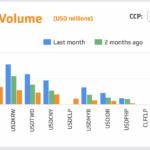

NDF Volumes – It’s all about Clearing

Cleared volumes are now a significant portion of the NDF market. The percentage of the NDF market that is cleared has steadily increased every month since September, to now stand at 14%. We estimate that 35% of Dealer-to-Dealer volumes are now cleared as a consequence of the Uncleared Margin Rules. A Brief Recap Our SDRView data products display trades […]

SA-CCR: Standardised Approach Counterparty Credit Risk

On 1 January 2017, the Standardised approach for measuring counterparty credit risk exposures (SA-CCR) will take effect. SA-CCR is required for Credit Risk Capital, as well as Exposures to CCPs and the Leverage Ratio. It is particularly important for Derivatives as it provides for improved netting benefit and recognition of margin for both cleared and bi-lateral […]

Why FCMs Don’t Like Intraday Margin Calls

We keep on hearing how difficult it is to be a clearing broker these days. Case in point – this Risk.net article discusses how FCMs had to find billions of dollars in the middle of the day after the Brexit vote. This is because, when the market moves, Clearing Houses can choose to make margin calls […]

ISDA SIMM™ – Swaptions IM in Excel

We build an IM calculator in Excel for Swaptions under ISDA SIMM™. The methodology builds on the margin methodology for linear products, and uses very similar formulae. There are some subtleties around multiple currency portfolios that we expand upon. We also introduce the concept of Curvature Margin which is calculated via theta and lambda multipliers. UPDATE: We […]

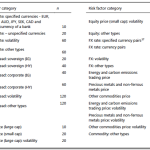

FRTB – Modellable Risk Factors and Non-Modellable

Following on from my article FRTB – Internal Models or Standardised Approach, I wanted to look at specific component of the Internal Model Approach (IMA), namely the fact that all risk factors are subject to a Modellable or Non-modellable requirement and non-modellable risk factors result in a higher capital charge. Background In January 2016, the Basel Committee on […]

November 2016 Swaps Review

Continuing with our monthly review series, let’s review Swap volumes in November 2016. SDR highlights: On SEF USD IRS price-forming volume in November was > $1.5 trillion Almost 50% higher than the prior month USD Swap Rates were up 50 bps for 10Y, with a steeper curve SEF Compression activity was > $250 billion in USD IRS On SEF EUR, GBP, […]

ISDA SIMM™ IM Comparisons

Clarus tools calculate margin under LCH, CME and ISDA SIMM™. It is a natural question to compare the three models. There are interesting differences across currencies and tenors. We find that SIMM is up to 37% higher than at a CCP. At last….! This blog has been sitting in my “to-do” box for long enough. It […]