NDF Clearing 2019

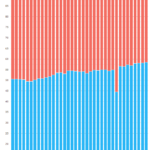

We update our analysis on NDF Clearing in 2019. We find that 20% of the overall market is now cleared. NDF volumes in Asian currency pairs have rocketed higher. Clearing volumes have reached somewhat of a plateau. Why? NDF Volume Analysis Finding up-to-date analysis on uncleared OTC derivatives is currently a frustrating job. The last […]

PaaS and SaaS – What you need to know

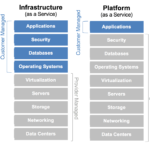

In my last blog I described the origins of Cloud and highlighted some of the benefits of Infrastructure as a Service (IaaS), but this does not reflect the real value of Cloud. To uncover this, we will explore the concepts of Platform as a Service (PaaS) and Software as a Service (SaaS). Platform as a […]

Current Clearing Rates

The death of uncleared markets has been widely over-reported. We look at Clarus CCPView and recent BIS data to look at the size of uncleared markets. Interest Rate derivatives remain the largest, followed by FX. Credit is very small in comparison when measured by notional outstanding. We strongly advocate further transparency into the remaining stock […]

Infrastructure as a Service – the Bedrock of Cloud

In this blog I will explain the origins and key features of Infrastructure as a Service (IaaS), the core foundations of what we think of as Cloud. Cloud computing is an evolutionary consequence of a sequence of technology innovations, stretching from human based computing, across generations of hardware and networking, to the advent of virtualisation […]

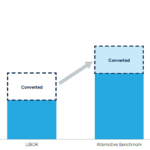

Portfolio Conversion of Libor to RFR trades

The closer we get to year end 2021, the more important the question of what will happen to existing LIBOR Swaps when and if LIBOR is no longer published or declared a non-compliant benchmark by the regulator. One approach is ISDA’s work on new Fallback language in the 2006 Definitions (see Libor Fallbacks: What will […]

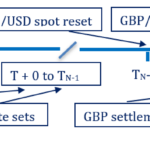

Potential Mechanics of Cross Currency Swaps and RFRs

As references to Libor declines ahead of 2021 and the use of Risk Free Rates (RFRs) increases, derivatives will have to adapt. So in this blog I will look at the cross-currency swaps and the choices needed to move to RFRs. Cross currency swaps can behave quite differently to single currency swaps and I will […]

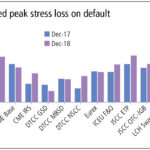

Swaps Data: IM grows in Listed and OTC markets

My monthly Swaps Review looks at the recently published CPMI-IOSCO Quantitative Disclosures by CCPs and highlights: Initial Margin YoY trends for IRS, CDS & ETD Clearing Houses Maximum total VM received on a single-day Estimated Peak Stress Loss on Default Actual largest Credit exposure Please click here for free access to the full article on […]

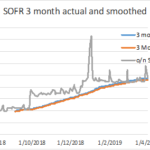

USD SOFR Volumes April 2019

Is USD SOFR trading becoming a real thing now? We use CCPView, SDRView and Clarus Microservices to measure activity levels. We find a record amount of risk traded in April 2019 versus SOFR. We also see Compression activity of back-dated trades in SOFR. Read on to find out more details. SOFR Volumes April 2019 You […]

SOFR Impacts From Liquidity Spikes

The Clarus website has a very interesting free service under the LOGIN tab called ‘Term RFRs’. This shows the compounded RFRs for the fixing date (yesterday) looking back overnight, 1, 2, 3 and 6 months for SOFR (USD), SONIA (GBP), TONA (JPY) and AONIA (AUD). This blog will look at the compounded SOFR rates for […]