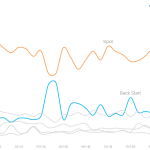

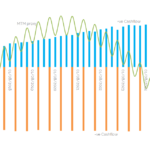

Fewer customer trades & more compression. How does a trader make money in a market like this?

We look at trade count data in the SDRs for Interest Rate Swaps in the major currencies There is evidence of reduced customer activity in large notional trades And a decrease in average trade size This is offset with an increase in Compression activity Those market trends are not very friendly towards traders trying to […]

Margin Valuation Adjustment

While it all began many years ago with Credit Valuation Adjustment (CVA), a number of new XVAs have risen to prominence in the last few years such as DVA, FVA, MVA, KVA. Chris wrote about Funding Valuation Adjustment (FVA) last week, so today I will look at Margin Valuation Adjustment (MVA). Background MVA arises when Initial […]

FCM Rankings – Q1 2016

I’ve written about the public FCM data in America a couple times before, most recently back in October 2015 here. I was keen to revisit and update the analysis to see: Growth in clearing business FCM rankings for swaps & futures Concentration amongst top FCMs Any real evidence to firms leaving the clearing business I […]

LSE and Deutsche Boerse: What the CCP Disclosures Show

The LSE and Deutsche Boerse merger to create one of largest Exchange Groups has generated a lot of press coverage and their respective Clearing Houses, LCH and Eurex, are seen as central to the transaction. (see Bloomberg). In this article I will look at the Public Quantitative Disclosures by LCH and Eurex to learn what […]

FVA for Cleared Swaps

We’ve recently added Margin Valuation Adjustment analysis into CHARM. As we’ve talked about in the past (here and here), MVA is a cost to the business because Initial Margin has to be funded for the holding period of a trade. This blog considers FVA – Funding Valuation Adjustment – caused by the Variation Margin of trades. All Swaps impart a […]

SBSDR Part 2: What will SBSDR Cost?

A couple months ago, I published an article “SBSDR: The SEC Version of SDR” detailing the generalities of SBSDR – the new trade repositories intended to capture securities based swaps such as single name CDS and equity swaps. At the time, there had been no applications by potential candidates. Fast forward to today, and it appears as […]

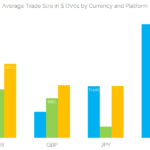

What’s the average trade size in swap markets?

We answer a simple question – what is the average size of a swap trade? We find that average size varies by maturity and currency Average trade size is also different between Dealer to Dealer and Dealer to Customer execution platforms. Overall, we find that USD swaps have the largest average trade size, at $45,000 in DV01 We’ve talked previously […]

April 2016 Swaps Review – LCH-JSCC Basis, Swaptions, AUD OIS

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in April 2016. First the highlights: On SEF USD IRS in April 2016 volume was > $1 trillion, down from >$1.25 trillion For price forming trades, DV01 was 16% lower than March 2016 but similar to April 2015 USD SEF Compression volumes were much lower than prior months USD Swap Rates […]

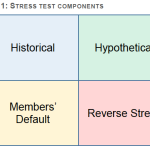

ESMA EU-Wide CCP Stress Test Results

ESMA just published the results of its EU-Wide CCP Stress Test, the aim being to assess the resilience and safety of the European CCP sector and to identify possible vulnerabilities. Given that CCPs are conservative organisations, it is no surprise to learn that “EU CCPs can overall be assessed as resilient to the stress scenarios used to […]

What is Multilateral Netting – FX NDF Clearing

Only a small portion of the NDF market is cleared We present theoretical exposures within bilateral and multilateral dealer networks to illustrate the reduction in Initial Margin that multilateral netting offers We can see that the motivation to clear varies with a dealer’s position And as positions change over time, more clearing leads to greater reductions in IM After my post last week […]