MIFID II: ESMA Trading Obligation

ESMA published their latest Consultation on Trading Obligation for Derivatives under MIFIR on 19th June 2017. EUR, USD and GBP swaps are deemed liquid and will be covered by the Trading Obligation under the current proposal. JPY, NOK, SEK and PLN swaps will continue to be covered by the Clearing Obligation but will not be […]

CME-LCH Basis For Dummies

We occasionally still get asked about the price differential between CME and LCH swaps. I typically refer folks to our online articles that have explained the phenomenon. Since 2014, we have written 18 separate pieces on the CME-LCH basis spread. A few of the ones that begin to quantify it include: May 20, 2015 – […]

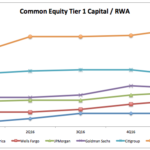

Capital Ratios and Risk Weighted Assets for Tier 1 US Banks

Following on from my recent Supplementary Leverage Ratio: Comparing US Banks article I wanted to look at Capital Ratios and Risk Weighted Assets (RWAs) published by the six largest US banks. Background One of the lessons learned from the Great Financial Crisis (GFC) was that Banks were generally under-capitalised for the risks they were exposed, leading to new […]

NDF Clearing Update

Little has changed in FX NDF Clearing since our last update in March. From the data, Clearing is now a “business as usual” operation for a significant sector of the market. We further refine our data methodology by introducing an estimate of the errors inherent in our market share metrics. These errors look to be acceptably small, at […]

Microservices: Swap equivalents in Julia

Julia is a modern high-level, high-performance language for numerical computing. Clarus API functions are easily accessed in Julia. What is Julia? Julia is a relatively new computing language, combining the ease of development (similar to python and matlab) with a Just-In-Time compiler and other language features to deliver runtime performance close to that of C. […]

EU Commission proposes more robust supervision of CCPs

There has been much recent coverage in the press about whether the EU would require a location requirement for EUR Swaps Clearing. (See City AM, Reuters, Risk.Net). Today the EU Commission put out a press release proposing more robust supervision of CCPs. What have they said pertinent to the debate about Brexit and LCH Clearnet Ltd? Lets extract […]

May 2017 Swaps Review

Continuing with our monthly Swaps review series, let’s look at volumes in May 2017 and in a change from the usual format of SDR data, then SEF market share and then CCP volumes, I will take a product centric view. Summary USD IRS Global Cleared volume in May was $4.6 trillion (up from $3.6 trillion in April) US On SEF volume […]

Clearing Mandates 2017

Which jurisdictions currently have Clearing Mandates in place for Interest Rate Derivatives? There are lots of articles and sources of information about upcoming mandates… …but finding what is already in force is more difficult. We therefore take this opportunity to summarise the Clearing Mandates that are now active across multiple jurisdictions. Sources Before we look […]

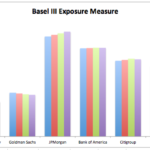

Supplementary Leverage Ratio: Comparing US Banks

In my recent Basel III Leverage Ratio article I provided an introduction to this important new metric and today I will look at the Supplementary Leverage Ratio (SLR) disclosures published by the six largest US banks. Background An underlying cause of the global financial crisis was the build-up of excessive on- and off-balance sheet leverage in banks which apparently still […]