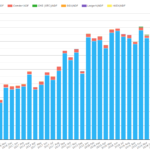

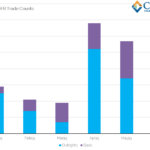

FXD Counterparty Risk Optimization and Q2 2019 Volumes

FX Derivatives (FXD) participants face a tricky choice across a patchwork of clearing and uncleared optimization techniques, trading off funding and capital usage with infrastructure spend and operational risk. In earlier posts, we showed you how FX IM optimization via NDFs and FX Options clearing developed in Q1 2019. Here I update the volumes for […]

CCP Basis – The Cost of Clearing Fragmentation

Staff Working Paper No. 800 from the Bank of England was published in May 2019. Titled “The Cost of Clearing Fragmentation”, the paper lays out a quantitative process to model the level of CCP basis. We’ll give you a layman’s guide to the paper here and show how our own data from CCPView can be […]

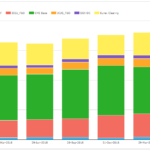

CPMI-IOSCO Quantitative Disclosures 1Q 2019

Clearing Houses 1Q 2019 CPMI-IOSCO Quantitative Disclosures are now available, so lets look at what the data shows, similar to my CCP Disclosures 4Q 2018 article. Summary: IM is up for IRS, CDS & ETD with YoY growth of 6%, 15%, 10% respectively Quarter-on-Quarter IM in CDS was flat ICE Europe F&O and ASX CLF IMs were […]

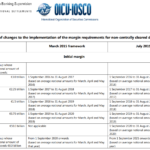

A new $50billion threshold for UMR and 1-year extension

Today BCSB IOSCO put out a press release announcing two significant changes to the UMR timeline: A one-year extension, to Sep-21 for the final UMR implementation phase for firms with > $8 billion of aggregate average notional amount (AANA) of un-cleared derivatives. An new phase for firms with > $50 billion of AANA on the […]

The ‘Dear CEO’ letters – a time to accelerate preparations

Several regulators and central banks have written to the CEOs of firms in their jurisdictions to emphasise the fact that Libor cessation is very real. In most cases (UK, EU, Switzerland and Australia) a written, often board-approved response is required. In other cases, the response is left open (USA, HK and Singapore) and firms were […]

ARRC Vendor Workshop June 28, 2019

The Alternative Reference Rates Committee (ARRC) hosted a vendor workshop recently at the Federal Reserve Bank of New York, which I attended and in this article I cover some of the key points from the workshop. Required SOFR interest rate characteristics Required trade economics and processing for SOFR-based derivatives and cash instruments Compound in arrears […]

Term Risk Free Rates from FX Forwards

The case for a Term Risk Free Rate (TRFR) to support the transition of cash instruments and products has been made by BoE and US ARRC over the past year. The TRFR is defined as a rate known in advance (similar to the current Libors) but based on RFRs in the relevant currency.

But the issue of how to construct an IOSCO-compliant TRFR has been a challenge for market participants and benchmark administrators.

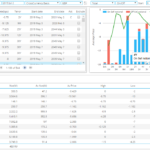

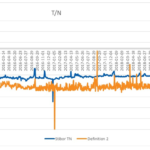

USD SOFR Volumes June 2019

SOFR traded notional hit $50bn in monthly notional for the first time. We take a look at the details of some of the block trades that drove this notional higher. LCH data shows that the amount of risk traded has been between $4m and $10m DV01 during May and June. We show how our data […]

SEK STIBOR Reform

The Swedish Banker’s Association is looking to introduce an Alternative Reference Rate for SEK markets. At the moment, STIBOR is the underlying index for SEK swaps. There are on-going consultations to introduce a Risk Free Rate in Swedish markets. We take a look at the details. SEK Markets Today As it stands today, there are […]

Cloud Security – What you need to consider

In this article we look at cloud security. With all the hype around Cloud, it’s easy to make assumptions as to what it can do, but security is an area where making assumptions can prove very costly, both financially and reputationally. This blog will look at the cloud security model, security features offered by cloud […]