Defering Bilateral Margin Rules with Low Hanging Fruit

For all those Category 1 Covered Entities in the US and Japan, the following few days should be interesting with the introduction of Bilateral Margin Rules. For all entities not yet covered by the rules, you have some time on your hands. And this time should be used wisely. As a brief reminder, all covered […]

Cross Currency Swaps – how much margin will they need?

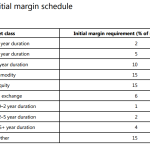

We look at the Standardised Schedule of Initial Margin for non-centrally cleared derivatives Cross Currency Swaps are a large part of the uncleared market that we did not look at last week We therefore take a look at the July volumes to estimate Initial Margin requirements for cross currency swaps Margin Requirements for non-centrally cleared derivatives The […]

非清算商品にかかる証拠金、ISDA SIMMとFRTB SA

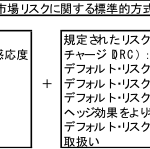

9月1日は証拠金規制の施行日であるため、このトピックを再訪したいと思う。

バックグラウンド

本件に関する私の直近の記事“米国における非清算取引のための証拠金規制”は2015年10月に投稿されていて、規制の概要とスケジュールについて記載がある。

欧州、オーストラリア、シンガポール他の国々では、規制開始日である2016年9月1日に施行が間に合わないか或いは延期を申し出ている一方で、米国と日本だけがこれを遵守し、施行しようとしている。

Bachelier Model: Fast Accurate Implied Volatility

“An industrial solution” – provides computation to near machine precision for option prices over an extremely large range! Fast and analytic in nature, employs rational polynomials to determine implied BpVol. Follows the Bachelier model; that is, dF = σdW. A new method for computing implied BP Vol (basis point volatility) analytically has come to light. It is described by […]

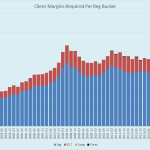

How much Initial Margin will Uncleared Derivatives require in the first month of trading?

Uncleared Margin Rules (UMR) come into effect as of 1st September So let’s play a fun little game. Take the SDR data for Uncleared Derivatives. Import this data into CHARM, our Initial Margin and Risk tool. Make a few broad assumptions about the trades and the Dealer market. We end up with an estimate of how much IM […]

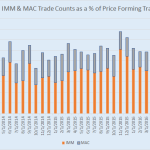

Uncleared Margin, ISDA SIMM and FRTB SA

As September 1, 2016 is the first date for the implementation of margin requirements for OTC Derivatives that are not cleared by a clearing house, I thought it would be interesting to re-visit this topic. Background My article Final US Rules on Margin for Non-Cleared Swaps, written in Oct 2015, summarises the US rules and compliance […]

30% of The Euro Swap Market Is Standardized ?

I was pulling some data recently out of SDRView and stumbled across some interesting metrics in EUR and GBP swaps. It would seem there has been a proliferation of standardized swaps, traded amongst the US-named business and reported to SDRs. GET OUR BEARINGS To begin, let’s get our bearings and terminology straight. To do so, […]

FCM Rankings – Q2 2016

It’s time to update our analysis of FCMs. The data from our last report showed a few things: The number of FCM’s reaching a 14-year low Any growth in pledged collateral being in “Cleared Swaps” A concentration of margins within the top firms, including 96% of swaps being cleared by the top 10 firms. Let’s see what, if […]

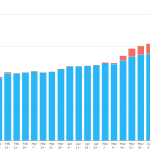

Compression and SPS in MXN Swaps

The MXN IRS market saw over MXN 6trn compressed in July 2016 This compression activity was from the first TriOptima run in MXN at CME, resulting in a large notional reduction MXN markets also see significant volumes in Single Period Swaps – which are equivalent to FRAs in all but name For on-SEF Compression, all of the […]

Swap Clearing Activity in Asia

Last month, news broke that Shanghai Clearing House was to launch FX Options clearing on August 1. The news inspired me to check for any data that might be out there. Sadly, as of today, there doesn’t seem to be any hard data to back this up. However I remained inspired enough to take a general […]