ISDA SIMM – What changes in v2.5?

ISDA SIMM v2.5 is effective December 3, 2022 Updated with a full re-calibration and industry backtesting Meaning Initial Margin will change for most portfolios In particular, material increases for Commodity and Credit risks To quantify the actual impact of SIMM v2.5 Clarus CHARM can run both SIMM v2.5 and v2.4 on your portfolios And do so before go-live, to […]

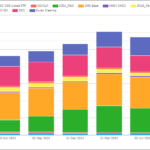

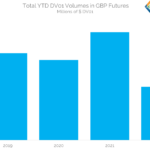

The GBP Financial Meltdown – what is still trading?

GBP markets are exceptionally volatile at the moment. We look at transparency data and find that derivatives markets are continuing to function. September 2022 will likely see the largest notional volumes traded this year. We cannot say for sure that will be the case for the amount of DV01 transacted. We consider what this means […]

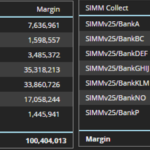

What’s New in CCP Quant Disclosures – 2Q22?

Clearing Houses have published their latest CPMI-IOSCO Quantitative Disclosures: Initial margin for ETD at $528 billion is down 7% QoQ and up 19% YoY Initial margin for IRS at $280 billion is up 4% QoQ and 8% YoY, to hit a record high Initial margin for CDS at $76 billion is up 15% QoQ and 31% YoY LME Disclosures that increase in the latest quarter are […]

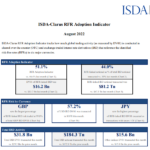

RFRs are now half of the market

The ISDA-Clarus RFR Adoption Indicator has now climbed above 50% for the first time. In August 2022 it hit a new all-time high at 51.1%. SOFR adoption increased to a new all-time high, at 57.2%. GBP and CHF continue to see nearly 100% of risk traded as RFRs. €STR trading slipped (again) to 19.3%, the […]

Here Are 6 Things I learnt after writing 400 blogs

The Numbers If I get the publishing date right, this should come up as my 400th blog for Clarus. We have a mini “leader board” on our website, and you will see that Amir is (just) ahead of me – not for long! Looking at my history on the blog: My very first blog was […]

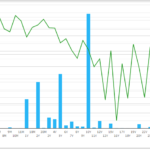

What is new in GBP Swap Markets?

We look at vanilla swaps, inflation swaps and futures. Some markets have seen volumes reduce by over 50%. Whilst others recorded all-time record volumes in August 2022. What is driving such different outcomes across a single derivatives market? With Liz Truss the newly anointed Prime Minister, the FT had an interesting take on UK markets […]