Great News: More SEF’s !?

Big news in SEF-land last week was the formal registration of 18 of the 20+ SEF’s. Generally speaking, chances are that if you have traded on a SEF, it has become fully registered. The news prodded me to go have a look at the list of SEFs on the CFTC website. In doing so, I was reminded of the […]

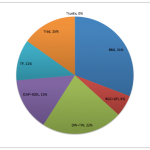

2015 SEF Market Share Statistics

In this article I will look at Swap Execution Facility (SEF) volumes and market share in 2015 for Credit, FX and Interest Rate Derivative asset classes. Clarus SEFView collects daily volumes published by each SEF and normalises this data to allow meaningful comparison and determination of market share statistics. I will use this to look […]

The Bank of England finds this interesting. So should you!

We use a recent Bank of England study to navigate Clarus data on the Swaps market. The Bank report looks at the impact of SEF trading on Rates markets… …showing that liquidity has increased and trading costs decreased. We bring the findings up to date, including API calls to replicate the study for our subscribers. Staff Research Staff […]

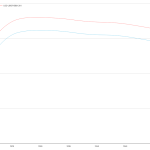

Fed Pulse – A New OIS Index

We use SDR USD OIS Volume and Price data to derive a new Fed Pulse Index The index construction takes all FOMC meeting-dated OIS that are traded across the yield curve This allows us to make maximum use of all price and volume data embedded within OIS trades Allowing us to “take the pulse” of the FOMC […]

Adapting to Direct Forward Curves

In interest rate pricing direct forward curves are defined on forward rates for a specific tenor as opposed to the more common discount factor representation, or the instantaneous forward curve representation. A simple example of a direct forward curve for 3M LIBOR would consist of a set of points and an interpolator, the points would […]

スワップのコンプレッション

・コンプレッションによるIMの減少額を示すことのできるCHARMを通して、コンプレッションのエクササイズをしてみよう

・差入れられるIMと圧縮されるNPVの比率の重要性

・資本効率性を正確に評価するための繰返し行われるプロセス

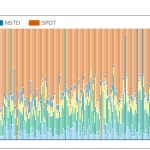

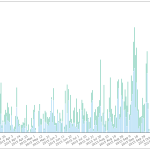

Review of 2015 US Swap Volumes in SDRs

In this article I will review 2015 US Swap volumes as reported to US Swap Data Repositories (SDRs). 2015 was an interesting year, not because of market structure change; this having already been implemented in 2014, but due to increased volatility as the Fed “will-they-wont-they-when-will-they” played out. The summary: On SEF vs Off SEF volume trends […]

A Year of CFTC Fines

aka How to solve the CFTC budget crisis. Just before the 2015 holidays, the public received word that the CFTC had its 2016 budget set at $250 million dollars, representing no change from the previous year’s budget, and significantly less than the $322m that the Chairman proposed here, and that the President had proposed to Congress. […]

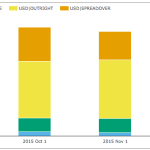

December 2015 Swaps Review

Happy New Year to our readers. Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in December 2015. First the highlights: On SEF USD IRS Dec 2015 volume was similar to Nov 2015 With Outrights and Curve trades higher, while Spreadovers and Butterflys lower The Fed Rate Rise on Dec 16 had […]

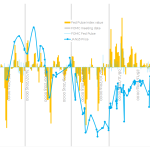

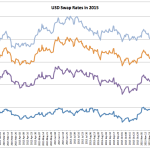

Fed Surprises in the USD OIS Data

We provide an update to our USD OIS Volumes blog from earlier last year. Highlighting that OIS structures that run from one FOMC meeting date to the next are the most common trades. This gives us a unique insight into market consensus pricing for the exact FOMC dates, unlike the 30-day Fed Fund futures contracts. We can therefore […]