Now LCH Have Converted Your USD Swaps too!

As recently as January I posed the question: That blog was written in response to the fact that 2022 continued to see plenty of USD LIBOR risk sent to CCPs. Could all of that trading just stop in time for the final cessation of USD LIBOR in June 2023? Following on from the recent CME […]

HJM-FMM Model – A Deep Dive

Authored by, Serena Manti and Gianluca Molteni of the Financial Engineering and A.I. team at List. This is the follow-up of our first post introducing the paper “Parsimonious HJM-FMM Model with the New Risk-Free Term Rates“. Here, we would like to provide you with a brief more technical description of our innovative HJM-FMM model, followed by […]

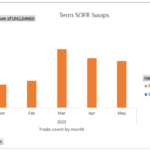

Term SOFR and BSBY Swap Volumes – May 2023

I last looked at Average and Term SOFR Volumes and Term SOFR and BSBY Volumes in early February 2023, focusing on 2022 volumes, so today I wanted to look at the 2023 data trends for these reference indices. As before we will seperate Term SOFR (published by CME) from Average SOFR (NY Fed), see the […]

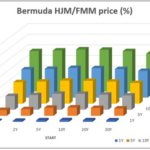

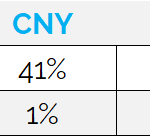

Swap Markets in China – What You Should Know

CNY Interest Rate Swap Introduction Before we look at some data on the Chinese swap markets, it is really important that readers are familiar with some of the terminology. Let’s start with the basics in terms of what the currency is actually called! Interest Rate Swap Market Conventions This blog looks at Interest Rate Swaps […]

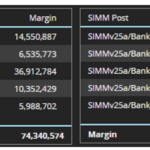

ISDA SIMM v25a the first off-cycle release

Version 2.5a ISDA has published ISDA SIMM v2.5a with a re-calibration of interest rate risk weights only. This is an off-cycle release, due to the higher interest rates volatility observed in 4Q 2022, compared to that in 2019-2021 and the stress period of Sep-08 to Jun-09; the time period used for the calibration of v2.5. Quarterly industry […]

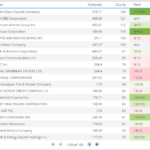

Most Active Names in Credit and Equity Derivatives – April 2023

I last looked at the most active trading names in CDS and TRS in January 2023, so today I will update that for April 2023 data. This data is from U.S. SEC Securities Based Swap Data Repositorys (SBSDRs). CDS on Sovereigns Using SBSDRView, we can find the most active sovereigns for Credit Derivatives trades in April […]

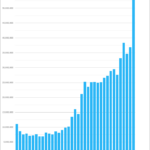

Do you know how much now trades in RFRs after the CME conversion exercises?

We’ve covered the CME conversion exercises in detail here on the Clarus blog because they were really significant events for market participants and for the broader transition to SOFR in US markets. You can catch up on the recent publications below: All of these blogs were written before we could assess the overall impact to […]

Parsimonious HJM-FMM Model with Risk-Free Term Rates

Authored by, Serena Manti and Gianluca Molteni of the Financial Engineering and A.I. team at List. In this post we would like to introduce our paper “Parsimonious HJM-FMM Model with the New Risk-Free Term Rates“, a modified version of the Heath-Jarrow-Morton (HJM) model that addresses the limitations of the traditional approaches in the context of […]

IDB Market Share in SOFR Swaps

Types of SOFR Swaps SOFR Swaps in the IDB (inter-dealer broker) market trade primarily as Spreadovers to US Treasuries. This is by far the most frequent trade type for IDBs, with the highest volume in notional or dv01 terms and the most important in setting prices of SOFR Swaps. Next are Curve/Switch trades, which are […]

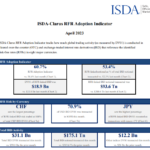

Is Now The Time to Optimise Your Initial Margin?

Initial Margin ISDA have just published the latest edition of the “ISDA Year-End Margin Survey”: We have covered previous versions of this survey, which are always worth a re-read because you can laugh at any predictions we made in the past! Sifting through all of those reveals that between $650-800bn in extra IM was anticipated by ISDA […]