ECB QE and Eonia Swaps

We take a look at Eonia invoice swaps, which match the dates for German bond futures traded at Eurex: From volume data, we see an increase in Eonia swap activity post-QE. The price action in Schatz appears closely related to short-end Eonia swaps, whilst in Bobls and Bunds it is harder to pin-down. The appearance of trades with […]

CFTC’s Roundtable on the Made Available to Trade Process – July 15, 2015

Amir presented ‘Data-based assessment of MAT’ at the CFTC’s division of market oversight roundtable on MAT meeting last week. The meeting has been recorded and is available on youtube (section starts at 0.53.04), (watch out for Tod in the audience at the top-left of the shot). The presentation slides are available for download here, […]

Webinar on CME-LCH Basis

The Recording of the Webinar is available here Please join us, CME and ICAP on Thursday 23rd July at 11:30am EST, by registering here.

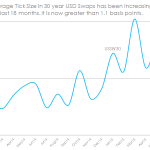

Is this the scariest chart in 2015 for Swap markets?

Clarus data shows that the average tick size in USD Swaps is increasing. We show evidence that this widening tick size is a feature across all maturities. The data suggests that the amount of liquidity has stayed constant in the market, whilst the cost of liquidity is increasing. This trend has been in place since the beginning […]

How to Fix the Broken MAT Process

aka “What I learned at the CFTC Roundtable” This past week, Amir sat on a panel at the CFTC to discuss everything MAT. I sat in the audience and heckled. And took notes. I will share those with you below. BACKGROUND If you are an avid reader of our blogs, you’d know we’ve been tracking […]

Why Are Bond Issuers Not Taking Advantage of Price Differentials?

Over the past couple months we’ve been documenting the CME-LCH basis trade including: How it’s come about Looked at clearing data for evidence of any movements between venues Looked at SEF data for which SEFs are seeing these flows The implied forward rates in the basis Downstream impacts to the CME convexity trade. Many newcomers […]

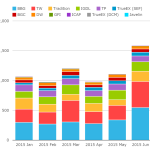

CME-LCH Basis Swaps Volumes Update

Eight weeks and six follow-on blogs later, my CME-LCH Basis Spreads blog continues to be one of our most popular blogs with a high number of daily views. So I thought it was high time I revisited the SEF volumes to see what the data shows for CME-LCH Switch trades. First a note to make […]

Patterns in the Swaps data

a.k.a Predictive Analysis in USD Swaps Clarus, ever since reporting began, have enriched both SDR and SEF data as we identify more and more trade types. Whether the trades are Compression, Spreadovers or Curve trades, we estimate that we are marking up over 1 in 2 trades reported to an SDR. But to what purpose? […]

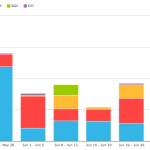

June 2015 Review – Clients start trading CME-LCH Basis

A typical month in swaps? Far from it! These were the highlights: A record ever month for SEF trading. A big increase in client flows. The data suggests that some clients used the IMM roll to trade the CME-LCH basis, in particular on Tradeweb. Bloomberg saw some huge compression flows in MAC-dated swaps after the IMM roll. Consolidation of […]

Principal Component Analysis of the Swap Curve: An Introduction

Principal Component Analysis (PCA) is a well-known statistical technique from multivariate analysis used in managing and explaining interest rate risk. Before applying the technique it can be useful to first inspect the swap curve over a period time and make qualitative observations. By inspection of the swap curve paths above we can see that; 1. […]