ISDA SIMM™: Concentration Thresholds

Concentration Thresholds are introduced as part of Version 1.2 of ISDA SIMM™ as of 4th February 2017. We must derive our own co-variance matrix between currency pairs in order to implement the new concentration thresholds into our ISDA SIMM Excel calculator. We provide a step-by-step guide that builds on our previous explanations of the model. UPDATE: […]

The Average Maturity of Swaps Is Increasing

We calculate the average maturity of USD IRS traded across SEFs. Over the past 3 years, this average maturity has meaningfully increased. This maturity extension has been seen on both D2D and D2C venues. The activity across D2D venues suggests that dealers continue to hedge the bulk of client trades with swaps themselves (as opposed to futures, […]

MIFID II: Instrument Reference Data

Following on from my article on the Trading Obligation For Derivatives under MiFIR, I wanted to look at more recent documents released by ESMA for MiFID II and MiFIR and found a briefing note released on 12 Jan 2017, titled “MiFID II technical data reporting requirements“. It starts with the following table: Interesting. Lets look […]

What I Learned At SEFCON VII

I attended SEFCON 7 yesterday to see what is going on in the world of Swap Execution Facilities. I had been thinking SEF’s were business as usual by now, so I went to see if anything cooking in the oven, or might be cooking after the Trump administration starts up. Session 1 Chairman Massad gave […]

CCP Disclosures 3Q 2016 – Trends in the Data

Central Counterparties recently published their latest CPMI-IOSCO Quantitative Disclosures, so lets look at trends in the data, similar to my article on 2Q 2016 trends. Background Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more are published each quarter with […]

VM Big Bang – Analysing CSA Amendments

The VM Big Bang deadline is on March 1st 2017. We explain how a CSA governs Variation Margin for OTC Derivatives. ISDA are providing a Variation Margin protocol, allowing industry participants to efficiently amend their bilateral margin agreements (CSAs). We analyse what some of the changes could mean from a pricing perspective. Using a simple example, we highlight why the […]

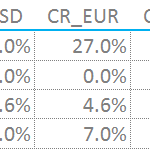

What percentage of client trades are cleared?

We combine BIS and Clarus data sources to provide a holistic view of IRS markets. Almost all of D2D volumes are now cleared, with little variability across the major currencies. Clearing in Dealer-to-Client IRS markets is highly currency dependent. Clearing in D2C markets varies from 27% (CHF IRS) up to 67% (USD IRS). 2016 – It was all […]

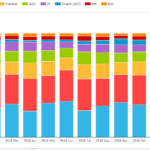

2016 SEF Market Share Statistics

In this article I will look at Swap Execution Facility (SEF) volumes and market share in 2016 for Credit, Foreign Exchange and Interest Rate Derivative asset classes. Clarus SEFView collects daily volumes published by each SEF and normalises this data to allow meaningful comparison and determination of market share statistics. Summary: CRD Index, Option and […]

Clarus Research cited at UK Parliament Treasury Committee

LSE’s Xavier Rolet cited our research in today’s UK parliament treasury committee meeting. During the session on ‘The UK’s future economic relationship with the European Union’ it was this research on EUR clearing that he referred to; ‘Moving Euro Clearing out of the UK: the $77bn problem?’, in answer to questions from Jacob Rees-Mogg. The […]

Top 10 CFTC Fines of 2016

Have you ever wondered how many people get in trouble with the CFTC every year, and what they got in trouble for? Over the holidays, I read through all 103 CFTC enforcement actions from calendar year 2016. As such, I am now in a position to give you my favorite CFTC fines of 2016. Headline […]