Could the Nasdaq default happen in Rates markets?

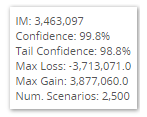

What could cause a Rates CCP to lose €100m from the Default Fund? We look at 10y IRS in NOK vs SEK. We find that liquidity add-ons prevent very large positions from being under-margined. Nevertheless, we present a scenario that causes a €74m loss. And then we explain why we really shouldn’t worry about it! […]

Non-Deliverable Swaps Clearing Volumes

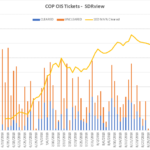

This year both CME and LCH launched clearing in new Non-Deliverable Swap (NDS) currencies and in today’s article I will look at how volumes in these products have performed. CME – NDS in CLP and COP In May 2018, CME launched Chilean Peso and Columbian Peso NDS as new currencies and both of these have […]

Default at Nasdaq Clearing

Last week’s default at Nasdaq Clearing in the power market, generated a lot of press, both because member defaults are few and far between events at CCPs and the fact that it coincided with the ten year anniversary of the Lehman’s bankruptcy. There are few analogies that we can draw between the two events; the […]

ESTER – What You Need To Know

ESTER will be the European Risk Free Rate (RFR), following an announcement from the European working group. This means that ESTER will replace EONIA (and EURIBOR) as the most important interest rate in Europe. Pre-ESTER data is now available, including volumes. The race starts now to be the first to trade ESTER swaps! What You Need […]

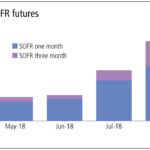

Swaps Data: The race to replace Libor

My monthly Swaps Review in Risk Magazine discusses Libor and looks at derivatives volumes in the Alternative Reference Rates that have been selected to replace it. I look in detail at SOFR Futures, SONIA and EONIA Swaps. Please click here for free access to the full article on Risk.net.

Capital and RWAs of top European Banks – 2017 to 2018

It is a year since we last looked at the Capital and RWA of European banks, so today I will look at what the past year’s data shows. Background One of the lessons learned from the Great Financial Crisis was that Banks were under capitalised commensurate to their risk exposure; leading to new Basel III […]

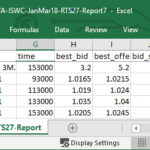

MiFID II Best Execution RTS27 – What the Data Shows

MiFID II Best Execution RTS27, requires Trading Venuesand Systemic Internalisers (SIs) to make public relevant data on the execution quality for financial instruments subject to the trading obligation. This data is published quarterly, with a quarterly lag, so the Best Execution reports for 1Q 2018 are now available from many MTFs, OTFs and SIs. In […]

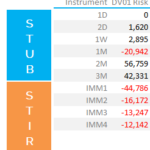

Mechanics of FRA Risks

Managing FRAs and Libor fixings on Swaps is complex. Short-end traders must balance their exposure between the Stub and STIR futures. Stub risk decays with time and changes with LIBOR fixings each day. It must therefore be carefully managed around event risks such as Central Bank meetings. IMM roll dates also result in PnL volatility […]