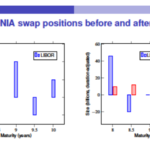

Compression Auctions for RFRs

At the December 2018 SONIA Working Group, Darrell Duffie (Stanford University), presented a way of compressing existing LIBOR contracts into SONIA contracts. I think it is worth reviewing the suggested methodology. I also put forward a slight alternative that draws heavily on the work of Duffie. This idea is meant for discussion purposes, so please […]

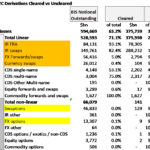

Will UMR lead to a further material shift to clearing?

In my previous post Counterparty Risk: Some Way to Go for Derivatives, I concluded that uncleared OTC counterparty risk is bigger than the 80% cleared traded notional volumes might imply. Of all counterparty risk about two thirds (65%) or more is uncleared and about half (49%) or more is linear delta. A lot is riding […]

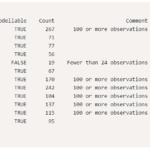

FRTB Risk Factor Eligibility Test (RFET)

In January 2019, the Basle Committee on Banking Supervision (BCBS) revised the 2016 market risk framework, generally known as the Fundamental Review of the Trading Book (FRTB) to address design and calibration issues and to provide further clarification. One of the topics of interest is an improved criteria for the identification of modellable risk factors […]

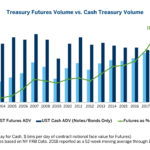

USD Swaps Market vs Futures Market Size

What is the biggest market in USD Rates? Are futures bigger than swaps? Are cash bonds even bigger? We build on important research from both CME and the CFTC to try to answer those questions. We look at Clarus data to measure the DV01 traded in both swaps and futures in long-end USD Rates. We […]

Test Data for the Cumulative Trivariate Normal Distribution

Using Java I implemented the double precision algorithm to compute the cumulative trivariate normal distribution found in A.Genz, Numerical computation of rectangular bivariate and trivariate normal and t probabilities”, Statistics and Computing, 14, (3), 2004. The cumulative trivariate normal is needed to price window barrier options, see G.F. Armstrong, Valuation formulae for window barrier options”, […]

What Traded On-SEF in 2018?

We look at what traded on- and off-SEF in 2018 across Rates and Credit markets. As a result of the CFTC’s proposed rule, we look at what is voluntarily trading on-SEF at the moment. We find that most voluntary SEF executed volumes are in USD-denominated FRA and OIS products. Liquidity is shown to be very high for SEF-executed, standardised […]

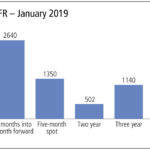

Swaps Data: SOFR volume and margin insights

My monthly Swaps Review in Risk Magazine looks at: IBOR benchmark reform CME SOFR Futures SOFR Swaps Uncleared margin rules Swaptions NDF in major ccy pairs Please click here for free access to the full article on Risk.net

What Traded Off-SEF in 2018?

We look at what traded off-SEF in 2018 across Rates markets. As a result of the CFTC’s proposed rule, we look at products that are mandated to clear. We find that most off-SEF volumes are in short-dated FRA and OIS products. For Fixed-Float traded off-SEF, 75% of it is forward starting. Introduction We are always […]

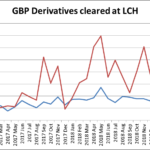

Growth in RFR Markets: Is 2019 the pivotal year?

I have previously written about the changes to derivative markets and the ways they are accommodating and adjusting to replacing Libor. Trades which reference Libor and other like benchmarks are gradually being replaced with RFR trades across many currencies and products as 2021 draws ever nearer. In this blog I will look at some recent […]