Incentives for Central Clearing and the Evolution of OTC Derivatives

We summarise the recent CCP12 report “Incentives for Central Clearing”. This report looks at the current state of play in Cleared FX, Interest Rates and Credit. It analyses particular niches in clearing, including Latam Rates and NDFs. It concludes that clearing has increased for Linear products, but Option markets remain uncleared. Further studies on legacy […]

€STR – What You Need to Know

€STR (né ESTER) will be the Risk Free Rate (RFR) for EUR markets. Publication begins 2nd October 2019. The ECB will provide a calculation of the spread between €STR and EONIA. The spread is likely to be around 8.7 basis points. What You Need to Know about €STR (ESTER) Some of our readers may be […]

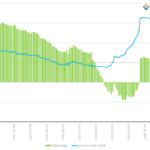

LIBOR Fallbacks – What will the GBP spread be?

We take a look at historic data for SONIA and GBP LIBOR. ISDA’s work on LIBOR fallbacks allows us to look into the potential values of the historic spread. We compare to the forward-looking LIBOR-OIS spreads to the backward looking compounded RFR values. Initial analysis shows that the look-back period will be an important consideration. […]

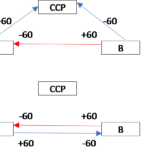

Reducing Counterparty Risk of Uncleared Derivatives

In my previous posts I concluded that uncleared counterparty risk is bigger than traded notional figures suggest and that, so far, UMR has only driven a limited further shift towards clearing. Here, as promised, I take a spin through approaches which complement new trade clearing and can also improve OTC uncleared counterparty risk efficiency. Summary […]

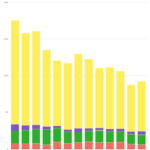

KCCP – Clearing is Getting Cheaper

KCCP defines the amount of capital that must be held versus default fund contributions at a CCP. The lower the value of KCCP, the lower the overall cost of clearing. CPMI-IOSCO public disclosures show that KCCP has decreased at all of the major CCPs in the past three years. We look at the data and […]

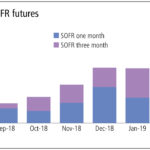

Swaps Data: SOFR Swaps slip, Futures flip

My monthly Swaps Review in Risk Magazine looks at: Volumes in SOFR Futures SOFR Swaps AONIA and SONIA Swaps Volumes and tenors traded Volumes in EONIA and FedFund Swaps Please click here for free access to the full article on Risk.net.

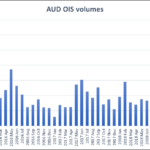

RFRs, Cross Currency Swaps and Australian markets

Cross-currency swap markets are in the process of adapting to a post-Libor environment. New trades will reference the RFRs or risk a complicated process of renegotiating fallbacks (in the case of legacy trades) or incorporating the proposed ISDA fallbacks, when the 2006 ISDA Definitions change. Either way, continuing to reference Libor past 2021 will become […]

Is the Leverage Ratio impacting Swaps Trading?

Is the Leverage Ratio impacting Swaps Trading in Europe? This is a question posted by the authors of a recent ECB Working Paper, “The anatomy of the euro area interest rate swap market“. We provide an overview of the paper and look through the window that it provides into post-trade data in Europe. Executive Summary […]