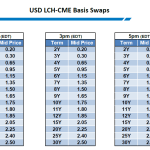

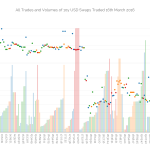

Identifying CCP Basis Trades in the SDR

We run a programme to identify CCP basis trades in SDRView We successfully identify the trades reported by SEFs every day within the SDR data We also find a surprisingly high number of trades transacted at the same time but at different prices – which are not CCP Basis trades. This suggests that price discovery […]

Data correction with fuzzy string matching

We are all familiar with Google’s “Did you mean” correction for misspelt search terms. But how does it work? There is a great chapter by Norvig in the book ‘Beautiful Data: The stories behind elegant data solutions’, that discusses and implements a basic spelling corrector, using only a few lines of python code. The chapter […]

オフSEFについて

我々は最近発表されたバンクオブイングランド(BOE)のワーキングペーパーからの知見について、いくつかここで紹介している。その1つは、米国におけるSEFでのUSD建て金利スワップ(ドル金利スワップ)のトレードについて、流動性は増加していて、同時にトレーディングにかかるコストは減少していると言うものだ。

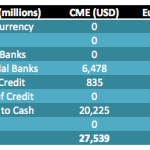

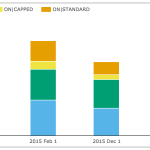

How Cash is Held by Clearing Houses

A lot has been written about the increasing systemic importance of Derivatives Clearing Houses, so I thought it would be interesting to see what the new CCP Quantitative Disclosures show on how cash is held by CCPs and the differences in practice between them. As the relevant disclosures are generally at a Clearing House level and not at […]

Swaps Price Data – Painting the full Liquidity Picture

Clarus price data has unique features that you cannot find elsewhere Categorising traded prices by package type reveals trends that you cannot see in a flat data series Our curation programme and augmentation of prices adds to our volume analysis in Swap markets A true picture of liquidity can be painted using prices, volumes and price dispersion measures. 10y […]

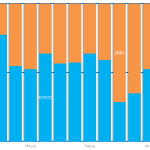

What is Left Off-SEF ?

We’ve written a few pieces now on the recent findings from the Bank Of England working paper. The BOE found that SEF trading in the USA has both (a) increased liquidity and (b) decreased execution costs for USD swaps. My colleague Chris validated the liquidity aspect in his recent blog using our own Clarus data and […]

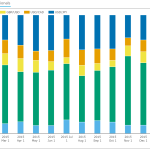

Swaptions Clearing at CME

Last week CME Group announced that it will begin clearing Swaptions on April 11, 2016 and this triggered my interest in revisiting trading volumes and taking a deeper dive into margin requirements for Swaptions. Volumes in SDRs I last covered Swaption volumes in Jan 2015, so lets use SDRView to look at volumes for US persons: Showing: […]

Liquidity on the Bloomberg SEF

We analyse the liquidity on Bloomberg SEF…. …by measuring the price dispersion of 10 Year USD Swaps using the methodology from a recent Bank of England staff paper. We compare these measures of liquidity versus the broader SEF market. We find that in the past 6 months, liquidity is higher on the Bloomberg SEF relative to the rest of the […]

SBSDR: The SEC Version of SDR

The CFTC began publishing rules about Swap Data Reporting in 2011, and we’ve come a very long way since then. Just read any of our blogs on SDR data and you’ll realize there is a world of data now on this once-opaque market. The SEC, however, took it a bit easier in their rulemaking for […]

BREXIT: What do the FX Option volumes tell us?

Regular readers may recall that we looked at the break of the SNB’s EUR/CHF cap back in January 2015 in this blog. “Francaggedon” was a unique event without any pre-warning, and yet we were still able to see evidence in the data of fortuitous/lucky/profitable trading strategies in fairly decent size. Now that the “Brexit” referendum […]