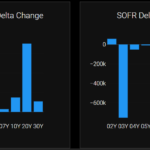

SOFR Discounting for Cleared Swaps

CME and LCH propose to change USD Swaps discounting and Price Alignment Interest (PAI) from Fed Funds (EFFR) to SOFR on October 17th 2020. By creating SOFR discounting risk from that date, this change should result in a need to hedge SOFR risk and drive increased liquidity as well as extend the tenors of SOFR Swaps […]

SONIA Market Volumes – What is Going On?

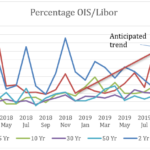

SONIA has seen some growth over the past year or so which we expected. Edwin Schooling Latter, Director of Markets and Wholesale Policy at the FCA in January 2019 and Andrew Bailey, Chief Executive Officer at the FCA in July 2019, both commented on the growth of SONIA derivatives markets. In summary the market volume […]

ISDA SIMM v2.2 – Are you ready?

ISDA SIMM 2.2 is effective December 1, 2019 Updated with a full re-calibration and industry backtesting Initial Margin will change for all portfolios Our clients can check the impact leading up to the effective date And can be confident on implementing SIMM v2.2 on time If you are interested in joining them, we offer free trials […]

What does SOFR volatility mean for LIBOR Fallbacks?

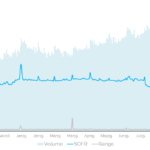

SOFR fixings have exhibited an elevated level of volatility in recent weeks. We look at the impact this may have on LIBOR fallback spreads for 1 month USD LIBOR. We use our IBOR Transition Management apps that we recently announced. The data shows that there are sustained periods where the realised spread has been negative, […]

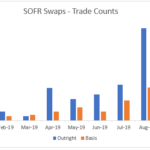

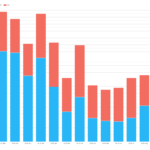

SOFR Swap Volumes – October 2019

SOFR vs FF Basis Swaps, a new high in Sep-19 of $19 billion SOFR Outright Swaps, less trades and notional than Aug-19 SOFR Swaps were mostly Off SEF and Cleared For On SEF, tpSEF reported the most trades Oct-19 volumes are shaping up to exceed Sep-19 LCH SwapClear reported $45 billion notional in Sep-19 Clarus […]

CAD Rates Markets and CORRA Reform

Canadian Rates markets look to be in an especially strong place from a market infrastructure viewpoint. CAD IRS trades versus a term rate, CDOR, which is based on real quotes from six panel banks. The underlying market for CDOR, Banker Acceptances, is a growing market of significant size (CAN$85bn outstanding). Meanwhile, OIS trading vs CORRA […]

NDF Clearing September 2019

CFTC data shows a sharp increase in NDF clearing since July this year. September 2019 was a record month for the notional of NDFs cleared. BIS data shows that NDF markets doubled in size between April 2016 and April 2019. Is Phase 4 of the Uncleared Margin Rules accelerating the uptake of NDF clearing? SDRView […]

CPMI-IOSCO Quantitative Disclosures 2Q 2019

Clearing Houses 2Q 2019 CPMI-IOSCO Quantitative Disclosures are now available, so lets look at what the data shows, similar to my CCP Disclosures 1Q 2019 article. Summary: Initial Margin for IRS is up 11% in the quarter and 18% in a year IM for CDS and ETD was flat in the quarter and up 12% in a year […]

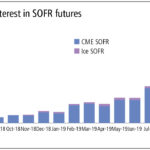

Swaps Data: Are RFRs on track to replace Libor?

My monthly Swaps Review looks at: USD SOFR Futures and growth in open interest USD SOFR Swaps outstanding notional GBP Libor and Sonia Swaps Tenor breakdown of Sonia Swaps Sonia Futures growth in open interest Please click here for free access to the full article on Risk.net.

Tools for IBOR Transition Management

Today we put out the press release, Clarus Financial Technology releases IBOR Transition Management Tools and in this blog I wanted to provide more details on our offering. Before I do that, another point to note is that we recently authored a whitepaper with our friends at Finastra, titled “IBOR Transition Made Simple“, which is […]